Regions Bank 2009 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2009 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

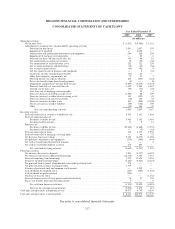

|

|

The allowance is maintained at a level believed adequate by management to absorb probable losses inherent

in the loan portfolio. Management’s determination of the adequacy of the allowance is a quarterly process and is

based on an evaluation of the loan portfolio, historical loan loss experience, current economic conditions,

collateral values of properties securing loans, volume, growth, quality and composition of the loan portfolio,

regulatory guidance, and other relevant factors. Unfavorable changes in any of these, or other factors, or the

availability of new information, could require that the allowance be adjusted in future periods. Actual losses

could vary from management’s estimates. No portion of the resulting allowance is allocated to any individual

credits or group of credits except for specific reserves required by authoritative accounting literature. The

remaining allowance is available to absorb losses from any and all loans.

Regions’ assessment of allowance levels is determined in accordance with GAAP and regulatory guidelines.

In determining the allowance, management uses information to stratify the loan portfolio into loan pools with

common risk characteristics. Loan pools in the portfolio are assigned estimated allowance amounts of loss based

on various factors and analyses, including but not limited to, current and historical loss experience trends and

levels of problem credits, current economic conditions, changes in product mix and underwriting. Loans deemed

to be impaired include non-accrual loans, excluding consumer loans, and troubled debt restructurings (“TDRs”).

Impaired loans, excluding consumer loans, with outstanding balances greater than $2.5 million are evaluated

individually rather than on a pool basis as described above. For these loans, Regions measures the level of

impairment based on the present value of the estimated projected cash flows, the estimated value of the collateral

or, if available, the observable market price. Regions generally uses the estimated projected cash flow method to

measure impairment. For consumer TDRs, Regions measures the level of impairment based on pools of loans

stratified by common risk characteristics.

In order to estimate a reserve for unfunded commitments, Regions uses a process consistent with that used

in developing the allowance for loan losses. Regions estimates future fundings, which are less than the total

unfunded commitment amounts, based on historical funding experience. Allowance for loan loss factors, which

are based on product and customer type and are consistent with the factors used for portfolio loans, are applied to

these funding estimates to arrive at the reserve balance. Changes in the reserve for unfunded commitments are

recognized in other non-interest expense.

ACCOUNTING FOR TRANSFERS AND SERVICING OF FINANCIAL ASSETS

Regions historically sold receivables, such as commercial loans, residential mortgage loans and dealer loans,

in securitizations and to third parties, including conduits. When Regions sold these receivables, it retained a

continuing interest in the form of interest-only strips, one or more subordinated tranches, servicing rights and/or

cash reserve accounts. These retained interests were initially recognized based on their respective allocated cost

basis on the date of transfer. Any gain or loss on the sale of the receivables depends in part on the previous

carrying amount of the financial assets involved in the transfer, allocated between the assets sold and the retained

interests based on their relative estimated fair value at the date of transfer. Retained interests in the subordinated

tranches and interest-only strips were recorded at fair value and included in securities available for sale.

Subsequent adjustments to fair value are recorded through other comprehensive income. Quoted market prices

for these assets are generally not available, so Regions estimates fair value based on the present value of

expected future cash flows using management’s best estimates of the key assumptions—expected credit losses,

prepayment speeds, weighted-average life, and discount rates commensurate with the inherent risks of the asset.

In calculating prepayment rates, Regions utilizes a variety of prepayment models depending on the loan type and

specific transaction requirements. The models used by Regions include the constant prepayment rate model

(CPR) and the Bond Market Trade Association’s Mortgaged Asset-Backed Securities Division’s prepayment

model (PSA). On a quarterly basis, Regions ensures that any retained interests are valued appropriately in the

consolidated financial statements. Management reviews the historical performance of each retained interest and

the assumptions used to project future cash flows. Assumptions are revised if past performance and future

expectations dictate. The present value of cash flows is then recalculated based on the revised assumptions. See

the “Future Application of Accounting Standards” section of Note 1 for further discussion of the impact of new

accounting literature on transfers of financial assets.

121