Regions Bank 2009 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2009 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

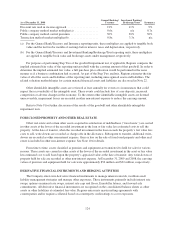

LOANS HELD FOR SALE

At December 31, 2009 and 2008, loans held for sale included commercial loans, investor real estate loans,

residential real estate mortgage loans and student loans. Commercial and investor real estate loans held for sale

consist of certain non-performing loans for which management has the intent to sell in the near term. Regions

primarily classifies new residential real estate mortgage loans as held for sale based on intent, which is

determined when the loans are underwritten. Residential real estate mortgage loans not designated as held for

sale are retained based on available liquidity, interest rate risk management and other business purposes. Regions

elected the fair value option for residential real estate mortgage loans held for sale originated after January 1,

2008. Student loans held for sale include certain loans for which management has the intent to sell in the near

term. Commercial and investor real estate loans held for sale are carried at the lower of cost or estimated fair

value, and student loans held for sale are carried at the lower of aggregate cost or estimated fair value. See Note

22 for discussion of determining fair value. Gains and losses on commercial, investor real estate and student

loans held for sale are included in other non-interest expense. Gains and losses on residential mortgage loans held

for sale are included in mortgage income.

LOANS

Loans are carried at the principal amount outstanding, net of premiums, discounts, unearned income and

deferred loan fees and costs. Interest income on loans is accrued based on the principal amount outstanding,

except for those loans classified as non-accrual. Non-refundable loan origination and commitment fees, net of

direct costs of originating or acquiring loans, are deferred and recognized over the estimated lives of the related

loans as an adjustment to the loans’ effective yield.

Regions engages in both direct and leveraged lease financing. The net investment in direct financing leases

is the sum of all minimum lease payments and estimated residual values, less unearned income. Unearned

income is recognized over the terms of the leases to produce a level yield. The net investment in leveraged leases

is the sum of all lease payments (less non-recourse debt payments), plus estimated residual values, less unearned

income. Income from leveraged leases is recognized over the term of the leases based on the unrecovered equity

investment.

Loans are placed on non-accrual status when management has determined that full payment of all

contractual principal and interest is in doubt, or the loan is past due 90 days or more as to principal and/or interest

unless the loan is well-secured and in the process of collection. When a commercial loan is placed on non-accrual

status, uncollected interest accrued in the current year is reversed and charged to interest income. Uncollected

interest accrued from prior years on commercial loans placed on non-accrual status in the current year is charged

against the allowance for loan losses. When a consumer loan is placed on non-accrual status, all uncollected

interest accrued is reversed and charged to interest income. Charge-offs on commercial loans occur when

available information confirms the loan is not fully collectible and the loss is reasonably quantifiable. Consumer

loans are subject to mandatory charge-off at a specified delinquency date consistent with regulatory guidelines.

Interest collections on non-accrual loans for which the ultimate collectability of principal is uncertain are applied

as principal reductions. In certain limited situations, if management concludes that all principal is ultimately

collectible, collections on non-accrual loans are applied to principal and interest. Regions determines past due or

delinquency status of a loan based on contractual payment terms.

ALLOWANCE FOR CREDIT LOSSES

Through provisions charged directly to expense, Regions has established an allowance for credit losses

(“allowance”). This allowance is comprised of two components: the allowance for loan losses, which is a contra-

asset to loans, and a reserve for unfunded credit commitments, which is recorded in other liabilities. The

allowance is reduced by actual losses and increased by recoveries, if any. Regions charges losses against the

allowance in the period the loss is confirmed.

120