Regions Bank 2009 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2009 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

available, the observable market price. For consumer TDRs, Regions measures the level of impairment based on

pools of loans stratified by common risk characteristics. If current valuations are lower than the current book

balance of the credit, the negative differences are reviewed for possible charge-off. In instances where

management determines that a charge-off is not appropriate, a specific reserve is established for the individual

loan in question. That specific reserve is incorporated as a part of the overall allowance for credit losses. The

recorded investment in impaired loans was $5.0 billion at December 31, 2009 and $1.4 billion at December 31,

2008. The allowance allocated to impaired loans, excluding TDRs, totaled $403 million and $130 million at

December 31, 2009 and 2008, respectively. Loans that were characterized as TDRs totaled $1.9 billion and $533

million at December 31, 2009 and 2008, respectively, and the allowance allocated to TDRs at December 31,

2009 and 2008 totaled $38 million and $9 million, respectively. The allocation to TDRs is a result of the type of

loans considered TDRs as well as the current payment status of the borrowers. Restructured residential and home

equity loans comprise 91 percent of all TDRs and 95 percent of all accruing TDRs at December 31, 2009. As

shown in the table below, the majority of consumer TDRs are on accrual status at December 31, 2009, which is

considered an indication of relatively low loss content. The average amount of impaired loans was $3.6 billion

during 2009 and $1.3 billion during 2008. No material amount of interest income was recognized on impaired

loans for the years ended December 31, 2009, 2008 and 2007.

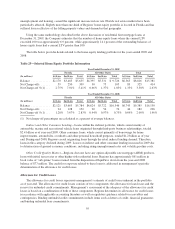

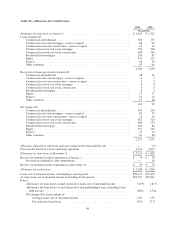

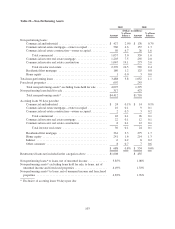

The following table summarizes TDRs for the years ended December 31, 2009 and 2008:

Table 28—Troubled Debt Restructurings

2009 2008

(In millions)

Accruing:

Commercial and industrial .......................................... $ 25 $ 1

Residential first mortgage .......................................... 1,291 406

Home equity ..................................................... 241 48

Other consumer .................................................. 51 —

1,608 455

Non-accrual status or 90 days past due:

Commercial and industrial .......................................... 92 10

Residential first mortgage .......................................... 178 67

Home equity ..................................................... 17 1

287 78

$1,895 $533

The increase in TDRs in 2009 is primarily related to restructuring of residential first mortgage and home

equity loans. Regions continues to work to meet individual needs of consumer borrowers to stem foreclosures

through the Customer Assistance Program. As a result, Regions initiated a significant number of extensions and

modifications beginning in late 2008 and continuing throughout 2009.

NON-PERFORMING ASSETS

Non-performing assets consist of loans on non-accrual status and foreclosed properties. Loans are placed on

non-accrual status when management has determined that payment of all contractual principal and interest is in

doubt, or the loan is past due 90 days or more as to principal and interest unless well-secured and in the process

of collection. When a commercial loan is placed on non-accrual status, uncollected interest accrued in the current

year is reversed and charged to interest income. Uncollected interest accrued from prior years on commercial

loans placed on non-accrual status in the current year is charged against the allowance for loan losses. When a

consumer loan is placed on non-accrual status, all uncollected interest accrued is reversed and charged to interest

income.

101