Regions Bank 2009 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2009 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

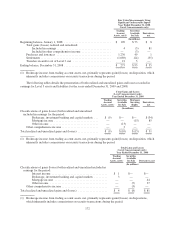

unobservable assumptions reflect the Company’s own estimates for assumptions that market

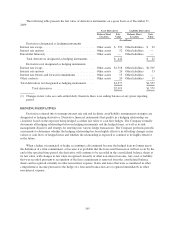

participants would use in pricing the asset or liability. Valuation techniques typically include option

pricing models, discounted cash flow models and similar techniques, but may also include the use of

market prices of assets or liabilities that are not directly comparable to the subject asset or liability.

ITEMS MEASURED AT FAIR VALUE ON A RECURRING BASIS

Trading account assets, securities available for sale, mortgage loans held for sale, and derivatives were

recorded at fair value on a recurring basis during 2009 and 2008. Mortgage servicing rights were recorded at fair

value on a recurring basis during 2009 and at lower of aggregate cost or estimated fair value during 2008. Below

is a description of valuation methodologies for these assets and liabilities.

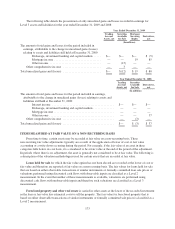

Trading account assets, net and securities available for sale primarily consist of U.S. Treasuries,

mortgage-backed and asset-backed securities (including agency securities), municipal bonds and equity securities

(primarily common stock and mutual funds). Regions uses quoted market prices of identical assets on active

exchanges, or Level 1 measurements. Where such quoted market prices are not available, Regions typically

employs quoted market prices of similar instruments (including matrix pricing) and/or discounted cash flows to

estimate a value of these securities, or Level 2 measurements. Level 2 discounted cash flow analyses are

typically based on market interest rates, prepayment speeds and/or option adjusted spreads. Level 3

measurements include discounted cash flow analyses based on assumptions that are not readily observable in the

market place. Such assumptions include projections of future cash flows, including loss assumptions, and

discount rates. Trading assets are presented net of short-sale liabilities which are valued based on the fair value of

the underlying securities.

Mortgage loans held for sale consist of residential first mortgage loans held for sale that are valued based

on traded market prices of similar assets where available and/or discounted cash flows at market interest rates,

adjusted for securitization activities that include servicing value and market conditions, a Level 2 measurement.

Regions has elected to measure mortgage loans held for sale at fair value by applying the fair value option (see

additional discussion under the “Fair Value Option” section below).

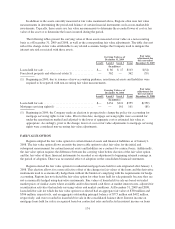

Mortgage servicing rights consist of residential mortgage servicing rights and were valued during 2009

using an option-adjusted spread valuation approach. During 2008, mortgage servicing rights were valued by

projecting and discounting future cash flows. Various assumptions including future cash flows, market discount

rates, expected prepayment rates, servicing costs and other factors are used in the valuation of mortgage servicing

rights, and therefore are Level 3 measurements. As discussed in Note 1, on January 1, 2009, the Company made

an election to prospectively change the policy of accounting for mortgage servicing rights under the fair value

method. Prior to this date, mortgage servicing rights were accounted for under the amortization method and

adjusted to the lower of aggregate cost or estimated fair value as appropriate.

Derivatives, net which primarily consist of interest rate contracts that include futures, options and swaps,

are included in other assets and other liabilities (as applicable) on the consolidated balance sheets, and are

presented in the tables below as a net amount. For exchange-traded options and futures contracts, values are

based on quoted market prices, or Level 1 measurements. For all other options and futures contracts traded in

over-the-counter markets, values are determined using discounted cash flow analyses and option pricing models

based on market rates and volatilities, or Level 2 measurements. Interest rate lock commitments on loans

intended for sale, treasury locks and credit derivatives are valued using option pricing models that incorporate

significant unobservable inputs, and therefore are Level 3 measurements.

Interest rate swaps are predominantly traded in over-the-counter markets and, as such, values are determined

using widely accepted discounted cash flow models, or Level 2 measurements. These discounted cash flow

models use projections of future cash payments/receipts that are discounted at mid-market rates. These valuations

are adjusted for the unsecured credit risk at the reporting date, which considers collateral posted and the impact

of master netting agreements.

170