RBS 2003 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

Operating and financial review continued

98

Operating and financial review

Credit risk (continued)

Provisions

The Group provides for losses in its loan portfolio so as to

record impaired loans and advances at their expected ultimate

net realisable value. The objective is to set provisions based on

the current understanding of the portfolio. To reach this

understanding, retail and corporate loans and advances are

treated separately.

The Group’s retail portfolios which consist of small value, high

volume credits have highly efficient largely automated processes

for identifying problem credits and very short timescales,

typically three months, before resolution or adoption of various

recovery measures.

Corporate portfolios consist of higher value, lower volume

credits, which tend to be structured to meet individual

customers requirements. These portfolios do not have an

automated provisioning process, relying on individual expert

judgement, controls and oversight to identify problems.

Early and proactive management of problem exposures ensures

that credit losses are minimised. Specialised units are used for

different customer types to ensure that the appropriate risk

mitigation is taken in a timely manner.

Specific and general provisions

Provisions fall into one of two categories, specific or general:

•Specific provisions: arise when the creditworthiness of a

borrower has undergone a significant deterioration and the

recovery of the advance is in significant doubt. The amount

of specific provision will reflect the financial condition of the

borrower, the realisable value of security and the costs of

recovery.

•General provisions: cover losses that have not yet been

specifically identified but are known from experience to be

present in any portfolio of loans. The level of general

provision reflects the size and diversity of the Group’s loan

portfolio, past experience, the current state of the

economies in which the Group operates and the scope of

specific provisioning procedures.

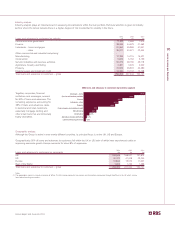

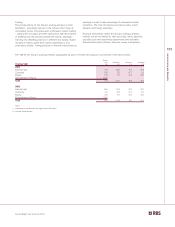

Provisions for bad and doubtful debts at the end of 2003 were

broadly unchanged from the previous year end. The increase

in provisions of £1,461 million through the charge to the profit

and loss account was substantially offset by the amounts

written-off, net of recoveries, of £1,447 million. This, coupled

with the growth in the portfolio, led to a reduction in the ratio of

provisions to loans and advances to customers from 1.72% at

the end of 2002 to 1.53%.

The coverage ratio of closing provisions as a percentage of

REIL has reduced to 76% from 81% at the end of 2002. This is

due to a slight shift in the composition of REIL away from

larger corporate customers, against which the Group typically

holds less security and thus requires higher provisions

proportionately, and into smaller mid-corporate customers

against which the Group tends to hold higher levels of security.

The coverage ratio of total closing provisions as a percentage of

PPL and REIL has increased to 68% from 65% and 66% at the

end of 2002 and 2001 respectively.

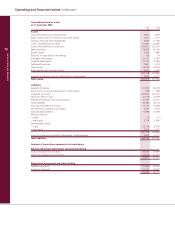

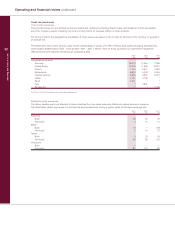

2003 2002 2001

Summary of provisions £m £m £m

Specific provision13,356 3,323 3,031

General provision 566 597 614

Total bad and doubtful debt provisions 3,922 3,920 3,645

Total loans and advances to customers 256,453 227,244 194,137

Specific provision as a percentage of loans and advances to customers 1.31% 1.46% 1.56%

General provision as a percentage of loans and advances to customers 0.22% 0.26% 0.32%

Total provisions as a percentage of loans and advances to customers 1.53% 1.72% 1.88%

Closing provisions for bad and doubtful debts expressed as a:

% of REIL 76% 81% 81%

% of REIL and PPL 68% 65% 66%

(1) Excludes specific provisions against loans and advances to banks of £7 million (2002 – £7 million; 2001 – £8 million)