RBS 2003 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

101

Annual Report and Accounts 2003

Operating and financial review

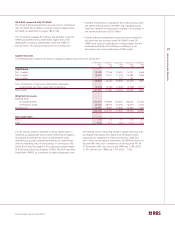

Customer accounts, excluding repo agreements, grew by

£15,841 million (8%), and represent 58% of the Group’s

funding excluding capital and other liabilities. In reflection of

the higher rate of growth in customer loans and advances

excluding reverse repos, up £27,081 million (13%), the

proportion of funding from wholesale sources has increased.

Repo agreements with corporate and institutional customers

are undertaken primarily by RBS Greenwich Capital in the US

and by Financial Markets. Repo activity with customers

represented 7% of the Group’s funding excluding capital and

other liabilities at 31 December 2003.

Deposits by banks increased by £12,603 million to represent

19% of the Group’s funding, excluding capital and other

liabilities. Deposits by banks are taken from a wide range of

counterparties, with the largest single depositor continuing to

represent less than 1% of the Group’s total funding.

Debt securities in issue increased by £7,078 million to represent

11% of the Group’s funding, excluding capital and other

liabilities, at 31 December 2003. Total debt securities in issue

at 31 December 2003 includes £9,187 million (2002 – £6,035

million) with a maturity of over one year, reflecting the activity of

the Group in raising term funds through its Euro Medium Term

Note programme and other term issues.

The Group remains well placed to access various wholesale

funding sources from a wide range of counterparties and

markets, and the changing mix evident between customer

repos, deposits by banks and debt securities in issue primarily

reflects comparative pricing and investor/counterparty demand

rather than a material perceived trend.

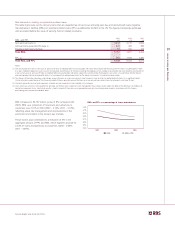

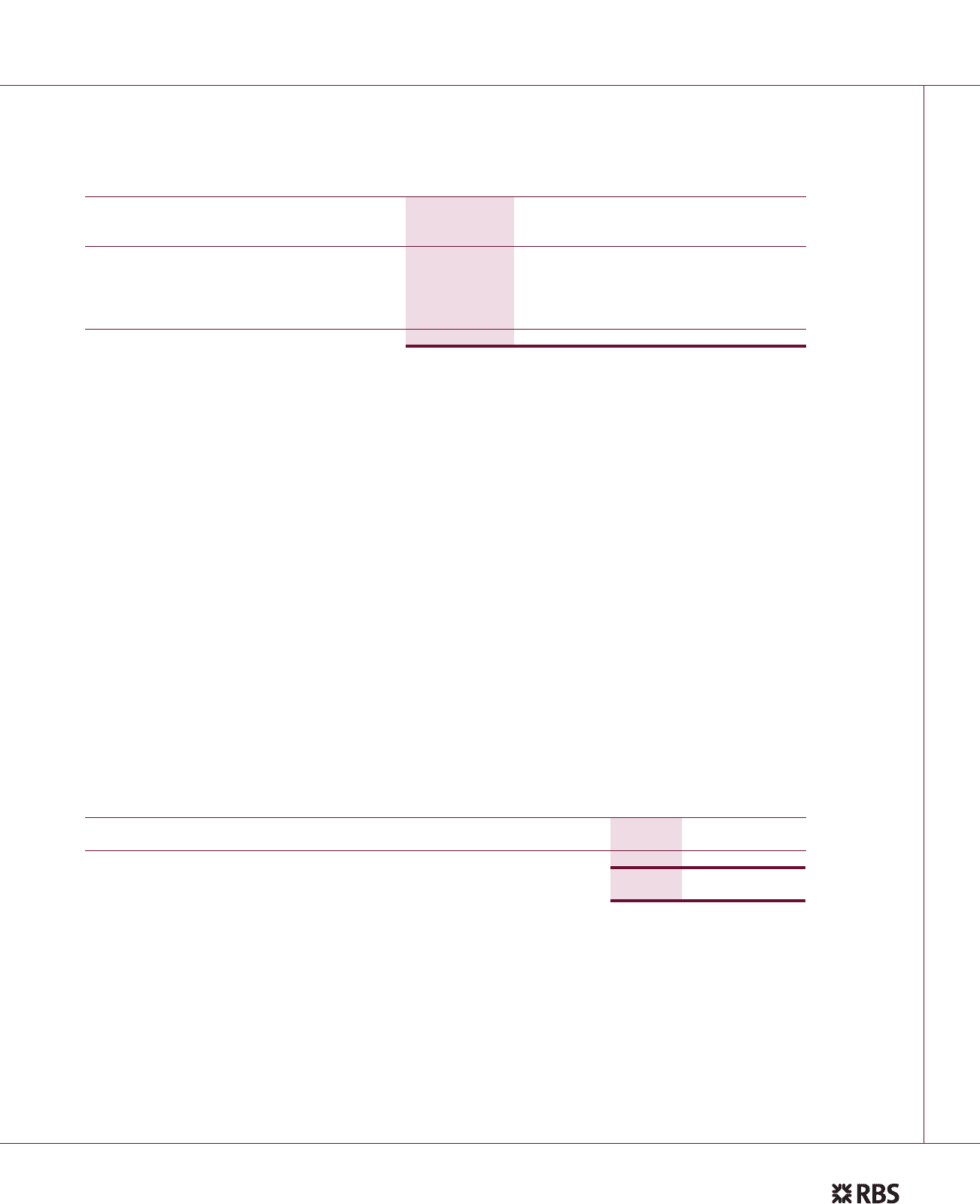

Sources of funding

Excluding capital and other liabilities, customer accounts continue to provide a substantial majority of the Group’s funding and

represent a well diversified and stable source of funds from a wide range of retail, corporate and non-bank institutional customers.

2003 2002 2001

£m % £m % £m %

Customer accounts (excluding repos):

Repayable on demand 141,560 39 127,320 39 115,054 41

Time deposits 68,382 19 66,781 21 66,486 23

Total customer accounts (excluding repos) 209,942 58 194,101 60 181,540 64

Repo agreements with customers 27,021 7 25,060 8 17,455 6

Deposits by banks (including repos) 67,323 19 54,720 17 40,038 14

Debt securities in issue 41,016 11 33,938 10 30,669 11

Short positions 19,128 5 16,381 5 14,622 5

Total 364,430 100 324,200 100 284,324 100

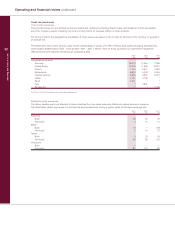

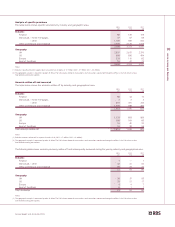

Net customer activity

Net customer lending rose by £11,240 million as the growth in loans and advances to customers exceeded the growth in customer

accounts, thus increasing wholesale market funding to support loan growth. Structural liquidity risk continues to be maintained well

within the Group’s policy parameters.

2003 2002 2001

£m £m £m

Loans and advances to customers (gross, excluding reverse repos) 232,384 205,303 182,549

Customer accounts (excluding repos) 209,942 194,101 181,540

Customer lending less customer accounts 22,442 11,202 1,009

Customer accounts as % of loans and advances to customers (gross, excluding repos) 90.3% 94.5% 99.4%

In prevailing economic conditions and with interest rates at

historically low levels in the UK, US and Europe, the growth in

demand for borrowing by customers may in the medium term

continue to exceed customer deposits received, thus

increasing net customer lending further. The Group has

evaluated a range of balance sheet management strategies

and has developed plans to increase gradually over time short

term and longer term funding from various wholesale market

sources, whilst maintaining its overall funding structure within

its normal prudent liquidity risk policy parameters.