RBS 2003 Annual Report Download - page 190

Download and view the complete annual report

Please find page 190 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

188

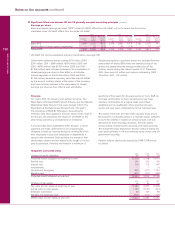

Notes on the accounts continued

Notes on the accounts

Sharesave schemes, under which employees are granted

options at a 20% discount to market value at date of grant.

Under US GAAP, the compensation is based on the

estimated fair value which is charged to the profit and loss

account over the period to their average vesting date.

(o) Variable interest entities

UK GAAP requires consolidation of entities controlled by an

enterprise where control means the enterprise’s ability to

direct the financial and operating policies of an entity with

a view to gaining economic benefits. US GAAP requires

consolidation by the primary beneficiary of a variable

interest entity (“VIE”). An enterprise is the primary

beneficiary of a VIE if it will absorb a majority of the

entity’s expected losses, receive a majority of the entity’s

expected residual returns, or both.

(p) Perpetual regulatory securities

Under UK GAAP, the Group’s perpetual regulatory

securities are classified as liabilities. Under US GAAP, they

are classified as equity instruments.

(q) Acceptances

Acceptances outstanding and the matching customers’

liabilities are not reflected in the consolidated balance

sheet, but are disclosed as memorandum items. Under US

GAAP, acceptances outstanding and the matching customers’

liabilities are reflected in the consolidated balance sheet.

(r) Offset of repurchase and reverse repurchase agreements

Under UK GAAP, debit and credit balances with the same

counterparty are aggregated into a single item where there

is a right to insist on net settlement and the debit balance

matures no later than the credit balance. Under US GAAP,

repurchase and reverse repurchase agreements with the

same counterparty may be offset only where they have the

same settlement date specified at inception.

(s) Deferred taxation

Accounting for deferred tax under UK GAAP is consistent

with US GAAP except that deferred tax is not recognised

under UK GAAP on certain timing differences resulting from

the roll-over of gains on disposal of properties, but is

provided under US GAAP on such differences.

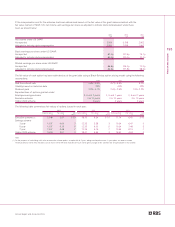

Recent developments in US GAAP

In April 2003, the Financial Accounting Standards Board

(“FASB”) issued Statement of Financial Accounting Standards

(“SFAS”) 149 ‘Amendment of Statement 133 on Derivative

Instruments and Hedging Activities’. It amends and clarifies

accounting for derivative instruments, including certain

derivative instruments embedded in other contracts, and

hedging activities under SFAS 133. The statement is effective

for contracts entered into or modified after 30 June 2003, and

for hedging relationships designated after 30 June 2003.

Implementation of SFAS 149 has had no effect on the Group’s

US financial information.

The FASB issued SFAS 150 ‘Accounting for Certain Financial

Instruments with Characteristics of both Liabilities and Equity’

in May 2003. This statement addresses classification and

measurement by an issuer of certain financial instruments with

characteristics of both liabilities and equity. SFAS 150 also

addresses the classification of certain financial instruments

that embody obligations to issue equity shares. The statement

is effective for financial instruments entered into or modified

after 31 May 2003 and is otherwise effective on or after 15

June 2003. SFAS 150 has not affected the classification of any

of the capital instruments issued by the Group.

The FASB issued SFAS 132 (revised) ‘Employers’ Disclosures

about Pensions and Other Postretirement Benefits – an

amendment of FASB Statements No. 87, 88 and 106’ in

December 2003. This statement retains the disclosures

required by SFAS 132 and requires additional information on

changes in pension and other post-retirement benefit

obligations and fair value of assets. SFAS 132R is effective for

the Group’s 2003 financial statements.

In December 2003, the FASB issued FASB Interpretation

(“FIN”) No. 46 (revised) ‘Consolidation of Variable Interest

Entities, an interpretation of ARB No. 51.’ FIN 46R clarifies

some of the provisions of FIN 46, issued in January 2003, and

exempts certain entities from its requirements. FIN 46R

replaces FIN 46 but as FIN 46R contains deferral provisions,

FIN 46 is extant until FIN 46R is applied. FIN 46 and FIN 46R

address accounting for VIEs. Expected losses and expected

residual returns of a VIE have been clarified in FIN 46R as the

expected negative variability and positive variability,

respectively, in the fair value of its net assets excluding

variable interests and include expected variability resulting

from the operating results of the entity.

The Group elected to adopt the provisions of FIN 46R as at 31

December 2003, except in relation to certain investments made

by its private equity business which is involved with entities that

may be deemed to be VIEs. The FASB has deferred non-

registered investment companies (entities that invest for capital

appreciation and income) from the application of FIN 46R until

the scope of investment company accounting has been

clarified by the American Institute of Certified Public

Accountants.

The FASB continues to provide additional guidance on

implementation of FIN 46. As further guidance is provided, the

Group will continue to review the status of the VIEs with which

it is involved.

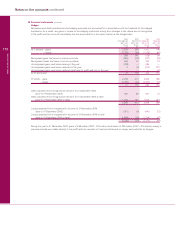

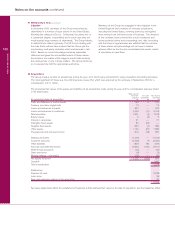

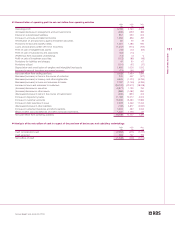

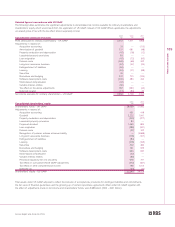

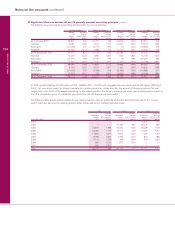

53 Significant differences between UK and US

generally accepted accounting principles (continued)