RBS 2003 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

Operating and financial review continued

78

Operating and financial review

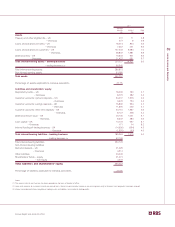

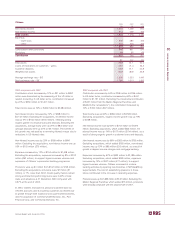

Retail Banking

2003 2002 2001

£m £m £m

Net interest income 2,951 2,840 2,622

Non-interest income 1,452 1,353 1,277

Total income 4,403 4,193 3,899

Direct expenses

– staff costs 777 707 702

– other 227 254 226

1,004 961 928

Contribution before provisions 3,399 3,232 2,971

Provisions 273 213 164

Contribution 3,126 3,019 2,807

£bn £bn £bn

Total banking assets 63.8 57.4 50.9

Loans and advances to customers – gross

– mortgages 36.6 32.1 28.5

– other 25.2 23.5 20.5

Customer deposits 66.3 61.7 56.8

Weighted risk assets 42.9 38.8 35.2

2003 compared with 2002

The division achieved strong volume growth across all personal

product areas - current accounts, mortgages and loans and

savings. Despite lower interest rates and the adverse effect of

the pricing remedies agreed following the Competition

Commission inquiry into SME banking which were implemented

from 1 January 2003, income increased by 5% or £210 million

to £4,403 million, and contribution by 4% or £107 million to

£3,126 million.

Net interest income rose by 4% or £111 million to £2,951 million,

reflecting the continued strong growth in customer advances

and deposits which was partially offset by the implementation

of the Competition Commission pricing remedies and the

impact of a lower interest rate environment. Excluding the

effect of the Competition Commission the increase was 8%.

Average loans to customers, excluding mortgages, grew by

9% or £1.9 billion to £23.7 billion. Average mortgage lending

grew by 12% or £3.6 billion to £33.7 billion. Average customer

deposits increased by 6% or £3.7 billion to £60.9 billion.

Non-interest income rose by 7% or £99 million to £1,452 million.

This reflected further growth in the customer base and a 15%

growth in general insurance income to £301 million. Embedded

value profits of the life assurance business increased by 14%,

or £7 million to £57 million.

Direct expenses increased by 4% or £43 million to £1,004

million. Staff expenses increased 10% or £70 million to £777

million reflecting further investment in customer facing staff.

Other expenses decreased 11% or £27 million to £227 million,

as a result of our rigorous approach to management of non-

staff costs.

The charge for provisions for bad debts increased by £60 million

to £273 million. The overall quality of the loan portfolio remains

stable and the increased charge reflects growth in lending over

recent years particularly in NatWest since its acquisition.