RBS 2003 Annual Report Download - page 194

Download and view the complete annual report

Please find page 194 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

192

Notes on the accounts continued

Notes on the accounts

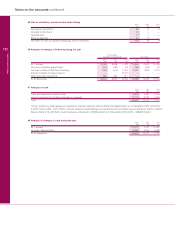

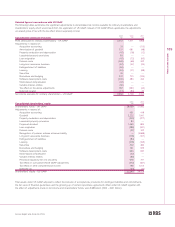

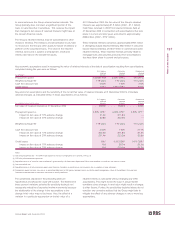

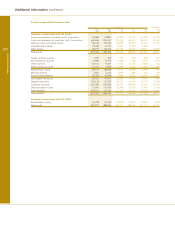

Loan impairment

At 31 December 2003 and 2002, the Group estimated that the

difference between the carrying value of its loan portfolio under

US GAAP and its value in the Group’s UK GAAP financial

statements was such that no adjustment to net income or

consolidated shareholders’ equity was required. At 31 December

2003, the Group’s non-accrual loans, loans past due 90 days

and troubled debt restructurings amounted to £5,157 million

(2002 – £4,871 million). Specific provisions of £2,782 million

(2002 – £2,435 million) were held against these loans. Average

non-accrual loans, loans past due 90 days and troubled debt

restructurings for the year to 31 December 2003 were £5,166

million (2002 – £4,762 million).

Gross interest income not recognised, but which would have

been recognised under the original terms of non-accrual and

restructured loans, amounted to £237 million for the year

ended 31 December 2003 (2002 – £234 million; 2001 – £173

million) from domestic loans and £55 million for the year ended

31 December 2003 (2002 – £73 million; 2001 – £60 million) from

foreign loans. Interest on non-accrual and restructured loans

included in net income was £60 million for the year ended 31

December 2003 (2002 – £47 million; 2001 – £42 million) from

domestic loans and £3 million for the year ended 31 December

2003 (2001 – £7 million; 2000 – £14 million) from foreign loans.

Securities

During 2003, there were no gross gains or gross losses included

in US GAAP net income from transfers of securities from the

available-for-sale category into the trading category. For 2003,

net unrealised losses of £652 million on available-for-sale

securities were included in US GAAP other comprehensive

income and £164 million was reclassified from accumulated

other comprehensive income into US GAAP net income.

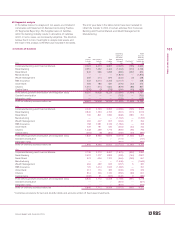

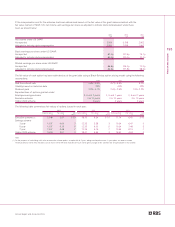

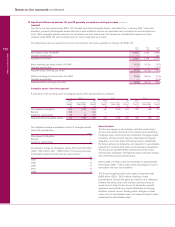

53 Significant differences between UK and US

generally accepted accounting principles (continued)

Cash flow statements

There are many similarities between SFAS 95, ‘Statement of Cash Flows’ as amended by SFAS 104 ‘Statement of Cash Flows – Net

Reporting of Certain Cash Receipts and Cash Payments and Classification of Cash Flows from Hedging Transactions’, and FRS 1

‘Cash Flow Statements’ (Revised). The principal differences are the classifications of certain transactions.

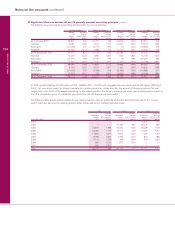

Classification under FRS 1 Classification under SFAS 95

Equity dividends paid Equity dividends paid Financing activities

Dividends paid on non-equity shares Returns on investments and Financing activities

servicing of finance

Tax paid Taxation Operating activities

Purchase and sale of associated and Acquisitions and disposals Investing activities

subsidiary undertakings

Purchase and sale of investment securities Capital expenditure and Investing activities

and fixed assets financial investment

Net change in loans and advances, Operating activities Investing activities

including finance lease receivables

Net change in deposits Operating activities Financing activities

Net change in debt securities in issue Operating activities Financing activities

Short-term funding not Operating activities Financing activities

included in cash