RBS 2003 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

187

Annual Report and Accounts 2003

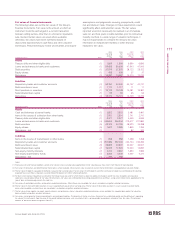

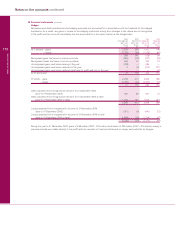

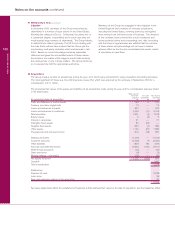

Notes on the accounts

actuary. US GAAP prescribes the method of actuarial

valuation and also requires assets to be assessed at fair

value and the assessment of liabilities to be based on

current interest rates. Additionally, under US GAAP a

minimum additional liability must be recognised if the

accumulated benefit obligation exceeds the fair value of

plan assets and the Group has recorded a prepaid

pension cost or has an accrued liability that is less than the

unfunded accumulated benefit. This minimum additional

liability represents the underfunding of the scheme on an

accumulated benefit obligation basis, together with an

amount equal to the pension prepayment. Movements in

the minimum additional liability, together with the related

deferred tax, are recognised through other comprehensive

income as a deduction from equity.

(h) Long-term assurance business

The shareholders’ interest in the long-term assurance fund

is valued as the discounted value of the cash flows

expected to be generated from in-force policies together

with net assets in excess of the statutory liabilities. Under

US GAAP, for traditional business, premiums are

recognised as revenue when due from the policyholders.

Costs of claims are recognised when insured events occur.

A liability for future policy benefits is established based

upon the present value of future benefits less the present

value of future net premiums. Acquisition costs for

traditional business contracts are charged to the profit and

loss account in proportion to premium revenue recognised.

For unit-linked business, premiums and front-end load-type

charges receivable from customers and acquisition costs

relating to the acquisition of new contracts are capitalised

and depreciated in proportion to the present value of

estimated gross profits. Costs of claims are recognised

when insured events occur.

(i) Extinguishment of liabilities

Under UK GAAP, recognition of a financial liability ceases

once any transfer of economic benefits to the creditor is no

longer likely. Under US GAAP, a financial liability is

derecognised only when the creditor is paid or the debtor

is legally released from being the primary obligator under

the liability, either judicially or by the creditor.

(j) Leasing

In accordance with UK GAAP, the Group’s accounting

policy for finance lease income receivable is to allocate

total gross earnings to accounting periods so as to give a

constant periodic rate of return on the net cash investment,

and certain operating lease assets are depreciated on a

reverse-annuity basis. Under US GAAP, finance lease

income is recognised so as to give a level rate of return on

the investment in the lease but without taking into account

the associated tax flows, and all operating lease assets are

depreciated on a straight-line basis.

(k) Securities

Under UK GAAP, the Group’s debt securities and equity

shares are classified as being held as investment

securities or for dealing purposes. Investment securities

are stated at cost less provision for any permanent

diminution in value. Premiums and discounts on dated debt

securities are amortised to interest income over the period

to maturity. Securities held for dealing purposes are carried

at fair value with changes in fair value recognised in the

profit and loss account. Under US GAAP, securities held by

the Group’s private equity business are considered to be

held by investment companies and are carried at fair value,

with changes in fair value being reflected in net income.

The Group’s other investment debt securities and

marketable investment equity shares are classified as

available-for-sale securities with unrealised gains and

losses reported in a separate component of equity.

(l) Derivatives and hedging activities

SFAS 133 ‘Accounting for Derivative Instruments and

Hedging Activities’ was effective for the Group’s US GAAP

information from 1 January 2001. The Group has not made

changes in its use of non-trading derivatives to meet the

hedge criteria of SFAS 133. As a result, from 1 January

2001, for US GAAP purposes, the Group’s portfolio of non-

trading derivatives has been remeasured to fair value and

changes in fair value reflected in net income. Under UK

GAAP, these derivatives continue to be classified as non-

trading and accounted for in accordance with the underlying

transaction or transactions being hedged. SFAS 133 does

not permit a non-derivative financial instrument to be

designated as the hedging instrument in a fair value hedge

of the foreign exchange exposure of available-for-sale

securities. The Group’s UK and US GAAP reconciliations

also reflect transition adjustments on initial application of

SFAS 133. These adjustments were: a cumulative-effect-

type adjustment increasing net income by £45 million (£65

million less tax of £20 million); and a cumulative-effect-type

adjustment decreasing other comprehensive income by

£51 million (£73 million less tax of £22 million). SFAS 133

also requires derivatives embedded in other financial

instruments to be accounted for on a stand-alone basis if

they have economic characteristics and risks that differ

from those of the host instrument.

US GAAP does not permit a profit or loss to be recognised

on transacting a derivative unless its valuation is based on

observable market data. There is no similar requirement

under UK GAAP. Inception profits and losses reflecting the

application of the Group’s usual pricing methodologies are

recognised as they arise.

(m) Software development costs

Under UK GAAP, most software development costs are

written off as incurred. Under US GAAP, certain costs

relating to software developed for own use that are

incurred after 1 January 1999 are capitalised and

depreciated over the estimated useful life of the software.

(n) Stock-based compensation

Under UK GAAP, no compensation expense is recognised

for the Group’s executive share option schemes, under

which options are granted at the higher of nominal value

and market value on the date of grant and for the Group’s