RBS 2003 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

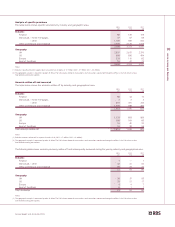

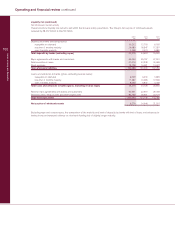

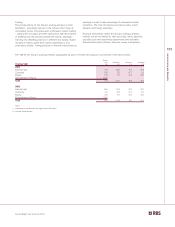

109

Annual Report and Accounts 2003

Operating and financial review

Insurance risk

The Group is exposed to insurance risk, either directly through

its businesses or through using insurance as a tool to reduce

other risk exposures:

•Insurance is a source of risk where the Group sells and

underwrites general insurance and life assurance. The

essence of an insurance contract is the transfer of risk from

the policyholder to the insurer.

The management of insurance risk is overseen by a Pricing

Committee that meets weekly to review underwriting factors,

e.g. car groups, terms and conditions, claims experience. This

is supplemented by a range of system controls and processes

including risk acceptance, with regular independent reviews of

underwriting across the business. Primary focus is on high

volume and relatively straightforward products for example

home and motor. This facilitates the generation of

comprehensive underwriting and claims data, which is used

to monitor and accurately price the risks accepted. This

attention to data analysis is reinforced by tight controls on

costs and claims handling procedures.

Underwriting concentrations and catastrophe exposure are

reviewed and, where necessary, mitigated by reinsurance

which is spread across a number of reinsurers. Reviews of

the Group’s general insurance reserves by external

actuaries are conducted annually.

Investment strategy reflects the maturity of underwriting

liabilities and is governed through Investment Management

Committees, with involvement and oversight from Group

Treasury. The Group’s underwriting experience, the level of

retained risk and solvency are monitored at divisional and

Group level.

•The Insurance Sourcing Department is responsible for the

Group-wide purchase of insurance as a means of reducing

other risk exposures. As such, it is a key component of the

Group Insurance Risk Management process and reports its

activities to the GEMC.

Enterprise risk

In order to adequately identify and manage the full range of

Enterprise risk, the Group has separately defined operational

and external risk:

Operational risk is defined as the risk arising from within the

organisation from:

•People – risks arising from an inappropriate level of staff,

inadequately skilled or managed people.

•Process – risk caused by inadequate or failed internal

processes.

•Systems – risks of inadequately designed or maintained

systems.

•Assets – risk of damage, misappropriation or theft of the

Group’s physical, logical and intangible assets.

External risk is defined as the risk arising from outside of the

organisation in three main areas:

•Business – risks arising from product performance,

competitor activity, supplier unreliability or customer activity.

•Political – risks caused by political unrest or uncertainty,

activity by public interest groups or extremists, and non-

compliance with, or changes to, current legislation.

•Environment – risks arising due to demographic, macro

economic, technical, cultural or environmental change.

Enterprise risk also includes the potential or actual impact on

corporate reputation arising from any of the Group’s activities.

Enterprise risk management is achieved through monitoring the

Group’s exposure to direct or indirect loss using a range of

policies, procedures, data, analytical tools and reporting

techniques. In particular, Group-wide risk management processes

ensure that Enterprise risk issues are quickly escalated and

resolved, that the risks inherent in new products are fully evaluated,

and that emerging external risks are actively monitored.

Operational risk exposures and loss events for each division

are captured through monthly Risk and Control returns, which

provide details on the change of risk exposures for each risk

category in the light of improving/deteriorating trends and the

risk profile of each division.