RBS 2003 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

63

Operating and financial review

Annual Report and Accounts 2003

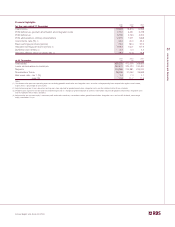

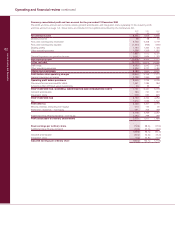

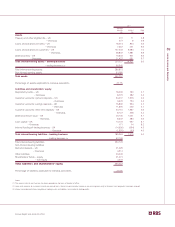

2003 compared with 2002

Profit

Profit before tax, goodwill amortisation and integration costs

increased by 11% or £700 million, from £6,451 million to

£7,151 million.

Profit before tax was up 29%, from £4,763 million to £6,159 million.

Total income

The Group achieved strong growth in income during 2003.

Total income was up 14% or £2,414 million to £19,229 million.

Non-interest income now accounts for 57% of total income.

Excluding acquisitions, total income rose by 10%.

Net interest income increased by 6% to £8,301 million and

represents 43% of total income (2002 – 47%). Average loans

and advances to customers and average customer deposits

grew by 12% and 8% respectively. The benefit of this growth

has more than offset the impact on net interest income of the

Competition Commission inquiry into SME banking in the UK and

the lower interest rate environment in the UK and the US which

have reduced income earned from deposits and investments.

Non-interest income increased by 22% to £10,928 million and

represents 57% of total income (2002 – 53%). Fees receivable

were up 8% with good growth in lending, transmission and

card related fees reflecting higher volumes. General insurance

premium income grew strongly, reflecting volume growth in

both motor and home insurance products, and the acquisition

of Churchill. In addition, volumes in financial markets were up

strongly in both the UK and the US reflecting growth in

customer-driven activity in interest rate protection, mortgage

securitisation and foreign exchange. Income from rental assets

grew by 17% to £1,088 million, reflecting the growth in

operating leases and investment properties.

Net interest margin

The Group’s net interest margin at 3.0% was, in line with the

first half, down from 3.1% in 2002 due to a reduced benefit

from interest-free funds arising from the lower interest rate

environment, and the outcome of the Competition Commission

inquiry into SME banking.

Operating expenses

Operating expenses, excluding goodwill amortisation and

integration costs, rose by 9% to £8,389 million. Excluding

acquisitions, operating expenses were up 7% or £521 million in

support of higher business volumes and 10% income growth.

Cost:income ratio

The strong growth in income together with tight cost management

resulted in a further improvement in the Group’s ratio of

operating expenses (excluding goodwill amortisation and

integration costs and after netting operating lease depreciation

against rental income) to total income, to 42.0% from 44.0%.

Excluding the effect of acquisitions, the cost:income ratio

improved to 42.5%.

Net insurance claims

General insurance claims, after reinsurance, increased by 63%

to £2,195 million. Excluding Churchill, the increase was 29%,

consistent with volume growth in the component parts of the

insurance division.

Provisions

The profit and loss charge for bad debts and amounts written

off fixed asset investments was £1,494 million compared with

£1,345 million in 2002. The profit and loss charge is in line with

the growth in loans and advances.

Credit quality

There has been no material change during the year in the

distribution by grade of the Group’s total risk assets.

The ratio of risk elements in lending to gross loans and

advances to customers at 2.01% at 31 December 2003

showed an improving trend (31 December 2002 – 2.14%).

Risk elements in lending and potential problem loans

represented 2.24% of gross loans and advances to customers

compared with 2.66% at 31 December 2002.

Integration

Integration costs in the year were £229 million, of which, £143

million related to the final elements of the NatWest integration

and £86 million related to other acquisitions, including Citizens’

acquisitions and Churchill.

All integration initiatives in relation to NatWest have been

implemented. The programme benefits, comprising £890

million annual revenue benefits and £1,440 million annual cost

savings, were fully implemented less than three years after the

acquisition of NatWest. Total costs for the integration

programme were £2.3 billion. Since 6 March 2000 the

integration initiatives have contributed a cumulative £5.6 billion

to the Group.

Earnings and dividends

Basic earnings per ordinary share increased by 15%, from

68.4p to 79.0p. Earnings per ordinary share, adjusted for

goodwill amortisation, integration costs and the dividend on

Additional Value Shares (“AVS”), increased by 11%, from

144.1p to 159.3p.

The final dividend of 55p per share amounting to £1.5 billion

was paid on 1 December 2003 to the holders of the AVS

issued in connection with the acquisition of NatWest. A total of

£1 per AVS amounting to £2.7 billion in aggregate has been

paid over three years to shareholders in accordance with the

original schedule.

A final dividend of 35.7p per ordinary share is recommended,

making a total for the year of 50.3p per share, an increase of

15%. If approved, the final dividend will be paid on 4 June

2004 to shareholders registered on 12 March 2004. The total

dividend is covered 3.1 times by earnings before goodwill

amortisation, integration costs and the AVS dividend.