RBS 2003 Annual Report Download - page 214

Download and view the complete annual report

Please find page 214 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

-

226

-

227

-

228

-

229

-

230

|

|

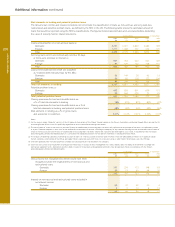

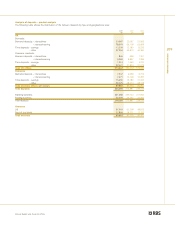

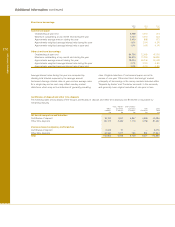

Additional information continued

212

Off balance sheet arrangements

The Group is involved with several types of off-balance sheet

arrangements, including special purpose vehicles, lending

commitments and financial guarantees.

Special purpose vehicles (“SPVs”)

SPVs are vehicles set up for a specific, limited purpose, do not

carry out a business or trade and typically have no employees.

They take a variety of legal forms – trusts, partnerships and

companies – and fulfil many different functions. They constitute

a key element of securitisation transactions in which an SPV

acquires financial assets funded by the issue of securities.

In the normal course of business, the Group arranges

securitisations to facilitate client transactions and undertakes

securitisations to sell financial assets or to obtain funding. It

has established a number of SPVs to act as commercial paper

conduits for customers. SPVs are also utilised in its fund

management activities to structure investment funds to which

the Group provides investment management services.

Under UK GAAP, the Group accounts for securitisations of

assets originated by the Group in accordance with FRS 5

‘Reporting the Substance of Transactions’. Assets are

derecognised and a gain or loss on disposal recognised if all

significant rights or access to benefits relating to those assets

and all significant risks in those benefits are transferred to

others. In cases where there is a significant change in the

entity’s rights to benefit and exposure to risk, the description or

monetary amount relating to an asset should be changed and

a liability recognised for any obligation to transfer benefits that

is assumed. Where a transaction in previously recognised

assets results in no significant change in the entity’s rights to

benefits in the assets or its exposure to risks inherent in those

benefits, the assets should continue to be recognised and no

gain or loss recognised. FRS 5 requires a linked presentation

where a transaction is in substance the financing of an asset

or pool of assets but where the item is financed in such a way

that the Group can suffer a loss which is limited to a fixed

monetary amount. The linked presentation involves showing the

gross amount of assets securitised less the related finance on

the face of the balance sheet – the net amount is included in

total assets. Profit is recognised on entering into the

arrangement only to the extent that non-returnable proceeds

exceed the previous carrying value of the assets securitised.

The Group securitises mortgage loans and other assets.

Under US GAAP, transfers of financial assets are accounted for

and reported based on the application of a financial-

components approach that focuses on control. Under this

approach, after a transfer of financial assets, the Group

recognises the assets it controls and the liabilities it has

incurred, derecognises financial assets when control has been

surrendered, and derecognises liabilities when extinguished.

Transfers of financial assets where the Group has surrendered

control over the transferred assets are accounted for as sales

and any gain or loss recognised in earnings. Otherwise,

transfers are accounted for as collateralised borrowings.

As financial intermediary, the Group arranges securitisations of

client assets. These include multi-seller commercial paper

conduits and client intermediation transactions. The Group has

established a number of SPVs to act as commercial paper

conduits. These allow customers to access liquidity in the

commercial paper market by selling assets to the conduit that

funds the purchase by issuing commercial paper to third

parties. The Group supplies certain services and contingent

liquidity support to some or all of these vehicles on an arm’s

length basis as well as programme credit enhancement. Other

client securitisations arranged by the Group involve individual

SPVs established to purchase customer assets financed by the

issue of debt obligations to third parties. The Group may act

as advisor to the manager of the SPV and provide liquidity

facilities to it.

Under UK GAAP the Group accounts for fees received from

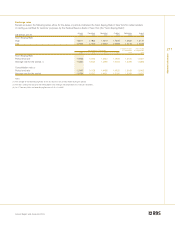

client securitisations in line with its usual policy for similar fees

from other banking activities. Undrawn liquidity lines are

included within undrawn commitments in Note 41 on page 179;

any drawn amounts will be included in loans and advances.

The assets and liabilities of the SPVs are not recognised on the

Group’s balance sheet unless the SPV is a quasi-subsidiary of

the Group. A quasi-subsidiary is defined in FRS 5 as ‘a

company, trust, partnership or other vehicle, that, though not

fulfilling the definition of a subsidiary, is directly or indirectly

controlled by the reporting entity and gives rise to benefits for

that entity that are in substance no different from those that

would arise were the vehicle a subsidiary’.

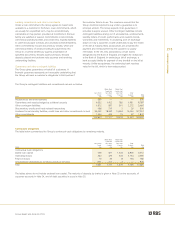

Following the issue of FASB Interpretation (“FIN”) No. 46 (revised),

the Group has consolidated SPVs acting as commercial paper

conduits and involved in other asset-backed transactions in its

US GAAP disclosures. Applying FIN 46R has resulted in total

assets on a US GAAP basis increasing by £6.9 billion. Further

information on FIN 46R can be found in Note 53 on page 198.

Additional information