RBS 2003 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

Annual Report and Accounts 2003

137

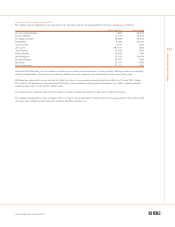

Accounting policies

The accounts have been prepared in accordance with applicable

Accounting Standards in the UK and the Statements of

Recommended Accounting Practice issued by the British

Bankers’ Association and by the Finance and Leasing

Association. The Statement of Recommended Practice issued

by the Association of British Insurers (1998) has been followed

by the insurance members of the Group; they have been

consolidated in the recognised manner for banking groups, in

particular, by using the embedded value method for life business.

A summary of the more important accounting policies is set

out below. The consolidated accounts are prepared in

accordance with the special provisions of Part VII of the

Companies Act 1985 (“the Act”) relating to banking groups.

The accounts of the company are prepared in accordance

with section 226 of, and Schedule 4 to, the Act and, as

permitted by section 230(3) of the Act, no profit and loss

account is presented.

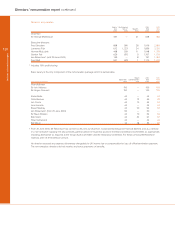

1 Accounting convention and bases of consolidation

The accounts are prepared under the historical cost

convention modified by the periodic revaluation of premises

and certain investments. To avoid undue delay in the

presentation of the Group’s accounts, the accounts of certain

subsidiary undertakings have been made up to 30 November.

There have been no changes in respect of these subsidiary

undertakings, in the period from their balance sheet dates to

31 December, that materially affect the view given by the

Group’s accounts.

2 Revenue recognition

Interest is credited to the profit and loss account as it accrues

unless there is significant doubt that it can be collected (as

described in the accounting policy on loans and advances).

Fees in respect of services are recognised as the right to

consideration accrues through performance to customers.

Services are in respect of financial services related products,

the arrangement is generally contractual, the cost of providing

this service is incurred as the service is rendered and the

price is usually fixed and always determinable.

The application of the Group’s policy to significant fee types is

outlined below.

Loan origination fees: up-front lending fees are recognised as

income when receivable except where they are charged in lieu

of interest or charged to cover the cost of a continuing service

to the borrower, in which case they are credited to income over

the life of the advance.

Commitment and utilisation fees: these are generally

determined as a percentage of the outstanding used or

unused facility. They are usually charged to the customer in

arrears and recognised when charged.

Payment services: this comprises income received for payment

services including cheques cashed, direct debits, Clearing

House Automated Payments (the UK electronic settlement

system) and BACS payments (the automated clearing house

that processes direct debits and direct credits). These are

generally charged on a per transaction basis. The income is

earned when the payment or transaction occurs. Payment

services income is usually charged to the customer’s account,

monthly or quarterly in arrears. Accruals are raised for services

provided but not charged at period end.

Card related services: fees from credit card business include:

Commission received from retailers for processing credit

and debit card transactions: income is accrued to the profit

and loss account as the service is performed.

Interchange received: as issuer, the Group receives a fee

(interchange) each time a cardholder purchases goods and

services. The Group also receives interchange fees from

other card issuers for providing cash advances through its

branch and Automated Teller Machine networks. These fees

are accrued once the transaction has taken place.

An annual fee payable by a credit card holder is charged at

the beginning of each year but is deferred and taken to

income over the period of the service i.e. 12 months.

Insurance brokerage: this is made up of fees and commissions

received from the agency sale of insurance. Commission on

the sale of an insurance contract is earned at the inception of

the policy as the insurance has been arranged and placed.

However, provision is made where commission is refundable in

the event of policy cancellation in line with estimated

cancellations.

Securities and derivatives held for trading are recorded at fair

value. Changes in fair value are recognised in dealing profits

together with dividends from, and interest receivable and

payable on, trading business assets and liabilities.

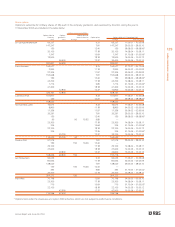

3 Goodwill

Goodwill is the excess of the cost of acquisition of subsidiary

and associated undertakings over the fair value of the Group’s

share of net tangible assets acquired. Goodwill arising on

acquisitions of subsidiary and associated undertakings after 1

October 1998 is capitalised on the balance sheet and

amortised on a straight-line basis over its estimated useful

economic life, currently over periods up to 20 years.

Capitalised goodwill is reviewed for impairment at the end of

the first full year following an acquisition and subsequently if

events or changes in circumstances indicate that its carrying

value may not be recoverable in full. Goodwill arising on

acquisitions of subsidiary and associated undertakings prior to

1 October 1998, previously charged directly against profit and

loss account reserves, was not reinstated under the transitional

provisions of FRS 10 ‘Goodwill and Intangible Assets’. It will be

written back only on disposal and reflected in the calculation of

the gains or losses arising.

Accounting policies