RBS 2003 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

Operating and financial review continued

84

Operating and financial review

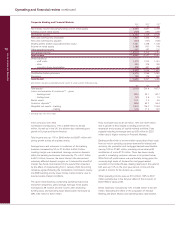

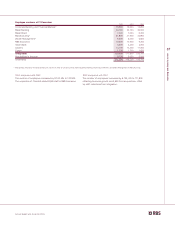

Ulster Bank

2003 2002 2001

£m £m £m

Net interest income 396 339 313

Non-interest income 185 181 170

Total income 581 520 483

Expenses

– staff costs 164 145 135

– other 112 109 104

276 254 239

Contribution before provisions 305 266 244

Provisions 32 22 15

Contribution 273 244 229

£bn £bn £bn

Total assets 15.6 12.7 10.8

Loans and advances to customers – gross 11.6 9.1 7.6

Customer deposits 9.7 8.8 7.7

Weighted risk assets 11.0 9.0 7.7

Average exchange rate – /£ 1.445 1.591 1.609

Spot exchange rate – /£ 1.416 1.536 1.637

2003 compared with 2002

Contribution increased by 12% or £29 million to £273 million

driven by strong volume growth in both loan and deposit products.

The number of customers increased in 2003 by 36,000.

Total income increased by 12% or £61 million to £581 million

reflecting the strong volume growth, in particular residential

mortgages.

Net interest income rose by 17% or £57 million to £396 million,

reflecting strong growth in both average customer lending and

deposits which increased by 26% or £2.1 billion, to £10.1

billion and by 13% or £1.0 billion, to £8.9 billion respectively.

Non-interest income increased by £4 million to £185 million.

Strong growth in lending, transmission and card fee income

was partially offset by lower dealing profits. Uncertainty in

equity markets adversely affected brokerage fees in the

stockbroking business which was sold in October 2003.

Expenses increased by 9% or £22 million to £276 million. This

reflected the annual pay award and the additional costs to

support increased business volumes.

The charge for provisions for bad debts was up £10 million to

£32 million reflecting growth in lending.

2002 compared with 2001

Contribution increased by 7%, or £15 million to £244 million.

Total income increased by 8%, £37 million to £520 million.

Net interest income rose by 8% or £26 million to £339 million,

reflecting good growth in loans and deposits despite a less

buoyant economic environment in the Republic of Ireland.

Average customer lending and deposits of the banking business

increased by 10%, £0.7 billion, to £8.0 billion, and by 7%, £0.5

billion, to £7.9 billion respectively. Average mortgage lending

grew by 23% to £1.5 billion and the number of current

accounts increased by 5%.

Non-interest income rose by 6% or £11 million to £181 million.

Increases of £7 million in net fees and commissions and £6

million in other operating income were partially offset by a £2

million reduction in dealing profits.

Expenses increased by 6% or £15 million to £254 million to

support higher business volumes and pay awards.

Provisions were up by £7 million to £22 million reflecting a

small number of specific situations.