RBS 2003 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

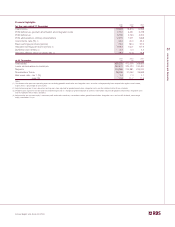

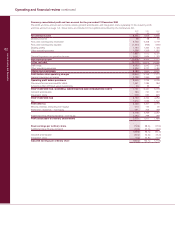

57

Operating and financial review

Annual Report and Accounts 2003

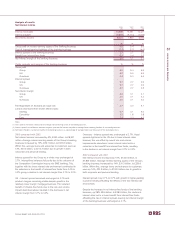

Critical accounting policies

The reported results of the Group are sensitive to the accounting

policies, assumptions and estimates that underlie the preparation

of its financial statements. The Group’s principal accounting

policies are set out on pages 137 to 140. UK company law and

accounting standards require the directors, in preparing the

Group’s financial statements, to select suitable accounting

policies, apply them consistently and make judgements and

estimates that are reasonable and prudent. Where UK GAAP

allows a choice of policy, Financial Reporting Standard (“FRS”)

18 ‘Accounting Policies’ requires an entity to adopt those

policies judged to be most appropriate to its particular

circumstances for the purpose of giving a true and fair view.

The judgements and assumptions involved in the Group’s

accounting policies that are most important to the portrayal of

its financial condition are discussed below. The use of

estimates, assumptions or models that differ from those

adopted by the Group would affect its reported results.

Provisions for bad and doubtful debts

The Group provides for losses existing in its lending book so

as to state its impaired loan portfolio at its expected ultimate

net realisable value. Specific provisions are established against

individual exposures and the general provision covers

advances impaired at the balance sheet date but which have

not been identified as such. Bad and doubtful debt provisions

made during the year less amounts released and recoveries of

amounts written-off in previous years are charged to the profit

and loss account. Loans and advances are reported on the

balance sheet net of specific and general provisions.

For certain homogeneous portfolios, including credit card

receivables and other personal advances including mortgages,

specific provisions are established on a portfolio basis, taking

into account the level of arrears, security, past loss experience,

credit scores and defaults based on portfolio trends. The most

significant factors in establishing these provisions are the

expected loss rates and the related average life. These factors

are kept under constant review by the Group.

For loans and advances that are individually assessed, the

specific provision is determined from a review of the financial

condition of the borrower and any guarantor and takes into

account the customer’s debt capacity and financial flexibility;

the level and quality of earnings; the amount and sources of

cash flows; the industry in which the customer operates; and

the realisable value of any security held. The most significant

estimates that affect the quantum of a specific provision are

the amounts and timing of receipts from the borrower and the

amount that will be recovered from any security held.

Evaluating these estimates involves significant judgement as

receipts will depend on the future performance of the borrower

and the value of security, both of which will be affected by

future economic conditions. Additionally, the security may not

be readily marketable.

The general provision covers bad and doubtful debts that have

not been separately identified at the balance sheet date but

are known to be present in any portfolio of advances. The level

of general provision is assessed in the light of past experience

and reflects the size and diversity of the Group’s loan portfolio,

the current state of the economies in which the Group operates,

other factors affecting the business environment, recent trends

in companies going into administration, receivership and

bankruptcy and the Group’s monitoring and control procedures,

including the scope of specific provisioning procedures.

The future credit quality of the Group’s lending book is subject

to uncertainties that could cause actual credit losses to differ

materially from reported loan loss provisions. These

uncertainties include the economic environment, notably

interest rates and their effect on customer spending, the

unemployment level, payment behaviour and bankruptcy trends

and changes in the Group’s portfolios.

Loans and advances – recognition of interest income

Where the collectibility of interest is in doubt it is excluded

from the profit and loss account but is credited to an interest in

suspense account. As interest charged to overdraft accounts

loses its identity, the determination of the collectibility is

generally achieved through individual file reviews. However, for

some products, such as personal loans and credit cards,

suspension of interest is automated based on the number of

payments in arrears. Such automated suspension of interest

may be accelerated in the event of death, bankruptcy, legal

proceedings or financial hardship. Notwithstanding any

arrears, where it is established that the customer is able to

cover interest, it is credited to the profit and loss account.

Loans classified as impaired and any related suspended

interest are written-down to their estimated net realisable value

when it is determined that there is no realistic prospect of

recovery of all or part of the loan.