RBS 2003 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

Operating and financial review continued

76

Operating and financial review

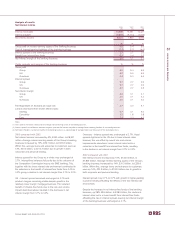

Corporate Banking and Financial Markets

2003 2002* 2001*

£m £m £m

Net interest income excluding funding cost of rental assets 2,653 2,631 2,338

Funding cost of rental assets (329) (282) (200)

Net interest income 2,324 2,349 2,138

Fees and commissions receivable 1,537 1,394 1,250

Fees and commissions payable (220) (157) (165)

Dealing profits (before associated direct costs) 1,661 1,338 1,349

Income on rental assets 1,088 931 748

Other operating income 307 197 137

Non-interest income 4,373 3,703 3,319

Total income 6,697 6,052 5,457

Direct expenses

– staff costs 1,410 1,230 1,091

– other 394 375 350

– operating lease depreciation 518 461 434

2,322 2,066 1,875

Contribution before provisions 4,375 3,986 3,582

Provisions 755 725 502

Contribution 3,620 3,261 3,080

* prior periods have been restated following the transfer of certain activities to Manufacturing

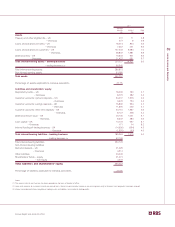

£bn £bn £bn

Total assets** 219.0 203.4 187.7

Loans and advances to customers** – gross

– banking book 99.3 92.1 82.7

– trading book 5.0 3.6 1.0

Rental assets 10.1 7.0 5.5

Customer deposits** 68.6 62.2 56.4

Weighted risk assets – banking 140.0 125.2 105.8

Weighted risk assets – trading 12.6 11.3 12.5

** excluding repos and reverse repos

2003 compared with 2002

Contribution increased by 11% or £359 million to £3,620

million. As well as in the UK, the division also achieved good

growth in Europe and North America.

Total income was up 11% or £645 million to £6,697 million with

strong growth across all business areas.

Average loans and advances to customers of the banking

business increased by 9% or £7.5 billion to £94.3 billion.

Lending margin was maintained. Average customer deposits

within the banking businesses increased by 7% or £4.1 billion

to £61.0 billion; however, the lower interest rate environment

adversely affected deposit margins as it reduced the benefit of

interest free funds. Net interest income was further impacted

by the effect of implementing from 1 January 2003 the pricing

remedies agreed following the Competition Commission inquiry

into SME banking and by lower money market income, due to

less favourable market conditions.

The asset rental business comprising operating leases and

investment properties, grew strongly. Average rental assets

increased to £8.1 billion and net income after deducting

funding costs and operating lease depreciation increased by

28%, £53 million to £241 million.

Fees receivable rose by £143 million, 10% to £1,537 million

due to growth in fees related to lending and from the

expansion and success of capital markets activities. Fees

payable including brokerage were up £63 million to £220

million due to higher volumes in Financial Markets.

Dealing profits which is income before associated direct costs

from our role in servicing customer demand for interest and

currency rate protection and mortgage backed securitisation

rose by 24% to £1,661 million providing incremental profit

contribution of some £170 million. There has been steady

growth in underlying customer volumes in all product areas.

While first half performance was particularly strong given the

unusually high levels of demand for mortgage backed

securities in the United States, dealing revenues in the second

half were up 10% on the prior year period, in line with the

growth in income for the division as a whole.

Other operating income was up £110 million, 56% to £307

million partially due to the full year effect of the inclusion of

Dixon Motors’ gross profit.

Direct expenses increased by 12% or £256 million to £2,322

million. Excluding the effect of the acquisition of Nordisk

Renting and Dixon Motors and operating lease depreciation,