RBS 2003 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

|

|

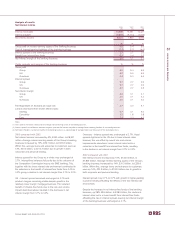

Operating and financial review continued

60

Operating and financial review

and ability to hold to maturity. Trading financial assets are held

for the purpose of selling in the near term. IFRS allows any

financial asset to be designated as fair value through profit and

loss on initial recognition. Unquoted debt financial assets that

are not classified as held-to-maturity, held for trading or

designated as fair value through profit or loss are categorised

as loans and receivables. All other financial assets are

classified as available-for-sale.

Effective interest rate and lending fees – under UK GAAP, loan

origination fees are recognised when receivable unless they

are charged in lieu of interest. IFRS requires origination fees to

be deferred and recognised as an adjustment to the effective

interest rate on the related financial asset. The effective interest

rate is the rate that discounts estimated future cash flows over

an instrument’s expected life to its net carrying value. It takes

into account all fees and points paid that are an integral part of

the yield, transaction costs and all other premiums and

discounts. Under IFRS, the carrying value of a financial

instrument held at amortised cost is calculated using the

effective interest method.

Loan impairment – under UK GAAP, provisions for bad and

doubtful debts are made so as to record impaired loans at their

ultimate net realisable value. IFRS require impairment losses

on financial assets carried at amortised cost to be measured

as the difference between the asset’s carrying amount and the

present value of estimated future cash flows discounted at the

asset’s original effective interest rate. Impairment must be

assessed individually for individually significant assets but can

be assessed collectively for other assets.

Financial instruments: financial liabilities – IFRS require all

financial liabilities to be measured at amortised cost except

those held for trading and those that were designated as fair

value through profit and loss on initial recognition. Under UK

GAAP, short positions in securities and trading derivatives are

carried at fair value, all other financial liabilities are recorded at

amortised cost.

Liabilities and equity – under UK GAAP, all issued shares are

classified as shareholders’ funds, and analysed between equity

and non-equity interests. There is no concept of non-equity

shares in IFRS. Instruments are classified between equity and

liabilities in accordance with the substance of the contractual

arrangements. A non-derivative instrument is classified as equity

if it does not include a contractual obligation either to deliver

cash or to exchange financial instruments with another entity

under potentially unfavourable conditions, and if the instrument

will or may be settled by the issue of equity, settlement does

not involve the issue of a variable number of shares.

Derivatives and hedging – under UK GAAP, non-trading

derivatives are accounted for on an accruals basis in

accordance with the accounting treatment of the underlying

transaction or transactions being hedged. If a non-trading

derivative transaction is terminated or ceases to be an effective

hedge, it is re-measured at fair value and any gain or loss

amortised over the remaining life of the underlying transaction

or transactions being hedged. If a hedged item is

derecognised the related non-trading derivative is remeasured

at fair value and any gain or loss taken to the profit and loss

account. Under IFRS, all derivatives are measured at fair value.

Hedge accounting is permitted for three types of hedge

relationship: fair value hedge – the hedge of changes in the

fair value of a recognised asset or liability or firm commitment;

cash flow hedge - the hedge of variability in cash flows from a

recognised asset or liability or a forecast transaction; and the

hedge of a net investment in a foreign entity. In a fair value

hedge the gain or loss on the derivative is recognised in the

profit and loss account as it arises offset by the corresponding

gain or loss on the hedged item attributable to the risk hedged.

In a cash flow hedge and in the hedge of a net investment in a

foreign entity, the element of the derivative’s gain or loss that is

an effective hedge is recognised directly in equity. The

ineffective element is taken to the profit and loss account.

Certain conditions must be met for a relationship to qualify for

hedge accounting. These include designation, documentation

and prospective and actual hedge effectiveness.

Offset – for a financial asset and financial liability to be offset,

IFRS require that an entity must intend to settle on a net basis

or to realise the asset and settle the liability simultaneously.

However, under UK GAAP an intention to settle net is not a

requirement for set off, although the entity must have the ability to

insist on net settlement and that ability is assured beyond doubt.

Leasing – under UK GAAP, finance lease income is recognised

so as to give a level rate of return on the net cash investment

in the lease. IFRS require a level rate of return on the net

investment in the lease. This means that under UK GAAP tax

cash flows are taken into account in allocating income but they

are not under IFRS.

US GAAP

For a discussion of recent developments in US GAAP relevant

to the Group, see Note 53 on the accounts.