RBS 2003 Annual Report Download - page 229

Download and view the complete annual report

Please find page 229 of the 2003 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230

|

|

227

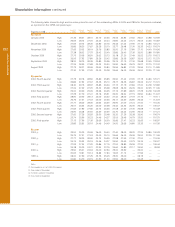

Shareholder information

Annual Report and Accounts 2003

(unless the Inland Revenue directs otherwise). Where interest

has been paid under deduction of UK withholding tax, US

Holders may be able to recover the tax deducted under the Treaty.

If interest were paid under deduction of UK income tax (e.g. if

the PROs lost their listing), US Holders may be able to claim a

refund of the tax deducted under the Treaty.

Any paying agent or other person by or through whom interest

is paid to, or by whom interest is received on behalf of, an

individual, may be required to provide information in relation to

the payment and the individual concerned to the UK Inland

Revenue. The Inland Revenue may communicate this

information to the tax authorities of other jurisdictions.

The UK Inland Revenue confirmed at around the time of the

issue of the PROs that interest payments would not be treated

as distributions for UK tax purposes (i) by reason of the fact

that interest may be deferred under the terms of issue or (ii) by

reason of the undated nature of the PROs, provided that at the

time an interest payment is made, the PROs are not held by a

company which is ‘associated’ with the company or by a

‘funded company’. A company will be associated with the

company if, broadly speaking, it is part of the same group as

the company. A company will be a ‘funded company’ for these

purposes if there are arrangements involving that company

being put in funds (directly or indirectly) by the company, or an

entity associated with the company. In this respect, the Inland

Revenue has confirmed that a company holding an interest in

the PROs which incidentally has banking facilities with any

company associated with the company will not be a ‘funded

company’ by virtue of such facilities.

Interest on the PROs constitutes UK source income for tax

purposes and, as such, may be subject to income tax by

direct assessment even where paid without withholding.

However, interest with a UK source received without deduction

or withholding on account of UK tax will not be chargeable to

UK tax in the hands of a US Holder unless, in the case of a

corporate US Holder, such US Holder carries on a trade in the

UK through a UK permanent establishment or in the case of

other US Holders, such persons carry on a trade, profession or

vocation in the UK through a UK branch or agency in

connection with which the interest is received or to which the

PROs are attributable. There are exemptions for interest

received by certain categories of agent (such as some brokers

and investment managers).

EU Directive on taxation of savings income

The European Union has adopted a new directive regarding

the taxation of savings income. Subject to a number of

important conditions being met, Member States of the

European Union will be required from a date not earlier than 1

January 2005 to provide to the tax authorities of another

Member State details of payments of interest or other similar

income paid by a person within its jurisdiction to an individual

resident in that other Member State, except that Belgium,

Luxembourg and Austria will instead operate a withholding

system for a transitional period in relation to such payments

unless during such period they elect otherwise.

Disposal (including redemption)

A disposal (including redemption) of PROs by a US Holder,

who is an individual or other non corporation tax payer, will not

give rise to any liability to UK taxation on capital gains unless

the US Holder carries on a trade (which for this purpose

includes a profession or a vocation) in the UK through a

branch or agency and the PROs are, or have been, held or

acquired for the purposes of that trade, branch or agency.

A transfer of PROs by a US Holder will not give rise to a

charge to UK tax on accrued but unpaid interest payments,

unless the US Holder is an individual or other non corporation

tax payer and at any time in the relevant year of assessment or

accounting period carries on a trade in the UK through a

branch or agency to which the PROs are attributable.

Annual tax charges

Corporate holders of PROs may be subject to annual UK tax

charges (or relief) by reference to fluctuations in exchange

rates and in respect of profits, gains and losses arising from

the PROs, in place of the tax treatment referred to in the two

preceding paragraphs but only if such corporate US Holders

carry on a trade, profession or vocation in the UK through a

UK permanent establishment to which the PROs are

attributable.

Inheritance tax

In relation to PROs held through DTC (or any other clearing

system), the UK inheritance tax position is not free from doubt

in respect of a lifetime transfer, or death of, a US Holder who is

not domiciled nor deemed to be domiciled in the UK for

inheritance tax purposes; the UK Inland Revenue are known to

consider that the situs of securities held in this manner is not

necessarily determined by the place where the securities are

registered. In appropriate circumstances, there may be a

charge to UK inheritance tax as a result of a lifetime transfer at

less than fair market value by, or on the death of, such a US

Holder. However, exemption from, or a reduction of, any such

UK tax liability may be available under the Estate Tax Treaty.

US Holders should consult their professional advisers in

relation to such potential liability.

Stamp duty and SDRT

No stamp duty, SDRT or similar tax is imposed in the UK on the

issue, transfer or redemption of the PROs.

Exchange controls

The company has been advised that there are currently no UK

laws, decrees or regulations which would prevent the remittance

of dividends or other payments to non-UK resident holders of

the company’s non-cumulative dollar preference shares.

There are no restrictions under the articles of association of

the company or under UK law, as currently in effect, which limit

the right of non-UK resident owners to hold or, when entitled to

vote, freely to vote the company’s non-cumulative dollar

preference shares.