BB&T 2012 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

90

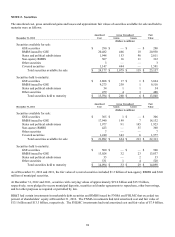

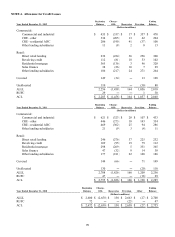

BB&T also maintains reserves for collective impairment that reflect an estimate of losses related to non-impaired commercial

loans as of the balance sheet date. Embedded loss estimates for BB&T’ s commercial loan portfolio are based on estimated

migration rates, which are estimated based on historical experience, and current risk mix as indicated by the risk grading

process described above. Embedded loss estimates may be adjusted to reflect current economic conditions and current

portfolio trends including credit quality, concentrations, aging of the portfolio, and significant policy and underwriting

changes.

Retail

The majority of the ALLL related to the retail lending portfolio is calculated on a collective basis using a delinquency-based

approach. Embedded loss estimates for BB&T’ s retail lending portfolio are based on estimated migration rates that are

developed based on historical experience, and current risk mix as indicated by prevailing delinquency rates. These estimates

may be adjusted to reflect current economic conditions and current portfolio trends. The remaining portion of the allowance

related to the retail lending portfolio relates to loans that have been deemed impaired based on their classification as a TDR at

the balance sheet date. BB&T establishes specific reserves related to these TDRs using an expected cash flow approach. The

allowance for retail TDRs is based on discounted cash flow analyses that incorporate adjustments to future cash flows that

reflect management’ s best estimate of the default risk related to TDRs based on a combination of historical experience and

management judgment.

Acquired Loans

Purchased impaired loans and all loans acquired in an FDIC-assisted transaction are typically aggregated into loan pools

based upon common risk characteristics. The ALLL for each loan pool is based on an analysis that is performed each period

to estimate the expected cash flows. To the extent that the expected cash flows of a loan pool have decreased since the

acquisition date, BB&T establishes an allowance for loan losses. For non-FDIC assisted purchased non-impaired loans,

BB&T uses an approach consistent with that described above for originated loans and leases.

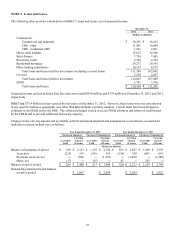

Covered Assets and Related FDIC Loss Share Receivable

Assets subject to loss sharing agreements with the FDIC are labeled “covered” and include certain loans, securities and other

assets.

The FDIC’ s obligation to reimburse Branch Bank for losses with respect to covered assets begins with the first dollar of loss

incurred. The terms of the loss sharing agreement with respect to certain non-agency RMBS provides that Branch Bank will

be reimbursed by the FDIC for 95% of any and all losses. All other covered assets are subject to a stated threshold of $5

billion that provides for the FDIC to reimburse Branch Bank for (1) 80% of losses incurred up to $5 billion and (2) 95% of

losses in excess of $5 billion. Gains and recoveries on covered assets will offset losses, or be paid to the FDIC, at the

applicable loss share percentage at the time of recovery. The loss sharing agreement applicable to single family residential

mortgage loans expires in 2019, and provides for FDIC loss sharing and Branch Bank reimbursement to the FDIC. The loss

sharing agreement applicable to commercial loans and other covered assets expires in 2014, however, Branch Bank must

reimburse the FDIC for realized gains and recoveries through August 2017. At the conclusion of the loss share period should

actual aggregate losses, excluding securities, be less than an amount determined in accordance with these agreements, BB&T

will pay the FDIC a portion of the difference.

The income statement effect of the changes in the FDIC loss share receivable includes the accretion due to discounting and

changes in expected net reimbursements. Decreases in expected net reimbursements, including the amounts expected to be

paid to the FDIC as a result of the aggregate losses calculation, are recognized in income prospectively over the term of the

loss share agreements consistent with the approach taken to recognize increases in cash flows on covered loans. Increases in

expected reimbursements are recognized in income in the same period that the ACL for the related loans is recognized.

Premises and Equipment

Premises, equipment, capital leases and leasehold improvements are stated at cost less accumulated depreciation and

amortization. Land is stated at cost. In addition, purchased software and costs of computer software developed for internal

use are capitalized provided certain criteria are met. Depreciation and amortization are computed principally using the

straight-line method over the estimated useful lives of the related assets. Leasehold improvements are amortized on a

straight-line basis over the lesser of the lease terms, including certain renewals that were deemed probable at lease inception,

or the estimated useful lives of the improvements. Capitalized leases are amortized by the same methods as premises and

equipment over the estimated useful lives or lease terms, whichever is less. Obligations under capital leases are amortized

using the interest method to allocate payments between principal reduction and interest expense. Rent expense and rental

income on operating leases is recorded using the straight-line method over the appropriate lease terms.