BB&T 2012 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

56

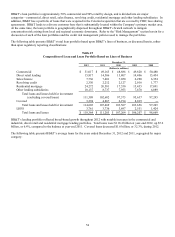

aggressive approach to reducing the inventory of foreclosed property that was implemented during the fourth quarter of 2011.

The current inventory of foreclosed real estate as of December 31, 2012 includes land and lots, totaling $35 million that have

been held for approximately 15 months on average. The remaining foreclosed real estate of $72 million, which is primarily

single family residential and commercial real estate, had an average holding period of seven months. NPAs as a percentage

of loans and leases plus foreclosed property were 1.33% at December 31, 2012 compared with 2.29% at December 31, 2011.

Management expects NPAs to improve at a modest pace during the first quarter of 2013, assuming no significant economic

deterioration during the quarter.

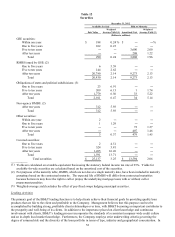

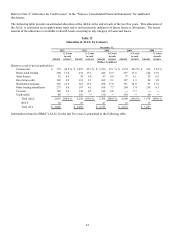

The following table presents the changes in NPAs during 2012 and 2011.

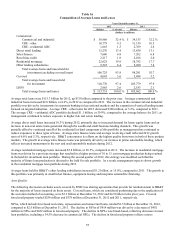

Table 17

Rollforward of NPAs

Years Ended December 31,

2012 2011

(Dollars in millions)

Balance at beginning of year $ 2,450 $ 3,971

N

ew NPAs 2,449 3,216

Advances and principal increases 161 120

Disposals of foreclosed property (737) (1,062)

Loan sales (1) (754) (1,139)

Charge-offs and losses (1,002) (1,719)

Payments (669) (634)

Transfers to performing status (392) (303)

Other, net 30 ―

Balance at end of year $ 1,536 $ 2,450

(1) Includes charge-offs and losses recorded upon sale of $219 million and $241 million for the years ended December 31,

2012 and 2011, respectively.

Tables 18 and 19 summarize asset quality information for the past five years. As more fully described below, this

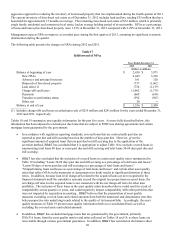

information has been adjusted to exclude past due loans that are subject to FDIC loss sharing agreements and certain

mortgage loans guaranteed by the government:

In accordance with regulatory reporting standards, covered loans that are contractually past due are

reported as past due and still accruing based on the number of days past due. However, given the

significant amount of acquired loans that are past due but still accruing due to the application of the

accretion method, BB&T has concluded that it is appropriate to adjust Table 18 to exclude covered loans in

summarizing total loans 90 days or more past due and still accruing and total loans 30-89 days past due and

still accruing.

BB&T has also concluded that the inclusion of covered loans in certain asset quality ratios summarized in

Table 19 including “Loans 30-89 days past due and still accruing as a percentage of total loans and leases,”

“Loans 90 days or more past due and still accruing as a percentage of total loans and leases,”

“Nonperforming loans and leases as a percentage of total loans and leases” and certain other asset quality

ratios that reflect NPAs in the numerator or denominator (or both) results in significant distortion to these

ratios. In addition, because loan level charge-offs related to the acquired loans are not recognized in the

financial statements until the cumulative amounts exceed the original loss projections on a pool basis, the

net charge-off ratio for the acquired loans is not consistent with the net charge-off ratio for other loan

portfolios. The inclusion of these loans in the asset quality ratios described above could result in a lack of

comparability across quarters or years, and could negatively impact comparability with other portfolios that

were not impacted by acquisition accounting. BB&T believes that the presentation of asset quality

measures excluding covered loans and related amounts from both the numerator and denominator provides

better perspective into underlying trends related to the quality of its loan portfolio. Accordingly, the asset

quality measures in Table 19 present asset quality information both on a consolidated basis as well as

excluding the covered assets and related amounts.

In addition, BB&T has excluded mortgage loans that are guaranteed by the government, primarily

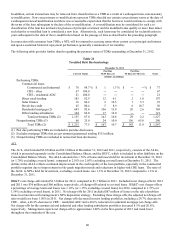

FHA/VA loans, from the asset quality metrics and ratios reflected on Tables 18 and 19, as these loans are

recoverable through various government guarantees. In addition, BB&T has recorded on the balance sheet