BB&T 2012 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

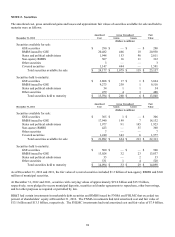

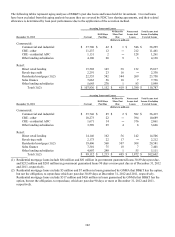

96

Less than 12 months 12 months or more Total

Fair Unrealized Fair Unrealized Fair Unrealized

December 31, 2011 Value Losses Value Losses Value Losses

(Dollars in millions)

Securities available for sale:

RMBS issued by GSE $ 3,098 $ 7 $ — $ — $ 3,098 $ 7

States and political subdivisions 16 3 702 142 718 145

N

on-agency RMBS — — 368 55 368 55

Covered securities 29 6 — — 29 6

Total $ 3,143 $ 16 $ 1,070 $ 197 $ 4,213 $ 213

Securities held to maturity:

RMBS issued by GSE $ 7,770 $ 23 $ — $ — $ 7,770 $ 23

States and political subdivisions 33 2 — — 33 2

Other securities 207 4 — — 207 4

Total $ 8,010 $ 29 $ — $ — $ 8,010 $ 29

BB&T conducts periodic reviews to identify and evaluate each investment with an unrealized loss for OTTI. An unrealized

loss exists when the current fair value of an individual security is less than its amortized cost basis. Unrealized losses that are

determined to be temporary in nature are recorded, net of tax, in AOCI for available-for-sale securities.

Factors considered in determining whether a loss is temporary include:

The financial condition and near-term prospects of the issuer, including any specific events that may influence the

operations of the issuer;

BB&T’ s intent to sell and whether it is more likely than not that the Company will be required to sell these debt

securities before the anticipated recovery of the amortized cost basis;

The length of time and the extent to which the market value has been less than cost;

Whether the decline in fair value is attributable to specific conditions, such as conditions in an industry or in a

geographic area;

Whether a debt security has been downgraded by a rating agency;

Whether the financial condition of the issuer has deteriorated;

The seniority of the security;

Whether dividends have been reduced or eliminated, or scheduled interest payments on debt securities have not been

made; and

Any other relevant available information.

To the extent that BB&T has identified OTTI and does not intend to sell the security and it is more likely than not that BB&T

will not be required to sell the security prior to recovery, the credit component of the unrealized loss is recognized in earnings

and the non-credit component is recognized in AOCI. In making this determination, BB&T considers its expected liquidity

and capital needs, including its asset/liability management needs, forecasts, strategies and other relevant information.

BB&T uses cash flow modeling to evaluate non-agency RMBS in an unrealized loss position for potential credit impairment.

These models give consideration to long-term macroeconomic factors applied to current security default rates, prepayment

rates and recovery rates and security-level performance. At December 31, 2012, four non-agency RMBS with an unrealized

loss were below investment grade. None of the unrealized losses were significant.

At December 31, 2012, $79 million of unrealized loss on municipal securities was the result of fair value hedge basis

adjustments that are a component of amortized cost. Municipal securities in an unrealized loss position are evaluated for

credit impairment through a qualitative analysis of issuer performance and the primary source of repayment. The evaluation

of municipal securities indicated there were no credit losses evident.