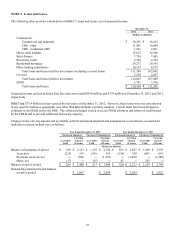

BB&T 2012 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

91

Securities Sold Under Repurchase Agreements

Securities sold under repurchase agreements generally have maturities ranging from 1 day to 36 months. Securities sold

under agreements to repurchase are reflected as collateralized borrowings on the Consolidated Balance Sheets and are

recorded based on the amount of cash received in connection with the borrowing. The terms of repurchase agreements may

require BB&T to provide additional collateral if the fair value of the securities underlying the borrowings declines during the

term of the agreement.

Income Taxes

Deferred income taxes have been provided when different accounting methods have been used in determining income for

income tax purposes and for financial reporting purposes. Deferred tax assets and liabilities are recognized based on future

tax consequences attributable to differences arising from the financial statement carrying values of assets and liabilities and

their tax bases. In the event of changes in the tax laws, deferred tax assets and liabilities are adjusted in the period of the

enactment of those changes, with the cumulative effects included in the current year’ s income tax provision.

Derivative Financial Instruments

A derivative is a financial instrument that derives its cash flows, and therefore its value, by reference to an underlying

instrument, index or referenced interest rate. These instruments include interest rate swaps, caps, floors, collars, financial

forwards and futures contracts, swaptions, when-issued securities, foreign exchange contracts and options written and

purchased. BB&T uses derivatives primarily to manage economic risk related to securities, commercial loans, MSRs and

mortgage banking operations, long-term debt and other funding sources. BB&T also uses derivatives to facilitate

transactions on behalf of its clients. The fair value of derivatives in a gain or loss position is included in other assets or

liabilities, respectively, on the Consolidated Balance Sheets.

BB&T classifies its derivative financial instruments as either (1) a hedge of an exposure to changes in the fair value of a

recorded asset or liability (“fair value hedge”), (2) a hedge of an exposure to changes in the cash flows of a recognized asset,

liability or forecasted transaction (“cash flow hedge”), (3) a hedge of a net investment in a subsidiary, or (4) derivatives not

designated as hedges. Changes in the fair value of derivatives not designated as hedges are recognized in current period

earnings. BB&T has master netting agreements with the derivatives dealers with which it does business, but reflects gross

assets and liabilities on the Consolidated Balance Sheets.

BB&T uses the long-haul method to assess hedge effectiveness. BB&T documents, both at inception and over the life of the

hedge, at least quarterly, its analysis of actual and expected hedge effectiveness. This analysis includes techniques such as

regression analysis and hypothetical derivatives to demonstrate that the hedge has been, and is expected to be, highly

effective in off-setting corresponding changes in the fair value or cash flows of the hedged item. For cash flow hedges

involving interest rate caps and collars, this analysis also includes consideration of whether critical terms match, the strike

price of the hedging option matches the specified level beyond (or within) which the entity’ s exposure is being hedged, the

hedging instrument’ s inflows (outflows) at its maturity date completely offset the change in the hedged transaction’ s cash

flows for the risk being hedged and the hedging instrument can be exercised only on its contractual maturity date. For a

qualifying fair value hedge, changes in the value of the derivatives that have been highly effective as hedges are recognized

in current period earnings along with the corresponding changes in the fair value of the designated hedged item attributable to

the risk being hedged. For a qualifying cash flow hedge, the portion of changes in the fair value of the derivatives that have

been highly effective are recognized in OCI until the related cash flows from the hedged item are recognized in earnings. For

qualifying cash flow hedges involving interest rate caps and collars, the initial fair value of the premium paid is allocated and

recognized in the same future period that the hedged forecasted transaction impacts earnings.

For either fair value hedges or cash flow hedges, ineffectiveness may be recognized in noninterest income to the extent that

changes in the value of the derivative instruments do not perfectly offset changes in the value of the hedged items. If the

hedge ceases to be highly effective, BB&T discontinues hedge accounting and recognizes the changes in fair value in current

period earnings. If a derivative that qualifies as a fair value or cash flow hedge is terminated or the designation removed, the

realized or then unrealized gain or loss is recognized into income over the life of the hedged item (fair value hedge) or period

in which the hedged item affects earnings (cash flow hedge). Immediate recognition in earnings is required upon sale or

extinguishment of the hedged item (fair value hedge) or if it is probable that the hedged cash flows will not occur (cash flow

hedge).

Derivatives used to manage economic risk not designated as hedges primarily represent economic risk management

instruments of MSRs and mortgage banking operations, with gains or losses included in mortgage banking income. In

connection with its mortgage banking activities, BB&T enters into loan commitments to fund residential mortgage loans at

specified rates and for specified periods of time. To the extent that BB&T’ s interest rate lock commitments relate to loans