BB&T 2012 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

74

specified ranges requires the approval of the Federal Housing Finance Agency. Because the extent of any obligation to

increase BB&T’ s investment in the FHLB depends entirely upon the occurrence of a future event, potential future payments

to the FHLB are not determinable.

In the normal course of business, BB&T is also a party to financial instruments to meet the financing needs of clients and to

mitigate exposure to interest rate risk. Such financial instruments include commitments to extend credit and certain

contractual agreements, including standby letters of credit and financial guarantee arrangements. Further discussion of these

commitments is included in Note 15 “Commitments and Contingencies” in the “Notes to Consolidated Financial Statements.”

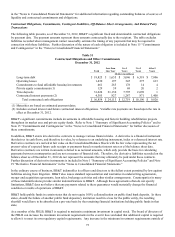

BB&T’ s significant commitments and obligations are summarized in the accompanying table. Not all of the commitments

presented in the table will be used, thus the actual cash requirements are likely to be significantly less than the amounts

reported.

Table 32

Summary of Significant Commitments

December 31, 2012

(Dollars in millions)

Lending commitments $ 43,760

Letters of credit and financial guarantees written 5,164

Total significant commitments $ 48,924

Related Party Transactions

The Company may extend credit to its officers and directors in the ordinary course of business. These loans are made under

substantially the same terms as comparable third-party lending arrangements and are in compliance with applicable banking

regulations.

Capital

The maintenance of appropriate levels of capital is a management priority and is monitored on a regular basis. BB&T’ s

principal goals related to the maintenance of capital are to provide adequate capital to support BB&T’ s risk profile consistent

with the Board-approved risk appetite, provide financial flexibility to support future growth and client needs, comply with

relevant laws, regulations, and supervisory guidance, achieve optimal credit ratings for BB&T and its subsidiaries and

provide a competitive return to shareholders.

Management regularly monitors the capital position of BB&T on both a consolidated and bank level basis. Capital ratios are

determined using operating forecasts and plans as well as stressed scenarios. In this regard, management’ s overriding policy

is to maintain capital at levels that are in excess of the operating capital guidelines, which are above the regulatory “well

capitalized” levels. Management has recently implemented stressed capital ratio minimum guidelines to evaluate whether

capital levels are sufficient to withstand the impact of plausible, severe economic downturns or bank-specific events. The

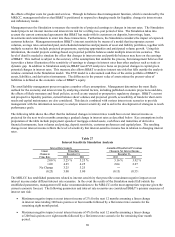

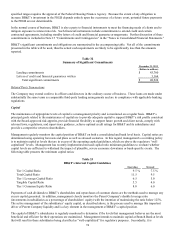

following table presents the minimum capital ratios:

Table 33

BB&T's Internal Capital Guidelines

Operating Stressed

Tier 1 Capital Ratio 9.5 % 7.5 %

Total Capital Ratio 11.5 9.5

Tier 1 Leverage Capital Ratio 6.5 5.0

Tangible Capital Ratio 5.5 4.0

Tier 1 Common Equity Ratio 8.0 6.0

Payments of cash dividends to BB&T’ s shareholders and repurchases of common shares are the methods used to manage any

excess capital generated. In addition, management closely monitors the Parent Company’ s double leverage ratio

(investments in subsidiaries as a percentage of shareholders’ equity) with the intention of maintaining the ratio below 125%.

The active management of the subsidiaries’ equity capital, as described above, is the process used to manage this important

driver of Parent Company liquidity and is a key element in the management of BB&T’ s capital position.

The capital of BB&T’ s subsidiaries is regularly monitored to determine if the levels that management believes are the most

beneficial and efficient for their operations are maintained. Management intends to maintain capital at Branch Bank at levels

that will result in these subsidiaries being classified as “well-capitalized” for regulatory purposes. Secondarily, it is