BB&T 2012 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

36

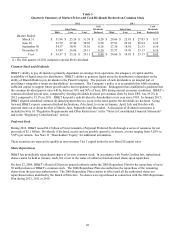

The rates paid on average short-term borrowings declined from 0.28% in 2010 to 0.27% during 2011. At December 31,

2011, the targeted Federal funds rate was a range of zero percent to 0.25%. The average rate on long-term debt during 2011

was 3.40%, a decrease of 56 basis points compared to the prior year. This reduction was due to new issuances at lower rates

and the positive impact of accelerated amortization from certain derivatives that were unwound in a gain position.

Covered Assets and FDIC Loss Share Receivable

In connection with the Colonial acquisition, Branch Bank entered into loss sharing agreements with the FDIC that outline the

terms and conditions under which the FDIC will reimburse Branch Bank for a portion of the losses incurred on certain loans,

OREO, certain investment securities and other assets (collectively, “covered assets”). The FDIC’ s obligation to reimburse

Branch Bank for losses with respect to covered assets begins with the first dollar of loss incurred. The loss sharing

agreement applicable to single family residential mortgage loans expires in 2019. The loss sharing agreement applicable to

commercial loans and other covered assets expires in 2014; however, Branch Bank must reimburse the FDIC for gains and

recoveries through August 2017. The terms of the loss sharing agreement with respect to certain non-agency RMBS provides

that Branch Bank will be reimbursed by the FDIC for 95% of any and all losses. For other covered assets, the FDIC will

reimburse Branch Bank for (1) 80% of losses incurred up to $5 billion and (2) 95% of losses in excess of $5 billion. Gains

and recoveries on covered assets will offset losses, or be paid to the FDIC, at the applicable loss share percentage at the time

of recovery. At the conclusion of the loss share period should actual aggregate losses, excluding securities, be less than an

amount determined in accordance with these agreements, BB&T will pay the FDIC a portion of the difference. The fair

value of the net reimbursement the Company expected to receive from the FDIC under those agreements was recorded as the

FDIC loss share receivable at the date of acquisition. The fair value of the FDIC loss share receivable was estimated using a

discounted cash flow methodology.

Acquired loans were aggregated into separate pools based upon common risk characteristics. Each pool is considered a unit

of account and the cash flows expected to be collected, credit losses and other relevant information are developed for each

pool. A summary of the accounting treatment related to changes in credit losses on each loan pool and the related FDIC loss

share asset follows.

If the estimated credit loss on a loan pool is increased:

o The reduction in the net present value of the loan pool is recognized immediately as provision expense and

an increase to the ALLL.

o The FDIC loss share asset is increased by 80% of the adjustment to the allowance through income.

If the estimated credit loss on a loan pool is reduced:

o If the loan pool has an allowance, the allowance is first reduced to $0 (and 80% of this reduction decreases

the FDIC loss share asset) through income.

o If the loan pool does not have an allowance (or it is first reduced to $0 and there remains additional

expected cash flows), the excess of expected cash flows is recognized as a yield adjustment over the

remaining expected life of the loan.

o The decrease in expected reimbursement from the FDIC is recognized in income prospectively using a

level yield methodology over the remaining life of the loss share agreements.

o The increase in the amount expected to be paid to the FDIC as a result of the aggregate loss calculation is

recognized prospectively using a level yield methodology over the remaining life of the loss share

agreements.

The accounting treatment for covered securities is summarized below:

The discount established at acquisition is accreted over the expected life of the underlying securities using a level

yield methodology.

Changes to the expected life of the securities are recognized with a cumulative adjustment to the accretion

recognized.

OTTI is determined using the same methodology as non-covered securities.