BB&T 2012 Annual Report Download - page 131

Download and view the complete annual report

Please find page 131 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

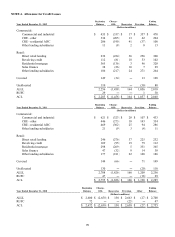

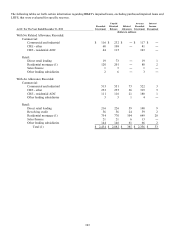

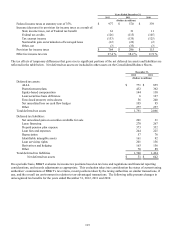

109

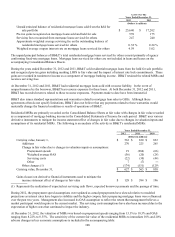

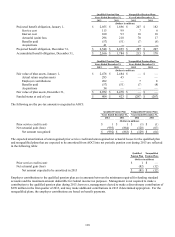

December 31,

2012 2011

(Dollars in millions)

Fair value of residential MSRs $ 627 $ 563

Composition of residential loans serviced for others:

Fixed-rate mortgage loans 99 % 99 %

Adjustable-rate mortgage loans 1 1

Total 100 % 100 %

Weighted average life 4.4 yrs 3.7 yrs

Prepayment speed 17.3 % 20.8 %

Effect on fair value of a 10% increase $ (35) $ (35)

Effect on fair value of a 20% increase (67) (66)

Weighted average OAS 8.3 % 6.9 %

Effect on fair value of a 10% increase $ (17) $ (12)

Effect on fair value of a 20% increase (33) (23)

The sensitivity calculations above are hypothetical and should not be considered to be predictive of future performance. As

indicated, changes in fair value based on adverse changes in assumptions generally cannot be extrapolated because the

relationship of the change in assumption to the change in fair value may not be linear. Also, in the above table, the effect of

an adverse variation in a particular assumption on the fair value of the MSRs is calculated without changing any other

assumption; while in reality, changes in one factor may result in changes in another, which may magnify or counteract the

effect of the change.

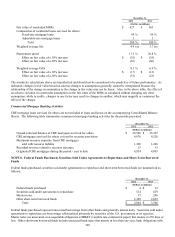

Commercial Mortgage Banking Activities

CRE mortgage loans serviced for others are not included in loans and leases on the accompanying Consolidated Balance

Sheets. The following table summarizes commercial mortgage banking activities for the periods presented:

December 31,

2012 2011

(Dollars in millions)

Unpaid principal balance of CRE mortgages serviced for others $ 29,520 $ 25,367

CRE mortgages serviced for others covered by recourse provisions 4,970 4,520

Maximum recourse exposure from CRE mortgages

sold with recourse liability 1,368 1,226

Recorded reserves related to recourse exposure 13 15

Originated CRE mortgages during the period - year to date 4,934 4,803

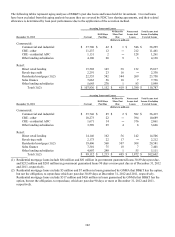

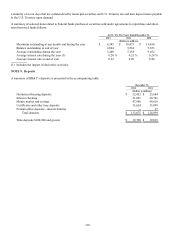

NOTE 8. Federal Funds Purchased, Securities Sold Under Agreements to Repurchase and Short-Term Borrowed

Funds

Federal funds purchased, securities sold under agreements to repurchase and short-term borrowed funds are summarized as

follows:

December 31,

2012 2011

(Dollars in millions)

Federal funds purchased $ 4 $ 12

Securities sold under agreements to repurchase 514 619

Master notes 37 296

Other short-term borrowed funds 2,309 2,639

Total $ 2,864 $ 3,566

Federal funds purchased represent unsecured borrowings from other banks and generally mature daily. Securities sold under

agreements to repurchase are borrowings collateralized primarily by securities of the U.S. government or its agencies.

Master notes are unsecured, non-negotiable obligations of BB&T (variable rate commercial paper) that mature in 270 days or

less. Other short-term borrowed funds include unsecured bank notes that mature in less than one year, bank obligations with