BB&T 2012 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

105

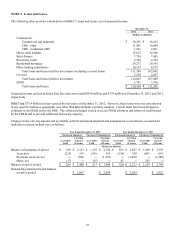

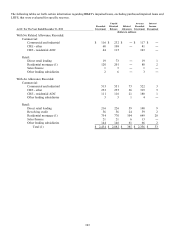

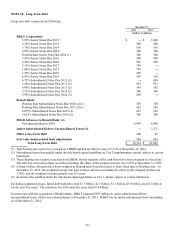

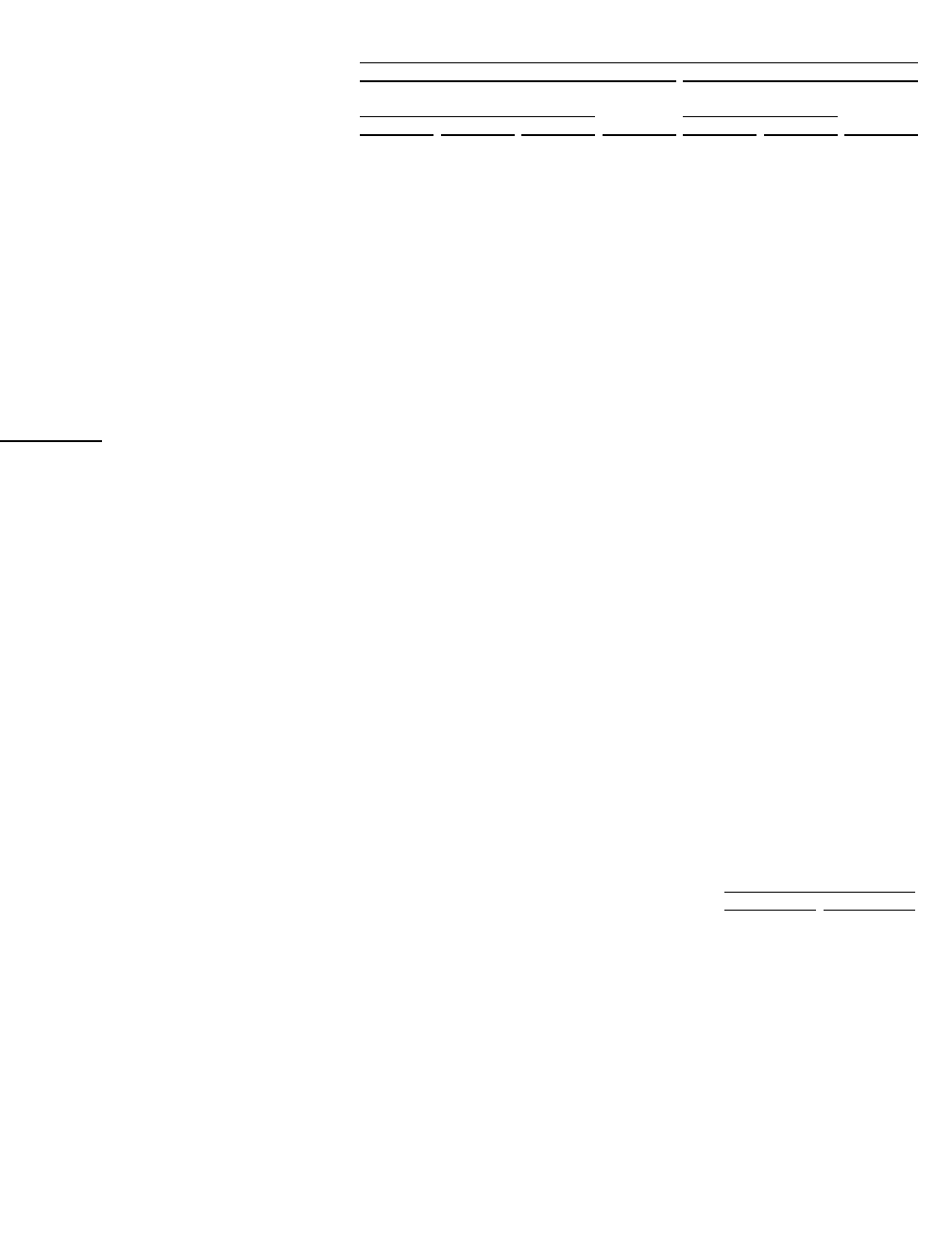

The following tables provide a summary of the primary reason current year loan modifications were classified as TDRs

and their estimated impact on the ALLL:

Years Ended December 31,

2012 2011

Types of Types of

Modifications (1) Impact To Modifications (1) Impact To

Rate (2) Structure Other ALLL Rate (2) Structure ALLL

(Dollars in millions)

Commercial:

Commercial and industrial $ 37 $ 63 $ 14 $ ―$ 29 $ 68 $ 5

CRE - other 60 45 7 ― 56 58 8

CRE - residential ADC 41 34 3 (1) 29 47 10

Other lending subsidiaries ― ― ― ― 1 1 ―

Retail:

Direct retail lending 38 17 82 35 51 5 9

Revolving credit 30 ― ― 5 40 ― 8

Residential mortgage 106 88 135 22 142 35 17

Sales finance 4 ― 12 4 5 5 1

Other lending subsidiaries 106 2 17 35 37 7 15

(1) Includes modifications made to existing TDRs, as well as new modifications that are considered TDRs. Balances

represent the recorded investment as of the end of the period in which the modification was made.

(2) Includes TDRs made with a below market interest rate that also includes a modification of loan structure.

During 2012, a national bank regulatory agency issued guidance that requires certain loans that had been discharged in

bankruptcy and not reaffirmed by the borrower to be accounted for as TDRs and possibly as nonperforming, regardless of

their actual payment history and expected performance. As of December 31, 2012, the Company’ s primary regulators had

not reached a final decision on how this guidance may apply to its regulated entities. BB&T concluded that these loans

should be classified as TDRs and these are included in “Other” in the above table. BB&T has also concluded there is a

reasonable expectation of collection of principal and interest and has classified these loans as performing unless already

classified as nonperforming.

Charge-offs recorded at the modification date were $25 million and $47 million for the year ended December 31, 2012 and

2011, respectively. The forgiveness of principal or interest for TDRs recorded during the year ended December 31, 2012 and

2011 was immaterial.

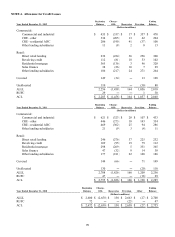

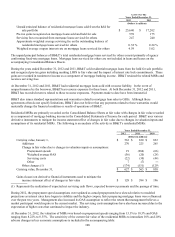

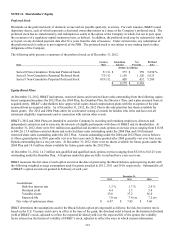

The following table summarizes the pre-default balance for modifications that experienced a payment default that had been

classified as TDRs during the previous 12 months. BB&T defines payment default as movement of the TDR to nonaccrual

status, foreclosure or charge-off, whichever occurs first.

Years Ended December 31,

2012 2011

(Dollars in millions)

Commercial:

Commercial and industrial $ 8 $ 39

CRE - other 6 92

CRE - residential ADC 14 80

Retail:

Direct retail lending 8 16

Revolving credit 12 15

Residential mortgage 36 31

Sales finance ― 2

Other lending subsidiaries 12 5

If a TDR subsequently defaults, BB&T evaluates the TDR for possible impairment. As a result, the related allowance may

be increased or charge-offs may be taken to reduce the carrying value of the loan.