BB&T 2012 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

41

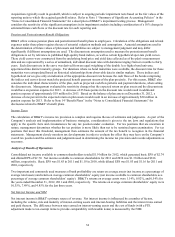

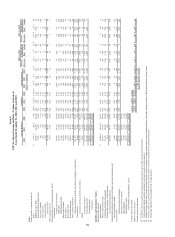

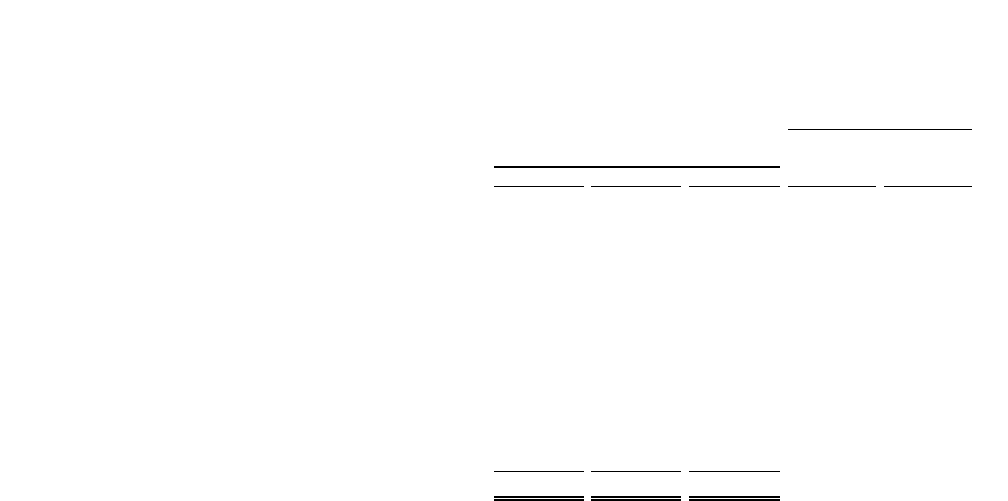

The following table provides a breakdown of BB&T’ s noninterest income:

Table 9

Noninterest Income

% Change

2012 2011

Years Ended December 31, v. v.

2012 2011 2010 2011 2010

(Dollars in millions)

Insurance income $ 1,359 $ 1,044 $ 1,041 30.2 % 0.3 %

Mortgage banking income 840 436 521 92.7 (16.3)

Service charges on deposits 566 563 618 0.5 (8.9)

Investment banking and brokerage fees and commissions 365 333 352 9.6 (5.4)

Bankcard fees and merchant discounts 236 204 177 15.7 15.3

Checkcard fees 185 271 274 (31.7) (1.1)

Trust and investment advisory revenues 184 173 159 6.4 8.8

Income from bank-owned life insurance 116 122 123 (4.9) (0.8)

FDIC loss share income, net (318) (289) (116) 10.0 149.1

Securities gains (losses), net (12) 62 554 (119.4) (88.8)

Other income 299 194 254 54.1 (23.6)

Total noninterest income $ 3,820 $ 3,113 $ 3,957 22.7 (21.3)

2012 compared to 2011

Noninterest income was $3.8 billion for 2012, up 22.7% compared to 2011. This increase was driven by record income

generated by BB&T’ s insurance, mortgage banking and investment banking and brokerage lines of business. In addition,

bankcard fees and merchant discounts and other income increased compared to the prior year. These increases were partially

offset by lower checkcard fees, a decrease in income related to the FDIC loss share receivable and a reduction in net

securities income. The major categories of noninterest income and fluctuations in these amounts are discussed in the

following paragraphs. These fluctuations include the impact of acquisitions.

Income from BB&T’ s insurance agency/brokerage operations was the largest source of noninterest income in 2012.

Insurance income was up 30.2% compared to 2011, primarily due to the acquisition of Crump Insurance on April 2, 2012,

which added approximately $234 million in revenues during 2012. The remainder of the increase in insurance income is

attributable to the impact of other acquisitions that closed during the fourth quarter of 2011 and firming market conditions.

Mortgage banking income totaled $840 million in 2012 compared to $436 million in 2011. The increase in mortgage

banking income was primarily due to an increase in residential mortgage production revenues totaling $378 million, which

was driven by higher gains on residential mortgage production and sales. Included in mortgage banking income for 2012 is a

negative valuation adjustment of $32 million related to changes in assumptions for residential MSRs that are carried at fair

value. Approximately $22 million of the decline in the valuation of the residential MSRs was due to a revision in the

servicing cost assumption based on an expectation of higher costs that continue to impact the industry. The remainder of the

net decrease is primarily due to the impact of an increase in OAS assumption changes partially offset by prepayment speed

changes, which are reflective of the current MSR market. This decrease was more than offset by gains of $128 million from

derivative financial instruments used to manage the economic risk.

Service charges on deposit accounts, which totaled $566 million in 2012, represent BB&T’ s third largest category of

noninterest revenue. Service charge revenues were essentially flat compared to the prior year, reflecting the impact of pricing

changes for routine services related to retail and commercial transaction deposit products, such as monthly maintenance fees

and commercial transaction deposit products, implemented in 2011 that were designed to offset a reduction in service charges

that occurred in 2010 as a result of a change in overdraft policies.

Investment banking and brokerage fees and commissions increased $32 million, or 9.6%, compared to 2011. This increase

was largely driven by a higher level of investment banking activities and higher brokerage fees and commissions. Checkcard

fees decreased $86 million, or 31.7%, due to the Durbin Amendment to the Dodd-Frank Act, which was implemented on

October 1, 2011 and limited the rate banks could assess for debit card transactions. Bankcard fees and merchant discounts

increased $32 million in 2012, primarily the result of higher volumes for both retail and commercial bankcard activities.

FDIC loss share income reflects accretion of the FDIC receivable due to credit loss improvement (including expense

associated with the aggregate loss calculation) and accretion related to covered securities, partially reduced by the offset to