BB&T 2012 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

100

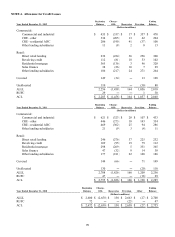

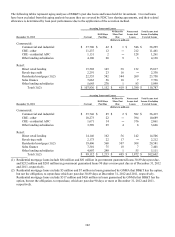

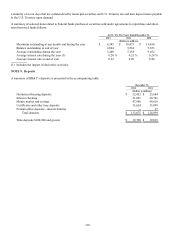

The following tables provide a breakdown of the ALLL and the recorded investment in loans based on the method for

determining the allowance:

ALLL

December 31, 2012 December 31, 2011

Individually Collectively Individually Collectively

Evaluated Evaluated Evaluated Evaluated

for for for for

Impairment Impairment Impairment Impairment

(Dollars in millions)

Commercial:

Commercial and industrial $ 73 $ 397 $ 77 $ 356

CRE - other 36 168 69 265

CRE - residential ADC 21 79 50 236

Other lending subsidiaries 1 12 1 10

Retail:

Direct retail lending 59 241 35 197

Revolving credit 24 78 27 85

Residential mortgage 130 198 152 213

Sales finance 6 23 1 37

Other lending subsidiaries 61 203 20 166

Covered ― 128 ― 149

Unallocated ― 80 ― 110

Total $ 411 $ 1,607 $ 432 $ 1,824

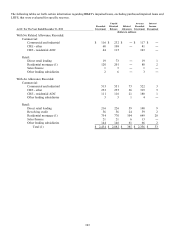

Loans and Leases

December 31, 2012 December 31, 2011

Individually Collectively Individually Collectively

Evaluated Evaluated Evaluated Evaluated

for for for for

Impairment Impairment Impairment Impairment

(Dollars in millions)

Commercial:

Commercial and industrial $ 631 $ 37,664 $ 656 $ 35,759

CRE - other 312 11,149 511 10,178

CRE - residential ADC 155 1,106 420 1,641

Other lending subsidiaries 3 4,135 5 3,621

Retail:

Direct retail lending 235 15,582 165 14,341

Revolving credit 56 2,274 62 2,150

Residential mortgage 1,187 23,085 931 19,650

Sales finance 22 7,714 10 7,391

Other lending subsidiaries 146 5,853 49 5,062

Covered ― 3,294 ― 4,867

Total $ 2,747 $ 111,856 $ 2,809 $ 104,660

BB&T monitors the credit quality of its commercial portfolio segment using internal risk ratings. These risk ratings are

based on established regulatory guidance. Loans with a Pass rating represent those not considered a problem credit. Special

mention loans are those that have a potential weakness deserving management’ s close attention. Substandard loans are those

for which a well-defined weakness has been identified that may put full collection of contractual cash flows at risk.

Substandard loans are placed in nonaccrual status when BB&T believes it is no longer probable it will collect all contractual

cash flows. BB&T assigns an internal risk rating at loan origination and reviews the relationship again on an annual basis or

at any point management becomes aware of information affecting the borrower’ s ability to fulfill their obligations.