BB&T 2012 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

53

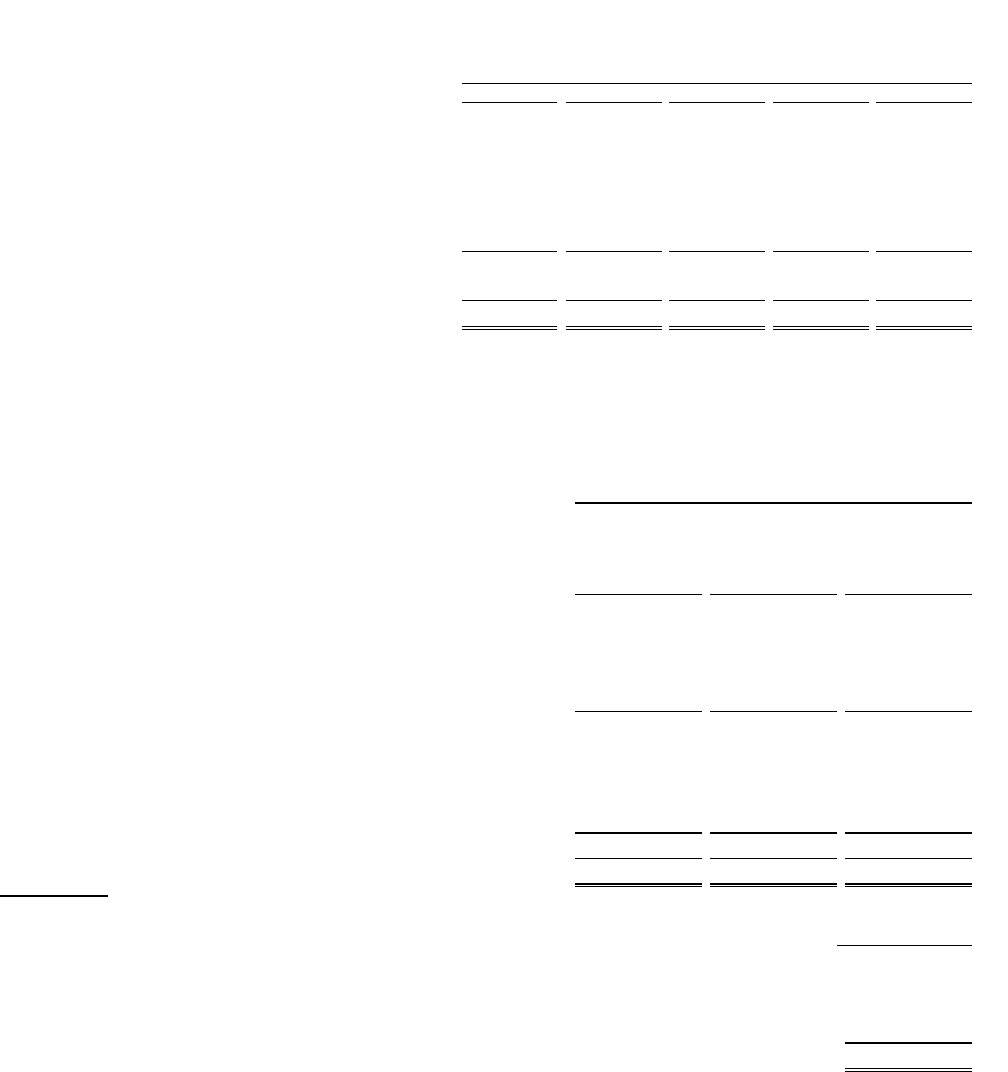

this context, BB&T strives to meet the credit needs of businesses and consumers in its markets while pursuing a balanced

strategy of loan profitability, loan growth and loan quality.

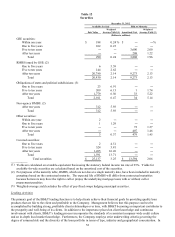

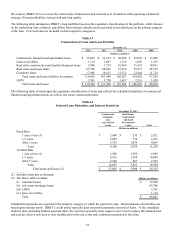

The following table summarizes BB&T’ s loan portfolio based on the regulatory classification of the portfolio, which focuses

on the underlying loan collateral, and differs from internal classifications presented herein that focus on the primary purpose

of the loan. Covered loans are included in their respective categories.

Table 13

Composition of Loan and Lease Portfolio

December 31,

2012 2011 2010 2009 2008

(Dollars in millions)

Commercial, financial and agricultural loans $ 23,863 $ 21,452 $ 20,490 $ 19,076 $ 17,489

Lease receivables 1,114 1,067 1,158 1,092 1,315

Real estate-construction and land development loans 5,900 7,714 10,969 15,353 18,012

Real estate-mortgage loans 65,760 60,821 57,418 55,671 48,719

Consumer loans 17,966 16,415 13,532 12,464 11,710

Total loans and leases held for investment 114,603 107,469 103,567 103,656 97,245

LHFS 3,761 3,736 3,697 2,551 1,424

Total loans and leases $ 118,364 $ 111,205 $ 107,264 $ 106,207 $ 98,669

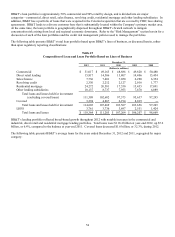

The following table is based upon the regulatory classification of loans and reflects the scheduled maturities of commercial,

financial and agricultural loans, as well as real estate construction loans:

Table 14

Selected Loan Maturities and Interest Sensitivity

December 31, 2012

Commercial, Real Estate:

Financial Construction

and and Land

Agricultural Development

Loans Loans Total

(Dollars in millions)

Fixed Rate:

1 year or less (1) $ 2,688 $ 233 $ 2,921

1-5 years 2,699 772 3,471

After 5 years 3,793 1,074 4,867

Total 9,180 2,079 11,259

Variable Rate:

1 year or less (1) 3,508 1,395 4,903

1-5 years 8,935 1,959 10,894

After 5 years 2,240 467 2,707

Total 14,683 3,821 18,504

Total loans and leases (2) $ 23,863 $ 5,900 $ 29,763

(1) Includes loans due on demand.

(2) The above table excludes: (Dollars in millions)

(i) consumer loans $ 17,966

(ii) real estate mortgage loans 65,760

(iii) LHFS 3,761

(iv) lease receivables 1,114

Total $ 88,601

Scheduled repayments are reported in the maturity category in which the payment is due. Determinations of maturities are

based upon contract terms. BB&T’ s credit policy typically does not permit automatic renewal of loans. At the scheduled

maturity date (including balloon payment date), the customer generally must request a new loan to replace the matured loan

and execute either a new note or note modification with rate, terms and conditions negotiated at that time.