BB&T 2012 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

72

As of December 31, 2012 and 2011, the Parent Company had 35 months and 23 months, respectively, of cash on hand to

satisfy projected contractual cash outflows as described above.

Branch Bank

Branch Bank has several major sources of funding to meet its liquidity requirements, including access to capital markets

through issuance of senior or subordinated bank notes and institutional CDs, access to the FHLB system, dealer repurchase

agreements and repurchase agreements with commercial clients, access to the overnight and term Federal funds markets, use

of a Cayman branch facility, access to retail brokered CDs and a borrower in custody program with the FRB for the discount

window. As of December 31, 2012, BB&T has approximately $53 billion of secured borrowing capacity, which represents

approximately 290% of one year wholesale funding maturities.

BB&T also monitors the ability to meet customer demand for funds under both normal and stressed market conditions. In

considering its liquidity position, management evaluates BB&T’ s funding mix based on client core funding, client rate-

sensitive funding and non-client rate-sensitive funding. In addition, management also evaluates exposure to rate-sensitive

funding sources that mature in one year or less. Management also measures liquidity needs against 30 days of stressed cash

outflows for Branch Bank. To ensure a strong liquidity position, management maintains a liquid asset buffer of cash on hand

and highly liquid unpledged securities. The Company has established a policy that the liquid asset buffer would be a

minimum of 5% of total assets, but intends to maintain the ratio well in excess of this level. As of December 31, 2012, and

December 31, 2011, BB&T’ s liquid asset buffer was 11.1% and 13.5%, respectively, of total assets.

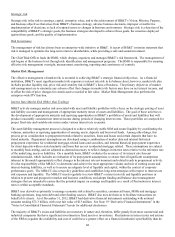

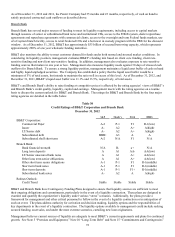

BB&T’ s and Branch Bank’ s ability to raise funding at competitive prices is affected by the rating agencies’ views of BB&T’ s

and Branch Bank’ s credit quality, liquidity, capital and earnings. Management meets with the rating agencies on a routine

basis to discuss the current outlook for BB&T and Branch Bank. The ratings for BB&T and Branch Bank by the four major

rating agencies are detailed in the table below.

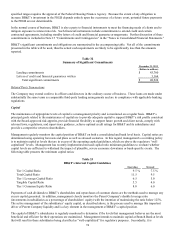

Table 30

Credit Ratings of BB&T Corporation and Branch Bank

December 31, 2012

S&P Moody's Fitch DBRS

BB&T Corporation:

Commercial Paper A-2 P-1 F1 R-1(low)

Issuer A- A2 A+ A(high)

LT/Senior debt A- A2 A+ A(high)

Subordinated debt BBB+ A3 A A

Subordinated shelf short term A-2 N/A F1 N/A

Branch Bank:

Bank financial strength N/A B- a+ N/A

Long term deposits A A1 AA- AA(low)

LT/Senior unsecured bank notes A A1 A+ AA(low)

Other long term senior obligations A A1 A+ AA(low)

Other short term senior obligations A-1 P-1 F1 R-1(middle)

Short term bank notes A-1 P-1 F1 R-1(middle)

Short term deposits A-1 P-1 F1+ R-1(middle)

Subordinated bank notes A- A2 A A(high)

Ratings Outlook:

Credit Trend Stable Stable Stable Stable

BB&T and Branch Bank have Contingency Funding Plans designed to ensure that liquidity sources are sufficient to meet

their ongoing obligations and commitments, particularly in the event of a liquidity contraction. These plans are designed to

examine and quantify the organization’ s liquidity under various “stress” scenarios. Additionally, the plans provide a

framework for management and other critical personnel to follow in the event of a liquidity contraction or in anticipation of

such an event. The plans address authority for activation and decision making, liquidity options and the responsibilities of

key departments in the event of a liquidity contraction. The liquidity options available to management could include seeking

secured funding, asset sales, and under the most extreme scenarios, curtailing new loan originations.

Management believes current sources of liquidity are adequate to meet BB&T’ s current requirements and plans for continued

growth. See Note 5 “Premises and Equipment,” Note 10 “Long-Term Debt” and Note 15 “Commitments and Contingencies”