BB&T 2012 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

2012 Annual Report

5

2012 RESULTS

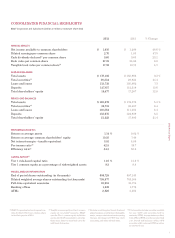

BB&T had an outstanding year in 2012. We achieved record net

income available to common shareholders and strong growth in

noninterest income, led by record performances in mortgage

banking, insurance and investment banking and brokerage.

We continued to produce broad-based improvement in credit

quality. We sustained balanced and broad-based loan growth

despite a still-slow economy and improved the growth, mix

and cost of our deposits. Our net interest margin remained

strong, and we held noninterest expenses essentially flat while

successfully completing our BankAtlantic and Crump Group

acquisitions. With increasing and diverse sources of revenue,

we believe BB&T is positioned for another high-performance

year in 2013.

Net income available to common shareholders for 2012

increased by 49% from 2011 to $1.9 billion. Earnings per

diluted common share totaled $2.70, compared with $1.83

earned in 2011, an increase of 48%. Total revenues increased

12.0% to $9.8 billion in 2012 compared with 2011.

Average loans and leases increased by 7.3% in 2012 over

2011, exceeding the 6.1% average growth of our peer group.

Commercial and industrial, direct retail and residential

mortgage loans led BB&T’s broad-based growth. We are

encouraged by increasing loan production from our Community

Bank, up 26% over last year, with strong gains in our newer

Florida, Texas and Alabama markets added through the

Colonial acquisition. Although many of those commitments

are not funded yet, we believe production is a good indicator of

future growth if there is a pickup in momentum in the economy.

Our average deposit growth of 13.6% outpaced all of our

peers, which had an average growth rate of 6.9%. We were

particularly pleased that BB&T’s average noninterest-bearing

deposits grew by 26.1% for the year, showing the success of our

strategy to change our deposit mix with lower deposit costs.

We anticipate more modest deposit growth in the first quarter

of 2013 with continued improvement in deposit costs.

BB&T’s credit-quality measures also continued to improve.

Total nonperforming assets as a percentage of average assets

decreased each quarter in 2012 to 0.85% at year end excluding

covered assets, the lowest level since the second quarter of 2008

and superior to the 1.08% average of BB&T’s peers. We expect

continued improvement at a modest pace in the first quarter

of 2013, assuming no significant deterioration in the economy.

Net charge-offs, excluding covered loans, also improved each

quarter of 2012 to 1.04% in the fourth quarter, a four-year

low. In the first quarter of 2013, we anticipate net charge-offs

to approximate 1.00% of average loans, and trend lower during

the year. In addition, our foreclosed real estate balance has

fallen to a five-year low.

BB&T’s fully taxable equivalent net interest income totaled

$6.0 billion in 2012, a 6.2% increase from 2011. Our net

interest margin remained strong at 3.91% for 2012, comparing

favorably with the 3.45% average of our peers. We do expect

the margin to decline somewhat in 2013. Improvement

in BB&T’s deposit mix is being offset by continued pressure on

our asset yields from the very low interest-rate environment

and anticipated runoff of covered assets acquired as part of

the Colonial transaction. The net interest margin, key to a

bank’s profitability, is the difference between the interest

received on loans and investments and the interest paid

on deposits and other funding, expressed as a percentage

of average earning assets.

Our noninterest income totaled $3.8 billion, a 22.7% increase

over 2011. Insurance income benefited from a somewhat

stronger pricing market and the acquisition of Crump Group.

Mortgage banking income increased with higher gains

on residential mortgage production and sales. Investment

banking and brokerage fees and commissions grew because

of improved financial market conditions. BB&T’s fee income

ratio improved to 42.5% for the year, up from 39.7% for 2011

and compared favorably with our peer average of 38.0%.

The ratio reflects our continued success in diversifying our

sources of revenue.

Excludes foreclosed property expense, provision for loan and lease losses, and securities gains (losses).

Pre-Tax Pre-Credit Earnings

Consistent Long-Term Earnings Power

As originally reported 15-year compound annual growth rate 13.3%