BB&T 2012 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

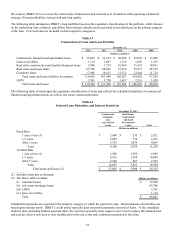

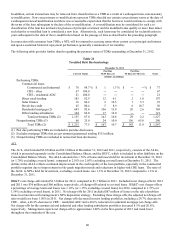

63

stability and relative cost. Deposits are regarded as an important part of the overall client relationship and provide

opportunities to cross-sell other BB&T services.

Total deposits at December 31, 2012, were $133.1 billion, an increase of $8.1 billion, or 6.5%, compared to year-end 2011.

Noninterest-bearing deposits totaled $32.5 billion at December 31, 2012, an increase of $6.8 billion, or 26.4%, from

December 31, 2011. The increase in noninterest-bearing deposits was broad based in nature, with increases in deposits from

personal, business and public funds clients. Interest checking and money market and savings accounts increased $3.7 billion,

or 5.6% compared to the prior year, while certificates and other time deposits declined $2.3 billion, or 6.7%, during that same

time period. For the year ended December 31, 2012, total deposits averaged $127.6 billion, an increase of $15.3 billion, or

13.6%, compared to 2011. Management currently expects more modest deposit growth in the first quarter of 2013.

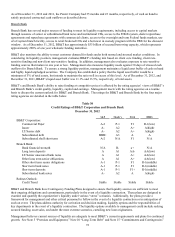

The following table presents BB&T’ s average deposits for the years ended December 31, 2012 and 2011, segregated by

major category:

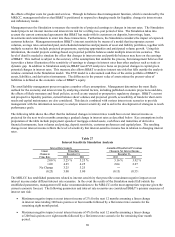

Table 24

Composition of Average Deposits

Years Ended December 31,

2012 2011

Balance % of total Balance % of total

(Dollars in millions)

N

oninteres

t

-bearing deposits $ 28,925 22.7 % $ 22,945 20.4 %

Interest checking 19,904 15.6 18,614 16.6

Money market and savings 46,927 36.7 41,287 36.7

Certificates and other time deposits 31,647 24.8 28,825 25.7

Foreign office deposits - interest-bearing 214 0.2 647 0.6

Total average deposits $ 127,617 100.0 % $ 112,318 100.0 %

The overall mix of deposits improved during 2012, with average noninterest-bearing deposits representing 22.7% of average

total deposits during 2012, compared to 20.4% during 2011. Deposit mix was also positively impacted by certificates and

other time deposits, which represented 24.8% of average total deposits during 2012, down from 25.7% of average total

deposits during 2011. The average cost of interest-bearing deposits was 0.43% for 2012, compared to 0.68% in the prior

year. Management expects that deposit costs will continue to trend downward in 2013.

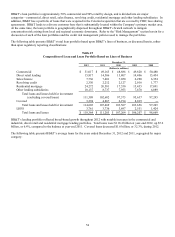

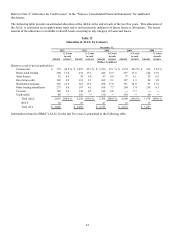

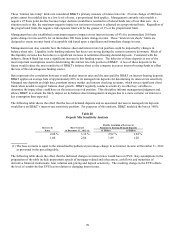

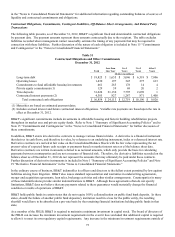

The following table provides information regarding the scheduled maturities of time deposits that are $100,000 and greater at

December 31, 2012:

Table 25

Scheduled Maturities of Time Deposits $100,000 and Greater

December 31, 2012

(Dollars in millions)

Three months or less $ 7,675

Over three through six months 4,163

Over six through twelve months 3,054

Over twelve months 4,436

Total $ 19,328

Short-term Borrowings

BB&T also uses various types of short-term borrowings in meeting funding needs. While deposits remain the primary source

for funding loan originations, management uses short-term borrowings as a supplementary funding source for loan growth

and other balance sheet management purposes. Short-term borrowings were 1.9% of total funding on average in 2012 as

compared to 3.2% in 2011. See Note 8 “Federal Funds Purchased, Securities Sold Under Agreements to Repurchase and

Short-Term Borrowed Funds” in the “Notes to Consolidated Financial Statements” herein for further disclosure. The types of

short-term borrowings that have been, or may be, used by the Company include Federal funds purchased, securities sold

under repurchase agreements, master notes, commercial paper, U.S. Treasury tax and loan deposit notes and short-term bank

notes. All of BB&T’ s securities sold under repurchase agreements are reflected as collateralized borrowings on the balance

sheet. Short-term borrowings at the end of 2012 were $2.9 billion, a decrease of $702 million, or 19.7%, compared to year-