BB&T 2012 Annual Report Download - page 157

Download and view the complete annual report

Please find page 157 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

135

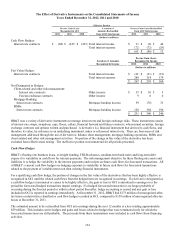

Fair Value Hedges

BB&T’ s fixed rate long-term debt, CDs, FHLB advances, loans and state and political subdivision securities produce

exposure to losses in value as interest rates change. The risk management objective for hedging fixed rate assets and

liabilities is to convert the fixed rate paid or received to a floating rate. BB&T accomplishes its risk management objective

by hedging exposure to changes in fair value of fixed rate financial instruments primarily through the use of swaps. For a

qualifying fair value hedge, changes in the value of the derivatives that have been highly effective as hedges are recognized

in current period earnings along with the corresponding changes in the fair value of the designated hedged item attributable to

the risk being hedged.

During the years ended December 31, 2012 and 2011, BB&T terminated certain fair value hedges related to its long-term

debt and municipal securities and received net proceeds of $85 million and $185 million, respectively. When a hedge has

been terminated but the hedged item remains outstanding, the proceeds from the termination of these hedges have been

reflected as part of the carrying value of the underlying debt/other financial instrument and are being amortized to earnings

over its estimated remaining life. The proceeds from these terminations were included in cash flows from financing

activities. During the years ended December 31, 2012 and 2011, BB&T recognized pre-tax benefits of $256 million and

$205 million, respectively, through reductions of interest expense from previously unwound fair value debt hedges.

Derivatives Not Designated As Hedges

Derivatives not designated as hedges are those that are entered into as either balance sheet risk management instruments or to

facilitate client needs. Balance sheet risk management hedges are those hedges that do not qualify to be treated as a cash

flow hedge, a fair value hedge or a foreign currency hedge for accounting purposes, but are necessary to economically

manage the risk associated with an asset or liability.

This category of hedges includes derivatives that hedge mortgage banking operations and MSRs. For mortgage loans

originated for sale, BB&T is exposed to changes in market rates and conditions subsequent to the interest rate lock and

funding date. BB&T’ s risk management strategy related to its interest rate lock commitment derivatives and LHFS includes

using mortgage-based derivatives such as forward commitments and options in order to mitigate market risk. For MSRs,

BB&T uses various derivative instruments to mitigate the income statement effect of changes in the fair value of its MSRs.

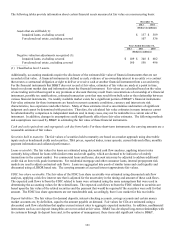

For the year ended December 31, 2012, BB&T recorded a gain of $128 million related to these derivatives, which was offset

by a negative $32 million valuation adjustment related to the MSR. For the year ended December 31, 2011, BB&T recorded

a gain of $394 million related to these derivatives, which was offset by a negative $341 million valuation adjustment related

to the MSR.

BB&T also held, as risk management instruments, other derivatives not designated as hedges primarily to facilitate

transactions on behalf of its clients, as well as activities related to balance sheet management.

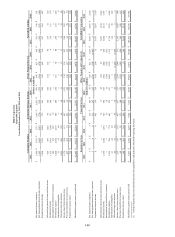

Derivatives Credit Risk – Dealer Counterparties

Credit risk related to derivatives arises when amounts receivable from a counterparty exceed those payable to the same

counterparty. BB&T addresses the risk of loss by subjecting dealer counterparties to credit reviews and approvals similar to

those used in making loans or other extensions of credit and by requiring collateral. Dealer counterparties operate under

agreements to provide cash and/or liquid collateral when unsecured loss positions exceed negotiated limits.

As of December 31, 2012, BB&T had received cash collateral from dealer counterparties totaling $44 million related to

derivatives in a gain position of $40 million and had posted $639 million in cash collateral to dealer counterparties to secure

derivatives in a loss position of $650 million. In the event that BB&T’ s credit ratings had been downgraded below

investment grade, the amount of collateral posted to these counterparties would have increased by $12 million. As of

December 31, 2011, BB&T had received cash collateral from dealer counterparties totaling $82 million related to derivatives

in a gain position of $79 million and had posted $639 million in cash collateral to dealer counterparties to secure derivatives

in a loss position of $669 million. In the event that BB&T’ s credit ratings had been downgraded below investment grade, the

amount of collateral posted to these counterparties would have increased by $30 million.

After collateral postings are considered, BB&T had no unsecured positions in a gain with dealer counterparties at December

31, 2012, compared to $3 million at December 31, 2011. All of BB&T’ s derivative contracts with dealer counterparties settle

on a monthly, quarterly or semiannual basis, with daily movement of collateral between counterparties required within

established netting agreements. BB&T only transacts with dealer counterparties that are national market makers with strong

credit ratings.