BB&T 2012 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

2012 Annual Report

7

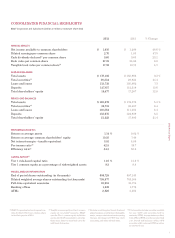

We held noninterest expenses basically flat at $5.8 billion

in 2012. Increases in production-related incentives and

commissions were offset in part by decreases in foreclosed

property expenses, which were at the lowest level since the third

quarter of 2007. For the first quarter of 2013, we expect lower

noninterest expenses, driven by decreases in production-related

incentives and professional services, with essentially flat

discretionary spending and full-time equivalent employment.

BB&T’s return on average assets improved to 1.14% in 2012

from 0.82% in 2011, while return on average common

shareholders’ equity increased to 10.4% from 7.5%. Both

measures are superior to our peer average. We also continue to

outperform our peers in pre-tax, pre-credit earnings, which we

believe is an important measure of a bank’s consistent long-term

earnings power. Over the last 15 years, the compound annual

growth rate of BB&T’s pre-tax, pre-credit earnings is 13.3%.

Overall, we believe our 2012 results reflect the excellent progress

BB&T has made with our diversification strategy over the last

several years as we work to return to normalized profitability.

OUR STOCK PERFORMANCE

Our ultimate responsibility is to optimize the long-term

return to our shareholders, while providing a safe and sound

investment. We meet that responsibility by managing BB&T

for the long-term, rather than chasing the latest investment

vehicle to boost short-term earnings. Consider, for example,

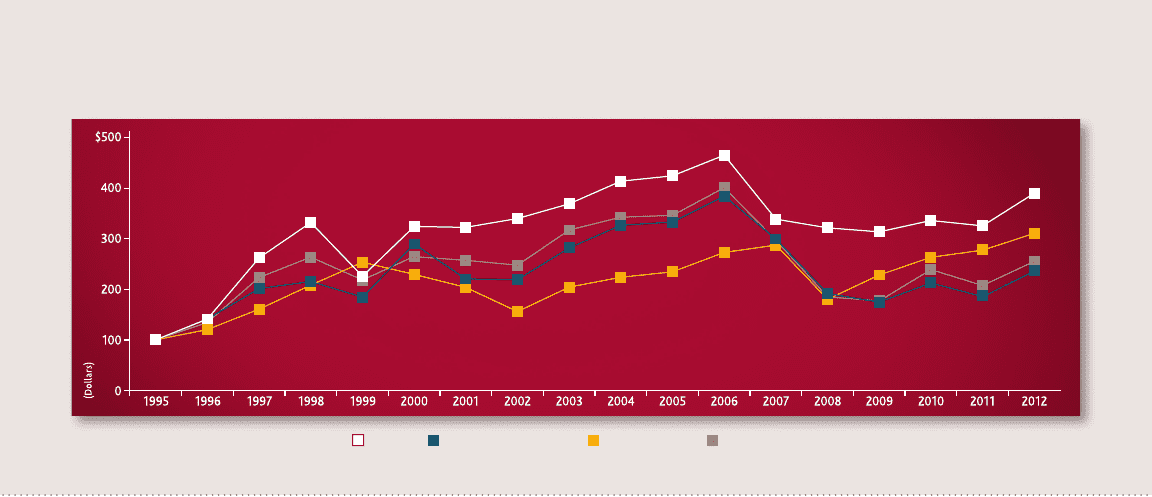

our 20-year annualized total return to shareholders, which

includes net stock price change plus dividends paid. BB&T’s

return was 9.2%, compared with the 5.4% average of our peers.

A $100 investment in BB&T shares in 1995 was worth $392

on December 31, 2012, significantly better than the S&P 500

as well as our in-market peers.

In 2012, BB&T’s total return to shareholders was 18.4%.

In part, our shares benefited from the appreciation of most

bank stocks as investors began to assign more reasonable

valuations following the financial-market crisis of the last five

years. But unlike some of our peers that realized outsized gains

mainly because their shares were recovering from very poor

performances in prior years, we believe investors recognize

the value of BB&T’s well-defined and consistent strategies and

our proven ability to execute them.

Our long-term and consistent approach also is reflected in our

dividend strategy. BB&T has paid a cash dividend every year

since 1903. We became the first of the largest banks to announce

an increase in our dividend in 2011, and our current dividend yield

of approximately 3.00% is among the strongest in the banking

industry. We have a special obligation to our shareholders

because, unlike many big banks with large majorities of

institutional investors, nearly half of BB&T’s shareholders are

individuals who depend on our returns and dividends.

We are committed to a robust dividend payout going forward.

In the fourth quarter of 2012, we earned $0.71 per diluted

common share and paid out $0.20 per share, or a 28% payout. In

January 2013, when BB&T declared our first quarter dividend,

we increased the amount to $0.23 a share, which is consistent

with the 2012 capital plan that BB&T submitted to the Federal

Reserve last year. My pledge to shareholders is to continue

to manage BB&T for the long term so we are able to consistently

increase our earnings and, in turn, reward our shareholders

with a safe and sound investment that pays superior long-term

returns and dividends.

OUR CAPITAL STRENGTH

BB&T continues to be one of the strongest capitalized

institutions in the banking industry. Our capital strength gives

BB&T the financial strength to take advantage of opportunities

that are in the best interest of our shareholders, including

continuing our proactive dividend strategy.

Our capital levels – the margin by which creditors are covered

if a bank’s assets are liquidated – well exceed regulatory

requirements. Those levels include the impact of our Crump

Group and BankAtlantic acquisitions and the early redemption

of trust preferred securities in 2012. Moreover, even though

Shareholder Return

BB&T S&P Commercial Banks S&P 500 Index Peer Average

Depicts $100 invested at 12/31/95 and held through 12/31/12 with dividends reinvested in the security or index.