BB&T 2012 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

101

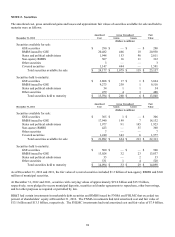

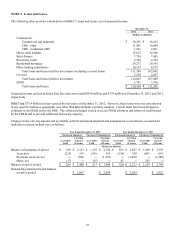

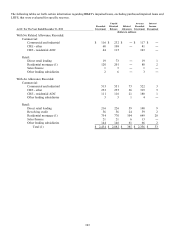

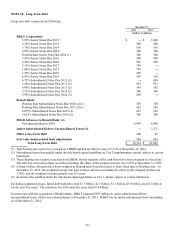

BB&T monitors the credit quality of its retail portfolio segment based primarily on delinquency status, which is the primary

factor considered in determining whether a retail loan should be classified as nonaccrual.

The following tables illustrate the credit quality indicators associated with loans and leases held for investment. Covered

loans are excluded from this analysis because their related allowance is determined by loan pool performance.

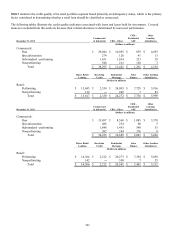

CRE - Other

Commercial Residential Lending

December 31, 2012 & Industrial CRE - Other ADC Subsidiaries

(Dollars in millions)

Commercial:

Pass $ 36,044 $ 10,095 $ 859 $ 4,093

Special mention 274 120 41 13

Substandard - performing 1,431 1,034 233 29

N

onperforming 546 212 128 3

Total $ 38,295 $ 11,461 $ 1,261 $ 4,138

Direct Retail Revolving Residential Sales Other Lending

Lending Credit Mortgage Finance Subsidiaries

(Dollars in millions)

Retail:

Performing $ 15,685 $ 2,330 $ 24,003 $ 7,729 $ 5,916

N

onperforming 132 ― 269 7 83

Total $ 15,817 $ 2,330 $ 24,272 $ 7,736 $ 5,999

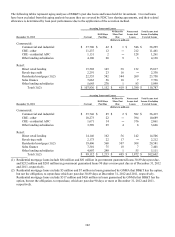

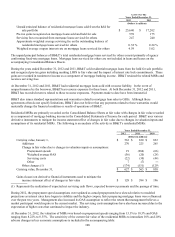

CRE - Other

Commercial Residential Lending

December 31, 2011 & Industrial CRE - Other ADC Subsidiaries

(Dollars in millions)

Commercial:

Pass $ 33,497 $ 8,568 $ 1,085 $ 3,578

Special mention 488 234 60 5

Substandard - performing 1,848 1,493 540 35

N

onperforming 582 394 376 8

Total $ 36,415 $ 10,689 $ 2,061 $ 3,626

Direct Retail Revolving Residential Sales Other Lending

Lending Credit Mortgage Finance Subsidiaries

(Dollars in millions)

Retail:

Performing $ 14,364 $ 2,212 $ 20,273 $ 7,394 $ 5,056

N

onperforming 142 ― 308 7 55

Total $ 14,506 $ 2,212 $ 20,581 $ 7,401 $ 5,111