BB&T 2012 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2012 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

25

Difficulty in integrating an acquired company may cause BB&T not to realize expected revenue increases, cost savings,

increases in geographic or product presence and/or other projected benefits from the acquisition. The integration could result

in higher than expected deposit attrition, loss of key employees, disruption of BB&T’ s businesses or the businesses of the

acquired company, or otherwise adversely affect BB&T’ s ability to maintain relationships with customers and employees or

achieve the anticipated benefits of the acquisition. Also, the negative effect of any divestitures required by regulatory

authorities in acquisitions or business combinations may be greater than expected.

Rulemaking changes implemented by the CFPB will result in higher regulatory and compliance costs related to originating

and servicing mortgages and may adversely affect our results of operations.

The CFPB recently has finalized a number of significant rules which will impact nearly every aspect of the lifecycle of a

residential mortgage. These rules implement the Dodd-Frank Act amendments to the Equal Credit Opportunity Act, the

Truth in Lending Act and the Real Estate Settlement Procedures Act. The final rules require banks to, among other things: (i)

develop and implement procedures to ensure compliance with a new "reasonable ability to repay" test and identify whether a

loan meets a new definition for a "qualified mortgage;" (ii) implement new or revised disclosures, policies and procedures for

servicing mortgages including, but not limited to, early intervention with delinquent borrowers and specific loss mitigation

procedures for loans secured by a borrower's principal residence; (iii) comply with additional restrictions on mortgage loan

originator compensation; and (iv) comply with new disclosure requirements and standards for appraisals and escrow accounts

maintained for "higher priced mortgage loans." These new rules create operational and strategic challenges for BB&T, as it

is both a mortgage originator and a servicer. For example, business models for cost, pricing, delivery, compensation, and risk

management will need to be reevaluated and potentially revised, perhaps substantially. Additionally, programming changes

and enhancements to systems will be necessary to comply with the new rules. Some of these new rules will be effective in

June 2013, while others will be effective in January 2014. Forthcoming additional rulemaking affecting the residential

mortgage business is also expected. Achieving full compliance in the relatively short timeframe provided for certain of the

new rules will result in increased regulatory and compliance costs.

The Colonial loan portfolios are largely covered by shared-loss agreements, however, BB&T is not immune from losses or

risks relative to these portfolios.

Branch Bank acquired significant loan portfolios in connection with its acquisition of Colonial and entered into loss sharing

agreements with the FDIC, which provide that a significant portion of losses related to the covered loan portfolios will be

borne by the FDIC. Fluctuations in economic conditions, including those related to local residential real estate, commercial

real estate and construction markets, may increase the level of charge-offs on the acquired loan portfolio and correspondingly

reduce BB&T’ s net income. These fluctuations are not predictable, cannot be controlled and may have a material adverse

impact on BB&T’ s operations and financial condition even if other favorable events occur. Additionally, the loss sharing

agreements have limited terms; therefore, any charge-off of related losses that Branch Bank experiences after the term of the

loss sharing agreements will not be reimbursed by the FDIC and will negatively impact BB&T’ s net income.

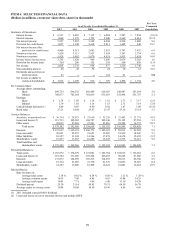

ITEM 2. PROPERTIES

BB&T owns or leases significant office space used as the Company’ s headquarters in Winston-Salem, North Carolina.

BB&T owns free-standing operations centers, with its primary operations and information technology center located in

Wilson, North Carolina. BB&T occupies offices that are either owned or operated under long-term leases. At December 31,

2012, Branch Bank operated 1,832 branch offices in North Carolina, Virginia, Florida, Georgia, Maryland, South Carolina,

Alabama, West Virginia, Kentucky, Tennessee, Texas, Washington D.C and Indiana. BB&T also operates numerous

insurance agencies and other businesses that occupy facilities. Office locations are either owned or leased. Management

believes that the premises occupied by BB&T and its subsidiaries are well-located and suitably equipped to serve as financial

services facilities. See Note 5 “Premises and Equipment” in the “Notes to Consolidated Financial Statements” in this report

for additional disclosures related to BB&T’ s properties and other fixed assets.

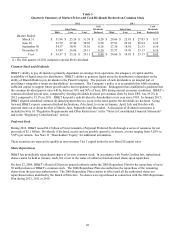

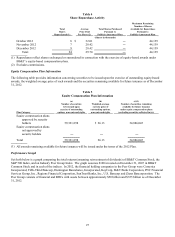

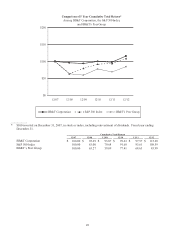

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND

ISSUER PURCHASES OF EQUITY SECURITIES

BB&T’ s common stock is traded on the NYSE under the symbol “BBT.” BB&T’ s common stock was held by

approximately 315,000 shareholders at December 31, 2012 compared to approximately 293,000 shareholders at December

31, 2011. The following table sets forth the quarterly high and low trading prices and closing sales prices for BB&T’ s

common stock and the dividends declared per share of common stock for each of the last eight quarters.