RBS 2005 Annual Report Download

Download and view the complete annual report

Please find the complete 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Make it happen

rbs.com

Annual Report and Accounts 2005

Profit before

tax up

21%

Total

income up

14%

Adjusted

earnings per

share up

8%

Dividend up

25%

Table of contents

-

Page 1

Annual Report and Accounts 2005 Profit before tax up 21% Total income up 14% Adjusted earnings per share up 8% Dividend up 25% rbs.com Make it happen -

Page 2

... acquisition of Churchill broadened the product and distribution channel capabilities of Direct Line and created the second largest general insurer in the UK. In corporate banking, RBS has entered the US, Continental European and Asia Pacific markets. In August 2005, RBS signed strategic investment... -

Page 3

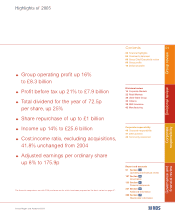

... before tax up 21% to £7.9 billion Total dividend for the year of 72.5p per share, up 25% Share repurchase of up to £1 billion Divisional review 14 Corporate Markets 22 Retail Markets 30 Ulster Bank Group 32 Citizens 38 RBS Insurance 42 Manufacturing Cost:income ratio, excluding acquisitions, 41... -

Page 4

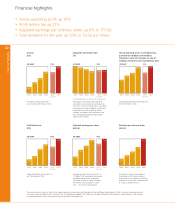

...per ordinary share up 8% to 175.9p Total dividend for the year up 25% to 72.5p per share 02 Financial highlights Income (£m) Adjusted cost:income ratio (%) Group operating profit - profit before tax, purchased intangibles amortisation, integration costs and net gain on sale of strategic investments... -

Page 5

... 28 13 1 UK US Europe Rest of World 75 19 5 1 The Group's market capitalisation at 31 December 2005 was £56.1 billion compared with £55.6 billion a year earlier. Europe Rest of World Geographic analysis of income determined by location of customer 2005 Group review Total shareholder return... -

Page 6

... markets, both will greatly strengthen the Board as we embark on our next phase of growth. On 1 February 2006 Guy Whittaker joined the Board as Group Finance Director. He is an experienced senior executive of the highest calibre, with great breadth of international experience in financial services... -

Page 7

2005 Group review 05 -

Page 8

Group Chief Executive's review 06 Group Chief Executive's review -

Page 9

... areas, including risk and financial management, human resources and information technology. Our customers Customer numbers increased in all our divisions, with The Royal Bank of Scotland securing top position amongst the high street banks for personal customer satisfaction and NatWest moving into... -

Page 10

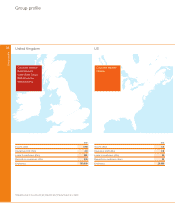

Group profile 08 Group profile United Kingdom US Corporate Markets Retail Markets Ulster Bank Group RBS Insurance Manufacturing Corporate Markets Citizens 2005 2005 Income (£bn) Operating profit (£bn) Loans to customers (£bn) Deposits by customers (£bn) Employees 18.8 4.8 281 235 103,... -

Page 11

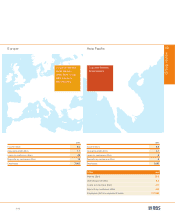

... 09 Corporate Markets Retail Markets Ulster Bank Group RBS Insurance Manufacturing Corporate Markets Retail Markets 2005 2005 Income (£bn) Operating profit (£bn) Loans to customers (£bn) Deposits by customers (£bn) Employees 2.0 1.1 42 18 7,000 Income (£bn) Operating profit (£bn) Loans... -

Page 12

... world. UK Corporate Banking Geographical spread UK Market data No.1 UK corporate and commercial relationship bank No.1 for UK payments No.1 for card transaction processing No.1 for deposits No.1 for lending No.1 for asset finance No.1 for invoice finance No.1 for foreign exchange No.1 for sterling... -

Page 13

... offshore customers. Retail Markets brands include The Royal Bank of Scotland and NatWest in retail banking and credit cards. MINT and Tesco Personal Finance also offer cards, and a range of products and services are available through The One account, First Active UK, Direct Line Financial Services... -

Page 14

... corporates via branches, telephone and the internet. Ulster Bank Group has the largest share of personal banking customers in Northern Ireland and is the third largest bank in the Republic of Ireland. In 2005 Ulster Bank Group launched market-leading mortgage and current account products and a new... -

Page 15

..., account management, lending, mortgage processing and money transmission. Group Technology develops and maintains the infrastructure and technology that supports the branches, ATMs and internet banking for customers of Corporate Markets, Retail Markets and RBS Insurance. Purchasing is responsible... -

Page 16

...Markets Kew Gardens has an international reputation. In 2005 they selected RBS for the quality of online banking data we offered alongside a very competitive and flexible interest bearing account. RBS is UK market leader in the provision of banking services to the charitable sector. Make it happen -

Page 17

...and RBS Invoice Finance have 400 sales staff working out of 53 offices, and over 100,000 customers. Make it happen The former Corporate Banking & Financial Markets division was renamed Corporate Markets on 1 January 2006, when we reorganised our activities into two businesses, UK Corporate Banking... -

Page 18

... enabled the company to trade safely in these countries. Global Banking & Markets is a leading banking partner to major corporates and financial institutions around the world, specialising in providing these customers with a full range of debt financing, risk management and investment services. We... -

Page 19

... consolidated its loan facilities with RBS as sole lender. Bloomsbury Publishing is one of Britain's most successful publishing houses. It is best known for titles such as Harry Potter and the Pru Leith Cookery books and is a long-standing UK Corporate Banking customer. 2005 Divisional review -

Page 20

... Banking &Corporate Financial Markets Pernod Ricard. In April 2005 Pernod Ricard completed the acquisition of Allied Domecq. RBS was one of four Bookrunners for the â,¬9.2 billion facility offering specialist expertise in â,¬/£ foreign exchange hedging and structured loans. Make it happen -

Page 21

...both of the UK's leading cable companies, deep sector knowledge and tactical use of our balance sheet we helped to pave the way for the merger between NTL and Telewest, thereby consolidating our position as a top-tier partner bank to this customer. 2005 Divisional review A controlled expansion of... -

Page 22

... Leveraged Finance Financial News Mezzanine Debt provider of the year European Venture Capital (& Private Equity) Journal EMEA Bank of the Year - Project Finance PFI awards Best Bank in Foreign Exchange in London FX Week Best Bank in Asian Prime Brokerage AsiaMoney FX Survey Make it happen -

Page 23

...billion private placement for Adidas, a global leader in the sporting goods industry. It was the largest such placement in the US out of Germany. The funding will largely be used to finance their acquisition of Reebok in the US. Monro Muffler. RBS Securities and Charter One in Chicago joined forces... -

Page 24

...banks to offer a Child Trust Fund in response to the Government's commitment to give £250 to each child born after September 2002. RBS has matched the £250 with discounted retail vouchers and created a new stakeholder product to capitalise on the value the child will receive at 18. Make it happen -

Page 25

..., 12 months to November 2005; high street banks defined as RBS, NatWest, Barclays, Lloyds TSB, HSBC and HBOS. Passion Divisional review We added nearly 800 people to our Royal Bank of Scotland and NatWest branch networks and telephony service, improved personal access for customers by opening new... -

Page 26

... Scotland launched First Home Saver, a new savings account designed to help customers get onto the property ladder by encouraging them to save regularly for the deposit, and by giving a tax-free bonus on taking out a Royal Bank of Scotland mortgage. In September 2005, Royal Bank of Scotland Business... -

Page 27

... Managers. In 2005 NatWest re-introduced local business managers covering 180 key branches. In Fareham Chris Jack meets Nick Bowes of Airport Bodyshop on his premises. NatWest Mobile Bank. Last year NatWest launched a new mobile bank in Cornwall bringing banking services to 13 local communities... -

Page 28

... Direct offers a full range of financial services products through a number of brands and a variety of convenient channels in the UK and continental Europe. 26 Retail Markets Tesco Personal Finance in Hungary. Our joint venture with Tesco is developing its presence in Europe. Financial services... -

Page 29

...the year the number of customer accounts at Tesco Personal Finance exceeded five million. First Active supported the launch of two new TPF mortgage products, making TPF the only supermarket bank to offer mortgages. Retail Direct also continued to support the development of Tesco's financial services... -

Page 30

... The Royal Bank of Scotland - Best for Overall Customer Service category 2005 Personal Finance and Savings Readership Awards First Active - Best Remortgage Lender Mortgage Magazine Awards and Mortgage Advisor & Homebuyer Awards NatWest Kirkham Branch - Customer Service Team of the Year Financial... -

Page 31

..., value for money is important. Last May after consolidating her mortgage and a home improvement loan into a fixed rate mortgage with First Active, she saved over £100 a month. The One account. "One Day" as the advertisements say...I'll have my own music studio. Mark Young transferred his mortgage... -

Page 32

...- £460 million) Total income increased 15% Profit up 15% 30 Ulster Bank Group University of Limerick. Ulster Bank and University of Limerick share a passion for innovation and high standards. A 10-year agreement has underlined Ulster Bank's commitment to the education sector nationally and to the... -

Page 33

... Ireland to provide free banking to all personal customers. First Active introduced the Republic of Ireland's first 100% First Time Buyers' Mortgage confirming First Active's reputation for innovative products. These include the Current Account Mortgage and Elevator savings account. Ulster Bank... -

Page 34

...years. It builds ferries, tugs and barges, one of which is seen here on the famous Staten Island crossing. To help fund further investment in its business K-Sea looked to Citizens Bank for a US$37 million Senior Credit Facility, US$34 million in equipment leases, and foreign exchange services. Make... -

Page 35

... new consumer loans totalling US$22 billion during 2005 and processed more than 1.5 million credit 2005 Divisional review Citizens ranks as the eighth largest commercial banking organisation in the US by deposits. Last year was Citizens' 13th consecutive year of record profits, achieved through... -

Page 36

... and distributor of metals. Our ability to meet the complex needs of large commercial customers is demonstrated in the partnership between RBS Corporate Markets, which provided Ryerson with credit facilities, and Charter One, which was able to offer treasury management services. Make it happen -

Page 37

...-supported ATMs into a number of Kroger locations. interest rate protection, foreign exchange, cash management, asset finance and administration, asset-based lending and private equity capital. The management and business of RBS Asset Finance, Inc. has been transferred from RBS Corporate Markets... -

Page 38

... Citizens' support for the community is extensive. Examples include a comprehensive, multi-million dollar investment plan to increase home ownership, strengthen commercial retail districts, and create an education district in Albany, New York; a new innovative product for low/moderate-income... -

Page 39

...and branded merchandise. Fence America. RBS Lynk, based in Atlanta, offers a range of payment systems for retail and business customers. Fence America is one of the first to use the innovative new product Treo, which allows credit card payments to be made via mobile phones. 2005 Divisional review -

Page 40

... contribution £926 million (2004 - £881 million) Total income up 8% Profit up 5% 38 RBS Insurance Churchill Home Insurance. David and Catherine Barton switched to Churchill Home Insurance last year. They loved the brand, saved £200 and found the quality of service excellent. Make it happen -

Page 41

... red telephone in 2005. When it first opened for business in April 1985, Direct Line employed just 63 people. Today it employs around 6,500 people and handles an average of 12,000 car quotes every day. Across its range of brands and products, RBS Insurance increased its total policies in-force by... -

Page 42

... Your Mortgage Magazine Direct Line - Special Achievement Award Superbrands Churchill - Best Home and Contents Insurance Provider Your Money Direct Awards Churchill - Travel Insurer of the Year International Travel Insurance Journal Awards Churchill - Customer Service Complaints Team of the Year... -

Page 43

...14 days have their cars crushed. NIG. For the broker market, quick and accurate online quotations are an important part of their competitive offering. NIG's Commercial Quotes system is regularly accessed by brokers such as Saffron Insurance to provide commercial insurance for their customers. 2005... -

Page 44

...telephone, property and purchasing support for the Group's customer-facing divisions. 42 Manufacturing Gogarburn. On 14 September 2005, Her Majesty The Queen and His Royal Highness The Duke of Edinburgh formally opened the new RBS headquarters in Edinburgh. It provides a superb working environment... -

Page 45

...dealing with corporate customers - helping to make the Group one of the top service providers for corporate and commercial customers in 2005. In November 2005 a new Tesco Personal Finance Centre was created in Glasgow bringing together telephony, loans and savings functions under one management team... -

Page 46

... Services Global Innovator's Award - Group Property CoreNet Industry Champion European Call Centre Awards Top prize for Business Infrastructure and Facilities Management Strategy and Delivery Royal Institute of Chartered Surveyors Property Management Awards Corporate Occupier of the year... -

Page 47

... Ulster Bank branch network, with work planned on a further 57 during 2006. Document Solutions processed 345 million customer communications in 2005, making it one of the largest mailing facilities in Europe. This enlarged facility in Scotland increased capacity and resilience for the Group. 2005... -

Page 48

... for the sector. 46 Corporate Responsibility Toynbee Hall is based in the east end of London. Through our partnership RBS has created an innovative programme of modules to help adults better understand and manage their finances, including the material for Services Against Financial Exclusion which... -

Page 49

... the Group second amongst the 25 Financial Service sector companies. Key statistics £368.3 billion loaned to our customers In the UK we are the sixth largest employer in the FTSE 100 paying £4.9 billion to our employees in salaries £2.7 billion paid to the UK Exchequer £2.0 billion paid to... -

Page 50

... long term benefit through genuine partnerships with charities, community groups, employees and other stakeholders. 48 Corporate Responsibility Community investment In the UK, we focus on three programmes that we believe have a strong and positive impact: Supporting Staff Giving, Money Matters... -

Page 51

... 250,000 who are now more active outdoors. School Banks. New to the Face2Face programme - the school banks train pupils to manage a branch helping them to understand money and the banking system. In the first year, 20 school banks have been established across the UK. 2005 Corporate Responsibility -

Page 52

50 -

Page 53

... income statement 61 Analysis of results 69 Divisional performance 82 Consolidated balance sheet 84 Cash flow 85 IFRS compared with US GAAP 85 Capital resources 86 Risk management 51 Operating and financial review section 01 Operating and financial review Annual Report and Accounts 2005 -

Page 54

...the Report and Accounts, and unless specified otherwise, the term 'company' means The Royal Bank of Scotland Group plc, 'RBS' or the 'Group' means the company and its subsidiary undertakings, 'the Royal Bank' means The Royal Bank of Scotland plc and 'NatWest' means National Westminster Bank Plc. The... -

Page 55

... include, but are not limited to: general economic conditions in the UK and in other countries in which the Group has significant business activities or investments, including the United States; the monetary and interest rate policies of the Bank of England, the Board of Governors of the Federal... -

Page 56

... Markets by customer grouping presented in this review. Corporate Markets provides an integrated range of core banking, structured finance and financial markets products and services, including acquisition finance, trade finance, leasing, factoring, treasury services, money markets, foreign exchange... -

Page 57

... range of retail and corporate banking services, including personal banking, residential mortgages and cash management. In addition, Citizens engages in a wide variety of commercial lending, consumer lending, commercial and consumer deposit products, merchant credit card services, insurance products... -

Page 58

... sterling-dollar and sterling-euro exchange rates, affect the value of assets and liabilities denominated in foreign currencies and affect earnings reported by the Group's nonUK subsidiaries, mainly Citizens, RBS Greenwich Capital and Ulster Bank, and may affect income from foreign exchange dealing... -

Page 59

... net gain on sale of strategic investments and subsidiaries, and average equity shareholders' funds. Basis of preparation of pro forma results In preparing its annual results, the Group has taken advantage of the option in IFRS 1 'First-time Adoption of International Financial Reporting Standards... -

Page 60

...purchased intangible assets Integration costs Net gain on sale of strategic investments and subsidiaries Profit before tax Tax on profit Profit for the year Minority interests Preference dividends Profit attributable to ordinary shareholders Basic earnings per ordinary share Intangibles amortisation... -

Page 61

..., the final dividend will be paid on 9 June 2006 to shareholders registered on 10 March 2006. The total dividend is covered 2.4 times by earnings before purchased intangibles amortisation, integration costs and net gain on sale of strategic investments and subsidiaries. Balance sheet Total assets of... -

Page 62

... integration costs and net gain on sale of strategic investments and subsidiaries increased by 8%, from 162.6p to 175.9p. Balance sheet Total assets were £776.8 billion at 31 December 2005, 12% higher than total assets of £696.5 billion at 1 January 2005. Lending to customers, excluding repurchase... -

Page 63

...Overseas Net interest margin (5) Group UK Overseas The Royal Bank of Scotland plc base rate (average) London inter-bank three month offered rates (average): Sterling Eurodollar Euro Notes: (1) Interest-earning assets and interest-bearing liabilities exclude the Retail bancassurance long-term assets... -

Page 64

...UK - Overseas Customer accounts: savings deposits - UK - Overseas Customer accounts: other time deposits - UK - Overseas Debt securities in issue - UK - Overseas Subordinated liabilities - UK - Overseas Internal funding of trading business - UK - Overseas Total interest-bearing liabilities - banking... -

Page 65

... profit or loss. Related interest-earning assets and interest-bearing liabilities have also been adjusted. (4) Interest receivable and interest payable on trading assets and liabilities are included in income from trading activites. Annual Report and Accounts 2005 Operating and financial review... -

Page 66

...: savings deposits UK Overseas Customer accounts: other time deposits UK Overseas Debt securities in issue UK Overseas Subordinated liabilities UK Overseas Internal funding of trading business UK Overseas Total interest payable of the banking business UK Overseas Movement in net interest income UK... -

Page 67

... bancassurance income and realised investment securities gains. General insurance premium income, after reinsurance, rose by 5%, or £256 million to £5,779 million reflecting volume growth in motor and home insurance products. 01 Operating and financial review Annual Report and Accounts 2005 -

Page 68

...to £11,298 million to support the strong growth in business volumes. Excluding acquisitions and at constant exchange rates, operating expenses were up by 10%, £962 million. Staff costs were up £713 million, 14% to £5,844 million reflecting business growth. The number of staff increased by 400 to... -

Page 69

... under UK GAAP but under IFRS are now amortised over 3-5 years. All software relating to the NatWest integration was fully amortised by the end of 2005. The balance of integration costs principally relates to the integration of Churchill, First Active and Citizens' acquisitions, including Charter... -

Page 70

... at 1 January 2005. Total provision coverage (the ratio of total balance sheet provisions for impairment to total risk elements in lending) decreased from 70% to 65%. The ratio of total balance sheet provisions for impairment to total risk elements in lending and potential problem loans decreased to... -

Page 71

...financial review section Corporate Markets Retail Markets Retail Banking Retail Direct Wealth Management Total Retail Markets Ulster Bank Citizens RBS Insurance Manufacturing Central items Profit before amortisation of purchased intangible assets, integration costs and net gain on sale of strategic... -

Page 72

...the opportunities for increased co-operation between Corporate Markets and Citizens. In Asia, our profile has benefited from the announcement of the Group's strategic partnership with Bank of China. Our businesses continue to deliver good returns. Weighted risk assets rose by 14% over the course of... -

Page 73

... review section Total assets* Loans and advances to customers - gross* Customer deposits* Weighted risk assets * excluding repos and reverse repos 70.4 67.9 60.0 74.2 61.6 59.4 51.8 65.6 Corporate Markets generated good results in the Mid-Corporate & Commercial customer segment in 2005, building... -

Page 74

... depreciation and rental asset funding costs, non-interest income now accounts for 69% of Global Banking & Markets revenues. We recorded good growth in fees earned from customer services in risk management, financial structuring and debtraising. A strong performance from RBS Greenwich Capital, which... -

Page 75

...Insurance net claims Contribution before impairment losses Impairment losses Contribution 2005 £bn 1 January 2005 £bn Total banking assets Loans and advances to customers - mortgages - personal - cards - business Customer deposits Investment management assets - excluding deposits Weighted risk... -

Page 76

...2,992 1 January 2005 £bn 74 Operating and financial review Insurance net claims Contribution before impairment losses Impairment losses Contribution Total banking assets Loans and advances to customers - gross - mortgages - personal - business Customer deposits Weighted risk assets 77.1 47.3 13... -

Page 77

... 410 748 75 Operating and financial review section 31 December 2005 £bn 1 January 2005 £bn Total assets Loans and advances to customers - gross - mortgages - cards - other Customer deposits Weighted risk assets 27.2 13.8 9.5 4.0 2.7 20.5 23.0 9.4 9.3 3.8 2.8 19.4 Total income rose by 11% to... -

Page 78

... 2005 £bn 76 Operating and financial review Contribution before impairment losses Impairment losses Contribution Loans and advances to customers - gross Investment management assets - excluding deposits Customer deposits Weighted risk assets 7.8 25.4 25.5 6.1 7.1 21.6 22.3 6.0 Total income... -

Page 79

... new credit card and direct loan products. The number of personal and business customers increased by 68,000 in the year. Ulster Bank personal customer numbers rose by 9% in the Republic of Ireland, where our switcher mortgage product has helped us to gain market share. In Northern Ireland, Ulster... -

Page 80

... income. We have grown our customer numbers in both personal and business segments, with Charter One increasing its small business and corporate customer base by 10%. Co-operation between Citizens and RBS Corporate Markets is yielding good results. Citizens' new international cash management service... -

Page 81

... home claims following severe storms in the UK in January 2005. The UK combined operating ratio for 2005 was 93.6% (2004 - 93.3%). section Annual Report and Accounts 2005 Operating and financial review Operating and financial review Earned premiums Reinsurers' share Insurance premium income Net... -

Page 82

... up 2%, with support for increased business volumes offset by efficiency improvements. The Group Efficiency Programme was substantially completed during the year, with major implementations such as a new system for handling customer queries and a new customer account-opening platform. The Churchill... -

Page 83

...charge of £45 million, in addition to a charge for £14 million for hedge ineffectiveness under IFRS. Employee numbers at 31 December 2005 2004 Corporate Markets Retail Banking Retail Direct Wealth Management Ulster Bank Citizens RBS Insurance Manufacturing Centre Group total 15,700 33,100 6,800... -

Page 84

...bills Loans and advances to banks Loans and advances to customers Debt securities Equity shares Intangible assets Property, plant and equipment Settlement balances Derivatives at fair value Prepayments, accrued income and other assets Total assets Liabilities Deposits by banks Customer accounts Debt... -

Page 85

... dividends, £0.1 billion. The fair value of the assets of the Group's post-retirement benefit schemes was £17.4 billion (2004 - £14.8 billion) and the present value of defined benefit obligations was £21.1 billion (2004 - £17.7 billion). The increase in net pension liability (after tax... -

Page 86

... from investing activities Net cash flows from financing activities Effects of exchange rate changes on cash and cash equivalents Net increase in cash and cash equivalents 8,950 (2,612) (703) (3,107) 2,528 2,493 (9,398) 7,119 1,686 1,900 84 Operating and financial review 2005 The major factors... -

Page 87

...relating to financial instruments principally foreign exchange gains on available-for-sale securities recognised in net income under IFRS but included directly in equity under US GAAP together with the adjustment for financial assets and liabilities designated as at fair value through profit or loss... -

Page 88

... Group Risk Committee Group Credit Committee Group Asset and Liability Management Committee • Group Audit Committee is a non-executive committee that supports the Board in carrying out its responsibilities for financial reporting including accounting policies and in respect of internal control... -

Page 89

.... The annual business planning and performance management process and associated activities ensure the expression of risk appetite remains appropriate. GRC and GALCO support this work. Annual Report and Accounts 2005 Operating and financial review tat nt i ua Policies Q 01 Risk y risk ator... -

Page 90

... with approved risk appetite. Group Risk Management is responsible for setting standards for maintaining and developing credit risk management throughout the Group. This is achieved via a combination of governance structures, credit risk policies, control processes and credit systems collectively... -

Page 91

... used in existing credit risk models prior to implementation. Annual Report and Accounts 2005 Operating and financial review Operating and financial review section default ("PD")/customer credit grade - these models assess the probability that the customer will fail to make full and timely... -

Page 92

...of loans and advances (including overdraft facilities), instalment credit, finance lease receivables, debt securities and other traded instruments across all customer types. Credit risk assets Corporate Markets Retail Banking Retail Direct Wealth Management Citizens RBS Insurance Ulster Bank Credit... -

Page 93

... 30%) relate to individuals (personal and retail customers) and include mortgage lending and other smaller loans that are intrinsically well-diversified. Corporate industry sectors, including public sector and quasi government, account for 48% (2004 - 46%) of credit risk assets, with banks and other... -

Page 94

... 92 Operating and financial review 40% 27.3 20% 52.2 0% 2004 Rest of world Europe North America 49.3 2005 United Kingdom Distribution of credit risk assets by product and customer type Lending to corporate customers Lending to individuals (mortgages) Debt securities to banks, sovereigns and... -

Page 95

... to 1.60% of customer loans and advances at 31 December 2005 (1 January 2005 - 1.84%). REIL by division The table below shows REIL by division. REIL Corporate Markets Retail Banking Retail Direct Wealth Management Ulster Bank Citizens RBS Insurance Total REIL 2005 £m 1 January 2005 £m 31 December... -

Page 96

... Review Forum chaired by the Group Chief Executive or the Group Finance Director. Early and active management of problem exposures ensures that credit losses are minimised. Specialised units are used for different customer types to ensure that the appropriate risk mitigation is taken in a timely... -

Page 97

...040) 172 1,703 (144) 3,887 01 Operating and financial review An impairment provision calculated using the effective interest rate method leaves a discounted asset; the discount unwinds at a constant effective rate until the outstanding asset is completely realised. Annual Report and Accounts 2005 -

Page 98

... of the balance sheet is regularly reviewed over the plan horizon and funding strategies and options are developed by Group Treasury and implemented after review and approval by GALCO. The level of large deposits taken from banks, corporate customers, non-bank financial institutions and other... -

Page 99

...of the Group's assets and liabilities is also managed within internal policy limits, to ensure that term asset commitments may be funded on an economic basis over their life. In managing its overall term structure, the Group analyses and takes into account the effect of retail and corporate customer... -

Page 100

...Group's policy parameters. 2005 £m 2004 £m 98 Operating and financial review Net short-term wholesale market activity Debt securities, treasury bills and other eligible bills Reverse repo agreements with banks and customers Less: repos with banks and customers Short positions Insurance Companies... -

Page 101

... advantage of anticipated market conditions. The main risk factors are interest rates, credit spreads and foreign exchange. Financial instruments held in the Group's trading portfolios include, but are not limited to, debt securities, loans, deposits, securities sale and repurchase agreements and... -

Page 102

Operating and financial review continued The VaR for the Group's trading portfolios segregated by type of market risk exposure, including idiosyncratic risk, is presented in the table below. Trading Interest rate Credit spread Currency Equity and commodity Diversification Total trading VaR Average ... -

Page 103

... its general insurance business are the principal sources of non-trading equity price risk. The Group's portfolios of nontrading financial instruments mainly comprise loans (including finance leases), debt securities, equity shares, deposits, certificates of deposits and other debt securities issued... -

Page 104

...-balance sheet items and do not reflect the behaviouralised repricing used in the Group's asset and liability management methodology and the nontrading interest rate VaR presented above. Currency risk The Group does not maintain material non-trading open currency positions other than the structural... -

Page 105

... control of changes policy wordings and any subsequent • Underwriting and pricing risk, • Claims management risk, • Reinsurance risk, • Reserving risk Annual Report and Accounts 2005 Operating and financial review Reinsurance and insurance of Group assets are centrally controlled... -

Page 106

... review Claims management risk Claims management risk is the risk that claims are paid inappropriately. Claims are managed using a range of IT system controls and manual processes conducted by experienced staff, to ensure that claims are handled in a timely and accurate manner. Detailed policies... -

Page 107

... or theft of the Group's physical, logical and intangible assets. Annual Report and Accounts 2005 Operating and financial review Operating and financial review c) Commercial other insurance contracts Other commercial claims come mainly from business interruption and loss arising from the... -

Page 108

...corporate reputation arising from any of the Group's activities. Enterprise risk management is achieved through monitoring the Group's exposure to direct or indirect loss using a range of policies, procedures, data, analytical tools and reporting techniques. In particular, Group-wide risk management... -

Page 109

Governance Contents 108 Board of directors and secretary 110 Report of the directors 115 Corporate governance 121 Directors' remuneration report 130 Directors' interests in shares 131 Statement of directors' responsibilities 107 Governance section 02 Governance Annual Report and Accounts 2005 -

Page 110

Board of directors and secretary 108 Board of directors and secretary Sir George Mathewson Sir Fred Goodwin Sir Tom McKillop Lawrence Fish Guy Whittaker Gordon Pell Archie Hunter Joe MacHale Charles 'Bud' Koch Janis ... -

Page 111

... Parliament and Business Exchange. A C N R member of the Audit Committee member of the Chairman's Advisory Group member of the Nominations Committee member of the Remuneration Committee independent non-executive director * Annual Report and Accounts 2005 Governance Board of directors and... -

Page 112

... the Royal Bank and NatWest. The Group is engaged principally in providing a wide range of banking, insurance and other financial services. The financial risk management objectives and policies of the Group and information on the Group's exposure to price, credit, liquidity and cash flow risk are... -

Page 113

...service agreement. Annual Report and Accounts 2005 Governance Report of the directors section Ordinary shares: Legal & General Group plc Barclays PLC The Capital Group of Companies, Inc 11% cumulative preference shares: Guardian Royal Exchange Assurance plc Windsor Life Assurance Company Limited... -

Page 114

... from Total Reward, a wide range of information about reward and benefits has been introduced through RBSpeople.com, an internet site offering 24 hour access from home or work. The RBS group Charity Lottery was launched during 2005. Employees contributing to the prize fund through a small monthly... -

Page 115

... year. This year, for the very first time, the Group scored above the ISR Global Financial Services Norm in every single category. The survey results are presented at Board, divisional and team levels. Action plans are developed to address any issues identified. With continuing year-on-year... -

Page 116

...does not have any trade creditors. Directors' indemnities In terms of section 309C of The Companies Act 1985 (as amended), the directors of the company, members of the Group Executive Management Committee and Approved Persons of the Group (under the Financial Services and Markets Act 2000) have been... -

Page 117

...the company. Meetings of the Board are structured to allow open discussion. The Board met nine times during 2005 and was supplied with comprehensive papers in advance of each Board meeting covering the Group's principal business activities. Members of the executive management attend and make regular... -

Page 118

...relevant disclosures in relation to the formulation and review of the Group's executive remuneration policy. The Remuneration Committee makes recommendations to the Board on the remuneration arrangements for its executive directors and the Chairman. The Directors' Remuneration Report is contained on... -

Page 119

... Institute of Chartered Accountants in England and Wales in 1999. The effectiveness of the Group's internal control system is reviewed regularly by the Board and the Audit Committee. Executive management committees or boards of directors in each of the Group's businesses receive quarterly reports on... -

Page 120

... the Board which has authorised the Group Chief Executive and the Group Finance Director to certify that as at 31 December 2005, the company's disclosure controls and procedures were adequate and effective and designed to ensure that material information relating to the company and its consolidated... -

Page 121

... the interim and annual financial statements to the Group Board. This core agenda is supplemented by additional meetings as required, four being added in 2005. Audit Committee meetings are attended by relevant executive directors, the internal and external auditors and risk management executives. At... -

Page 122

... that there will be an external review of the effectiveness of the Audit Committee every three years, with internal reviews by the Board continuing in the intervening years. In 2005 the Audit Committee reviewed the audit committee structure throughout the Group and as a result proposed to the... -

Page 123

... decisions taking account of the remuneration environment and the performance and responsibilities of the individual director. Benefits UK-based executive directors are eligible to participate in The Royal Bank of Scotland Group Pension Fund ("the RBS Fund"). 02 Governance • Total rewards will... -

Page 124

... profit sharing scheme, which currently pays up to 10 per cent of salaries, depending on the Group's performance. These schemes are not subject to performance conditions since they are operated on an all-employee basis. Executive directors also receive death-in-service benefits. Short-term annual... -

Page 125

...Lawrence Fish's total remuneration package was reviewed in 2004 by the Remuneration Committee as a result of the acquisition of Charter One and his changing RBS responsibilities in North America. A new cash long-term incentive plan was approved by shareholders at the 2005 Annual General Meeting. The... -

Page 126

...160 124 Directors' remuneration report 140 120 100 Index 80 60 40 20 0 2000 RBS 2001 FTSE 100 2002 2003 2004 2005 Source: Datastream Service contracts The company's policy in relation to the duration of contracts with directors is that executive directors' contracts generally continue... -

Page 127

...the plans, policies and practices of Citizens at the time of termination. The Remuneration Committee has been advised that these termination provisions are less generous than the current market practice in the US. As Group Finance Director, Mr Whittaker will be eligible to receive short-term annual... -

Page 128

...of Charter One Financial, Inc. For these services Mr Koch receives $402,500 per annum. Mr Scott's senior independent director fee covers all Board and Board Committee work including Chairmanship of the Remuneration Committee. No director received any expense allowances chargeable to UK income tax or... -

Page 129

... Robertson retired from the Board on 20 April 2005. *** Mr Watt resigned from the Board on 31 January 2006. The performance conditions for options granted in 2005 are detailed on page 123. Annual Report and Accounts 2005 Governance 57,259 57,259 Directors' remuneration report section 69,257 147... -

Page 130

Directors' remuneration report continued No options had their terms and conditions varied during the accounting period to 31 December 2005. No payment is required on the award of an option. The executive share options which are exercisable from March 2002 onwards are subject to the satisfaction of ... -

Page 131

... proportion of the benefits. Of the total transfer value as at 31 December 2005 shown, 25% relates to benefits in funded pension schemes. Sir George Mathewson receives life insurance cover under an individual arrangement. The non-executive directors do not accrue pension benefits, other than Mr... -

Page 132

...2006 and 7 February 2006, 7 ordinary shares of 25p each were acquired by Sir Fred Goodwin under the Group's Buy As You Earn share scheme. Notes: (1) The numbers shown in this table are taken from the audited disclosures shown elsewhere in this Annual Report. (2) The value is based on the share price... -

Page 133

... each financial year in accordance with International Financial Reporting Standards. They are responsible for preparing accounts that present fairly the financial position, financial performance, and cash flows of the Group and the Company. In preparing those accounts, the directors are required to... -

Page 134

132 -

Page 135

... 134 Independent auditors' report 136 Accounting policies 145 Consolidated income statement 146 Balance sheets 147 Statements of recognised income and expense 148 Cash flow statements 149 Notes on the accounts 133 Financial statements section 03 Financial statements Annual Report and Accounts 2005 -

Page 136

... to the members of The Royal Bank of Scotland Group plc We have audited the financial statements of The Royal Bank of Scotland Group plc ("the company") and its subsidiaries (together "the Group") for the year ended 31 December 2005 which comprise the accounting policies, the balance sheets as at... -

Page 137

... as at 31 December 2005 and of its profit and cash flows for the year then ended; • the company financial statements give a true and fair view, in Independent auditors' report to the members of The Royal Bank of Scotland Group plc section accordance with IFRS as adopted for use in the European... -

Page 138

... are designated as at fair value through profit or loss, available-for-sale financial assets and investment property. Recognised financial assets and financial liabilities in fair value hedges are adjusted for changes in fair value in respect of the risk that is hedged. 3. Basis of consolidation The... -

Page 139

... by the Group are stated at cost less accumulated amortisation and impairment losses. Amortisation is charged to profit or loss using methods that best reflect the economic benefits over their estimated useful 137 Accounting policies section 03 Financial statements Annual Report and Accounts 2005 -

Page 140

...-for-sale reserve in equity unless the asset is the hedged item in a fair value hedge. The assets and liabilities of foreign operations, including goodwill and fair value adjustments arising on acquisition, are translated into sterling at foreign exchange rates ruling at the balance sheet date... -

Page 141

... of financial assets, financial liabilities or both that the Group manages and Annual Report and Accounts 2005 Financial statements Designated as at fair value through profit or loss - financial assets that the Group designates on initial recognition as being at fair value through profit or loss... -

Page 142

... purchases of financial assets classified as loans and receivables are recognised on settlement date; all other regular way purchases are recognised on trade date. Fair value for a net open position in a financial asset that is quoted in an active market is the current bid price times the number of... -

Page 143

... of financial liabilities designated as at fair value through profit or loss are (a) structured liabilities issued by the Group: designation significantly reduces the measurement inconsistency between these liabilities and the related derivatives carried at fair value, and (b) investment contracts... -

Page 144

... account the option's exercise price, its term, the risk free interest rate and the expected volatility of the market price of The Royal Bank of Scotland Group plc's shares. Vesting conditions are not taken into account when measuring fair value, but are reflected by adjusting the number of options... -

Page 145

...Deposits by banks, Customer accounts, Debt securities in issue and Subordinated liabilities. Derivative assets and Derivative liabilities are shown separately on the face of the balance sheets. Gains or losses arising from changes in fair value of financial instruments classified as held-for-trading... -

Page 146

... June 2005, places conditions on the option in IAS 39 to designate on initial recognition a financial asset or financial liability as at fair value through profit or loss. The amendment is effective for annual periods beginning on or after 1 January 2006. Earlier application is encouraged. The Group... -

Page 147

...565 (305) 8,769 1,485 7,284 1,995 5,289 145 Consolidated income statement section 6 57 109 5,392 5,558 177 256 4,856 5,289 Per 25p ordinary share: Basic earnings Diluted earnings Dividends 9 9 7 169.4p 168.3p 60.6p 157.4p 155.9p 52.5p 03 Financial statements Annual Report and Accounts 2005 -

Page 148

... to banks Loans and advances to customers Debt securities Equity shares Investments in Group undertakings Intangible assets Property, plant and equipment Settlement balances Derivatives at fair value Prepayments, accrued income and other assets Total assets Liabilities Deposits by banks Customer... -

Page 149

... for the year ended 31 December 2005 Group Note 2005 £m 2004 £m Company 2005 £m 2004 £m Available-for-sale investments Net valuation gains taken direct to equity Net profit taken to income on sales Cash flow hedges Net (losses)/gains taken direct to equity Exchange differences on translation... -

Page 150

...to defined benefit pension schemes Other non-cash items Net cash inflow from trading activities Changes in operating assets and liabilities Net cash flows from operating activities before tax Income taxes (paid)/received Net cash flows from operating activities Investing activities Sale and maturity... -

Page 151

... and related hedges and funding. Group 2005 £m 2004 £m 683 39 1,023 598 2,343 616 149 Notes on the accounts section 36 811 525 1,988 2 Operating expenses Administrative expenses Staff costs Wages, salaries and other staff costs Social security costs Share-based compensation Pension costs... -

Page 152

...independent of the Group's finances. In addition to The Royal Bank of Scotland Group Pension Fund ('Main Scheme'), the Group operates a number of other UK and overseas pension schemes. It also provides other post-retirement benefits, principally through subscriptions to private healthcare schemes in... -

Page 153

...relates to unfunded schemes. Annual Report and Accounts 2005 Financial statements Notes on the accounts section Changes in value of net pension liability At 1 January 2004 Currency translation and other adjustments Income statement: Expected return Interest cost Current service cost Past service... -

Page 154

...properties Net gains on financial assets and liabilities designated as at fair value through profit or loss Expenses Interest on subordinated liabilities Direct operating expenses of investment properties Integration expenditure* relating to: - acquisition of NatWest - other acquisitions Group 2005... -

Page 155

... foreign exchange movements Foreign profits taxed at other rates Unutilised losses brought forward and carried forward Adjustments relating to prior periods Actual tax charge for the year 2,381 79 230 (166) (10) 77 (5) (208) 2,378 2,185 - 110 (128) (10) 49 6 (217) 1,995 (1) Deferred tax assets of... -

Page 156

...in respect of equity preference shareholders for payment on 31 March 2006. 7 Ordinary dividends 2005 p per share Group 2004 p per share 2005 £m 2004 £m Final dividend for previous year declared during the current year Interim dividend Total dividends paid on ordinary equity shares 41.2 19.4 60... -

Page 157

... - Annual Report and Accounts 2005 Financial statements Held-for-trading Designated as at fair value through profit or loss Loans and receivables Finance leases 53,963 616 350,960 11,687 417,226 - - 567 - 567 Notes on the accounts section Number of ordinary shares: Weighted average number of... -

Page 158

... mortgage related securities, US Government agency collateralised mortgage obligations, and other types of financial assets. In such transactions, the assets, or interests in the assets, are transferred generally to a special purpose entity which then issues liabilities to third party investors... -

Page 159

... million) relating to these securitisations. Net pre-tax gains are based on the difference between the sales prices and previous carrying values of assets prior to date of sale, are net of transaction costs, and exclude any results attributable to hedging activities, interest income, funding costs... -

Page 160

... levels on certain designated mortgages. The Group is not obliged, and does not intend, to support losses that may be suffered by the Agencies. Under the terms of the sale agreements, the Agencies have agreed to seek repayment only from the cash from the mortgage loans. Once the securities exchanged... -

Page 161

... securities UK government £m Other government £m Group Other public sector body £m Bank and building society £m Other issuers £m 2005 Total £m Held-for-trading Designated as at fair value through profit or loss Available-for-sale Loans and receivables At 31 December 2005 Available-for-sale... -

Page 162

... because they reflect changes in benchmark interest rates. 14 Equity shares Listed £m Unlisted £m Group 2005 Total £m Listed £m Unlisted £m 2004 Total £m Held-for-trading Designated as at fair value through profit or loss Available-for-sale Investment securities Other securities At 31... -

Page 163

... area of operation The Royal Bank of Scotland plc National Westminster Bank Plc(1) Citizens Financial Group, Inc. Coutts & Co(2) Greenwich Capital Markets, Inc. RBS Insurance Group Limited Ulster Bank Limited(3) Notes: (1) The company does not hold any of the NatWest preference shares in issue... -

Page 164

... financial assets 2005 Cost £m Group Provision £m Net book value £m Impaired financial assets Loans and receivables and finance leases Available-for-sale 5,926 316 6,242 3,344 132 3,476 Group 2,582 184 2,766 162 Notes on the accounts Impairment losses charged to the income statement Loans... -

Page 165

... goodwill, subject to amortisation are: Years The amortisation expense for each of the next five years is currently estimated to be: £m Core deposit intangibles Other purchased intangibles 6 7 2006 2007 2008 2009 2010 113 113 113 67 20 03 Financial statements Annual Report and Accounts 2005 -

Page 166

...164 Notes on the accounts Citizens (acquired 2004) RBS Insurance Charter One Charter One 4,471 Earnings Earnings Earnings Expected earnings and cash generation multiples, including control premium Value-in-use: cash flow Allocation of common resources Mellon business typical of recent transactions... -

Page 167

...1,268 Investment properties are valued to reflect fair market value. Valuations are carried out by qualified surveyors who are members of the Royal Institution of Chartered Surveyors, or an equivalent overseas body. The 31 December 2005 valuation for a significant majority of the Group's investment... -

Page 168

... at fair value Companies in the Group enter into various off-balance sheet financial instruments (derivatives) as principal either as a trading activity or to manage balance sheet foreign exchange and interest rate risk. Derivatives include swaps, forwards, futures and options. They may be traded on... -

Page 169

... transferred risks to the trading portfolio or to external third party participants in the derivatives market. Group Fair value Notional amounts £bn Positive £m Negative £m Book value Assets £m Liabilities £m 2004 Exchange rate contracts Spot, forwards and futures Currency swaps and options... -

Page 170

... replacement cost of internal trades is not included as there is no credit risk associated with them. Group Within one year £m One to five years £m Over five years £m Total £m 2004 Before netting Exchange rate contracts Interest rate contracts Credit derivatives Equity and commodity contracts... -

Page 171

... include insurance linked liabilities with a carrying value of £2,296 million. The carrying amount of other customer accounts designated as at fair value through profit or loss is £114 million greater than amortised cost. No amounts have been recognised in profit or loss for changes in credit risk... -

Page 172

... accrued income and other assets, Note 20) Net deferred tax Group 2005 £m 2004 £m Company 2005 £m 2004 £m 1,695 (156) 1,539 Group 2,061 (47) 2,014 - (3) (3) - - - Accelerated capital Pension allowances £m £m Provisions £m Deferred gains £m Fair value of Other financial transition... -

Page 173

...General insurance business (i) Claims and loss adjustment expenses Group Gross £m Reinsurance £m Net £m Notified claims Incurred but not reported At 1 January 2004 Cash paid for claims settled in the year Increase in liabilities - arising from current year claims - arising from prior year claims... -

Page 174

... return variances Economic assumption changes Other Closing net assets 772 34 16 (13) 3 7 (15) 23 824 New business contribution represents the present value of future profits on new insurance contract business written during the year. Movement in provision for liabilities under life contracts and... -

Page 175

... classified as investment contracts (within customer deposits) 2005 £m 2004 £m 1,497 2,217 8 49 1,640 2,131 1,491 1,887 14 65 1,514 1,943 Annual Report and Accounts 2005 Financial statements Notes on the accounts section There are no options and guarantees relating to life assurance... -

Page 176

... liabilities Group 2005 £m 2004 £m Company 2005 £m 2004 £m Designated as at fair value through profit or loss Amortised cost 150 28,124 28,274 12,977 10,236 2,840 2,221 28,274 11,013 9,353 - 9,242 9,242 2,039 1,244 2,344 3,615 9,242 4,850 1,085 174 Notes on the accounts Dated loan... -

Page 177

... Notes on the accounts section 371 54 1,260 5,920 3,408 Group 2004 - call date Sterling US$ Euro Other Dated loan capital Sterling US$ Euro Other Undated loan capital Currently £m 2005 £m 2006 £m 2007-2009 £m 2010- 2014 £m thereafter £m perpetual £m Total £m - - - - - - 1,316... -

Page 178

... 1,572 202 176 Notes on the accounts Company 2005 - call date Dated loan capital - US$ Undated loan capital - US$ Sterling US$ Euro Preference securities Currently £m 2006 £m 2007 £m 2008 - 2010 £m 2011- 2015 £m thereafter £m perpetual £m Total £m - 484 - 595 - 595 1,079 33 24... -

Page 179

... up and fully paid 1 January 2005 £m Issued during the year £m 31 December 2005 £m Authorised 31 December 2005 £m 31 December 2004 £m Equity shares Ordinary shares of 25p Non-voting deferred shares of £0.01 Total equity share capital Non-equity shares Additional Value Shares of £0.01 Non... -

Page 180

... schemes which had been exchanged for options over the company's shares following the acquisition of NatWest in 2000; (b) 7.4 million ordinary shares in lieu of cash in respect of the final dividend for the year ended 31 December 2004 and the interim dividend for the year ended 31 December 2005; and... -

Page 181

... other resolution). In addition, in the event that, prior to any general meeting of shareholders, the company has failed to pay in full the three most recent quarterly dividend payments due on the non-cumulative dollar preference shares, the two most recent semi-annual dividend payments due on the... -

Page 182

...and other movements Profit attributable to ordinary and equity preference shareholders Ordinary dividends paid Equity preference dividends paid Preference dividends - non-equity Share-based payments, net of tax Actuarial losses recognised in post-retirement benefit schemes, net of tax At 31 December... -

Page 183

... term performance plan. 181 Notes on the accounts section 32 Leases Minimum amounts receivable and payable under non-cancellable leases Within 1 year £m Group Year in which receipt or payment will occur After 1 year but within 5 years £m After 5 years £m 2005 Total £m Finance lease assets... -

Page 184

... lease assets in balance sheet Transportation Cars and light commercial vehicles Other 7,742 978 333 9,053 6,185 895 585 7,665 182 Notes on the accounts Amounts recognised as income and expense Finance lease receivables - contingent rental income Operating lease payables - minimum payments... -

Page 185

... 60 16 38,020 2005 £m 16,071 4,852 1,268 - 4 22,195 2004 £m Liabilities secured by charges on assets Deposits by banks Customer accounts Debt securities in issue Other liabilities 11,407 6,761 11,347 20 29,535 5,628 2,001 6,561 - 14,190 03 Financial statements Annual Report and Accounts 2005 -

Page 186

... financial performance and customer behaviour, and qualitative inputs, such as company management performance or sector outlook. Every customer credit grade across all grading scales in the Group can be mapped to a Group level credit grade which uses a five band scale from AQ1 to AQ5. • Loss... -

Page 187

...limits and other policy parameters set by Group Asset and Liability Management Committee (GALCO). The structure of the Group's balance sheet is managed to maintain substantial diversification, to minimise concentration across its various deposit sources, and to contain the level of reliance on total... -

Page 188

... advantage of anticipated market conditions. The main risk factors are interest rates, credit spreads and foreign exchange. Financial instruments held in the Group's trading portfolios include, but are not limited to, debt securities, loans, deposits, securities sale and repurchase agreements and... -

Page 189

... the management of internal funds flow within the Group's businesses. Money market portfolios include cash instruments (principally debt securities, loans and deposits) and related hedging derivatives. Retail and corporate banking Structural interest rate risk arises in these activities where assets... -

Page 190

... of quoted and unquoted investments, or its portfolio of strategic investments. These investments are carried at fair value with changes in fair value recorded in profit or loss, or equity. Insurance risk The Group is exposed to insurance risk, either directly through its businesses or through using... -

Page 191

... fall due. Claims development data provides information on the historical pattern of reserving risk. Current estimate of cumulative claims Cumulative payments to date Liability recognised on the balance sheet Liability in respect of prior years Claims handling costs Total liability included on the... -

Page 192

... each major class of business, gross and net of reinsurance. 190 Notes on the accounts 2005 Earned premiums £m Claims incurred £m Loss ratio % Earned premiums £m 2004 Claims incurred £m Loss ratio % Residential property Personal motor Commercial property Commercial motor Creditor Other Total... -

Page 193

... accounts is the economic environment. Life business The three regulated life companies of RBSG, NatWest Life Assurance Limited, Royal Scottish Assurance plc ("RSA") and Direct Line Life Limited, are required to meet minimum capital requirements at all times under the Financial Service Authority... -

Page 194

... into consideration that assets and liabilities are actively managed and may vary at the time that any actual market movement occurs. Purchased insurance The Insurance Sourcing Department is responsible to GEMC for the Group-wide purchase of insurance as a means of reducing other risk exposures. -

Page 195

Group Remaining maturity 2005 1 month or less £m Within 3 months £m 3-12 months £m 1-5 years £m Over 5 years £m Equity shares £m Total £m Liabilities Deposits by banks Customer accounts Debt securities in issue Settlement balances and short positions Derivatives at fair value ... -

Page 196

... 2005 Company 1 month or less £m 1-3 months £m 3-12 months £m 1-5 years £m Over 5 years £m Total £m Assets Loans and advances to banks Loans and advances to customers Derivatives at fair value Liabilities Deposits by banks Customer accounts Debt securities in issue Subordinated liabilities... -

Page 197

... £m After 6 months but less than 1 year £m After 1 year but less than 5 years £m Over 5 years £m Total interest earning/ bearing £m Yield % Non interest earning/ bearing £m Fair value through profit or loss £m Banking book total £m Trading book total £m Total £m Assets Loans and... -

Page 198

... bills Other assets Total assets Liabilities and equity Deposits by banks Customer accounts Debt securities in issue Subordinated liabilities Other liabilities Shareholders' equity Internal funding of trading business Total liabilities and equity Off-balance sheet items interest rate sensitivity gap... -

Page 199

...2005 3 months or less £m Over 5 years £m Yield % Banking Book Total £m Assets Loans and advances to banks Loans and advances to customers Investment in subsidiaries Other assets Total assets Liabilities and equity Deposits by banks Customer accounts Debt securities in issue Other liabilities... -

Page 200

...Debt securities Held-for-trading Designated as at fair value through profit or loss Available-for-sale Loans and receivables Banking business Trading business 80,653 3,991 35,533 788 80,653 3,991 35,533 788 39,182 54,726 93,908 38,998 54,726 93,724 - - - - 120,965 120,965 Equity shares Held... -

Page 201

Group 2005 Carrying value £m 2005 Fair value £m 2004 Carrying value £m 2004 Fair value £m 2005 Carrying value £m Company 2005 Fair value £m 2004 Carrying value £m 2004 Fair value £m Financial liabilities Deposits by banks Held-for-trading Amortised cost Banking business Trading business ... -

Page 202

... 34 Financial instruments (continued) Industry risk - geographical analysis Group Loans and advances to banks and customers £m Treasury bills, debt securities and equity shares £m Netting and offset (2) £m 2005 Derivatives £m Other (1) £m Total £m 200 Notes on the accounts UK Central... -

Page 203

... - - - Annual Report and Accounts 2005 Financial statements Notes on the accounts section Total Central and local government Manufacturing Construction Finance Service industries and business activities Agriculture, forestry and fishing Property Individuals Home mortgages Other Finance lease and... -

Page 204

... of credit, supporting customer debt issues and contingent liabilities relating to customer trading activities such as those arising from performance and customs bonds, warranties and indemnities. Commitments Commitments to lend - under a loan commitment the Group agrees to make funds available... -

Page 205

...and customers Increase in insurance liabilities Increase/(decrease) in debt securities in issue Increase/(decrease) in other liabilities Increase/(decrease) in derivative liabilities Increase in settlement balances and short positions Changes in operating liabilities Total income taxes paid Net cash... -

Page 206

... (704) (216) 337 (402) (65) 39 Analysis of changes in financing during the year Group Company Subordinated liabilities 2004 £m 2005 £m 2004 £m Share capital 2005 £m 2004 £m Subordinated liabilities 2005 £m 2004 £m 204 Notes on the accounts At 1 January Implementation of IAS 32 At 1 January... -

Page 207

... £m Total £m Provisions £m Corporate Markets Retail Banking Retail Direct Wealth Management Ulster Bank Citizens RBS Insurance Manufacturing Central items Eliminations Operating profit before amortisation of purchased intangibles, integration costs and net gain on sale of strategic investments... -

Page 208

... acquire fixed assets and intangible Liabilities assets £m £m 2004 Cost to acquire fixed assets and intangible Liabilities assets £m £m Group Assets £m Assets £m 206 Notes on the accounts Corporate Markets Retail Banking Retail Direct Wealth Management Ulster Bank Citizens RBS Insurance... -

Page 209

... trading activities Other operating income Insurance premium income (net of reinsurers' share) Total income Operating profit before tax Total assets Total liabilities Net assets attributable to equity shareholders and minority interests Contingent liabilities and commitments Cost to acquire property... -

Page 210

...pages 126 to 129. Compensation of key management The aggregate remuneration of directors and other members of key management during the year was as follows: Group 2005 £000 2004 £000 Short-term benefits Post-employment benefits Other long-term Share-based payments 26,180 9,383 4,215 1,568 41,346... -

Page 211

...021 Key management have banking relationships with Group entities which are entered into in the normal course of business. Key management had no reportable transactions or balances with the company except for dividends. 44 Related parties (a) Group companies provide development and other types of... -

Page 212

... consolidation of entities controlled by the reporting entity. Control is the ability to direct the financial and operating policies of an entity. IFRS requires a level rate of return on the net investment in the lease. Tax cash flows are not reflected in the pattern of income recognition. Assets... -

Page 213

... IFRS balance sheet (1 January 2004). (i) Investment property Investment property is revalued annually to open market value and changes in market value reflected in the Statement of total recognised gains and losses. (j) Share-based payments No expense is recognised for options over The Royal Bank... -

Page 214

...for-sale financial assets are reported in a separate component of shareholders' equity. Changes in the fair value of financial assets held-for-trading or designated as at fair value are taken to profit or loss. Financial assets can be classified as held-to-maturity only if they have a fixed maturity... -

Page 215

... not closely related to the economic characteristics of the host contract, unless the entire contract is carried at fair value through profit or loss. Embedded derivatives are not bifurcated from the host contract. Annual Report and Accounts 2005 Financial statements (s) Loan impairment Under UK... -

Page 216

..., the balance sheet value of financial assets and financial liabilities increased by £104 billion. 214 Notes on the accounts (u) Insurance contracts All contracts within the life assurance business are accounted for as insurance contracts and the obligations to policyholders presented as Long-term... -

Page 217

... 4 Opening balance sheet at 1 January 2004 - Group UK GAAP £m Dividends £m Income tax £m Software development Leases Consolidation costs £m £m £m Share Investment based Employee property payment benefits £m £m £m Insurance £m Total adjustments £m IFRS £m Assets Cash and balances at... -

Page 218

...to IFRS (continued) Opening balance sheet at 1 January 2004 - Company UK GAAP £m Dividends £m Valuation of subsidiaries £m Total adjustments £m IFRS £m 216 Notes on the accounts Assets Loans and advances to banks Loans and advances to customers Investments in Group undertakings Prepayments... -

Page 219

... - Group UK GAAP £m Dividends £m Income tax £m Property plant and equipment £m Software development Leases Consolidation costs £m £m £m Investment property £m Share based payment £m Employee benefits £m Insurance Goodwill £m £m Total adjustments £m IFRS £m Assets Cash and balances at... -

Page 220

... to banks Loans and advances to customers Investments in Group undertakings Prepayments, accrued income and other assets Total assets Liabilities Deposits by banks Debt securities in issue Accruals, deferred income and other liabilities Subordinated liabilities Shareholders' equity Total liabilities... -

Page 221

...£m £m Insurance contracts £m Fair value Total option Other adjustments £m £m £m IFRS 1 January 2005 £m Assets Cash and balances at central banks 4,293 - - Treasury bills and other eligible bills 6,110 - - Loans and advances to banks 61,073 4,425 165 Loans and advances to customers 347,251... -

Page 222

...Fair value option £m Total adjustments £m IFRS 1 January 2005 £m 220 Notes on the accounts Assets Loans and advances to banks Loans and advances to customers Investment in Group undertakings Derivatives at fair value Prepayments, accrued income and other assets Total assets Liabilities Deposits... -

Page 223

... the related loan or facility. (e) Pension costs Pension scheme assets are measured at their fair value. Scheme liabilities are measured on an actuarial basis using the projected unit method and discounted at the current rate of return on a high quality corporate bond of equivalent term and currency... -

Page 224

... such and carried at fair value with changes in fair value recognised in net income. A financial liability may be designated as at fair value through profit or loss. Such differences are included with other unrealised gains and losses and reported in a separate component of equity. Only financial... -

Page 225

... unfavourable terms. An instrument is classified as equity if it evidences a residual interest in the assets of the Group after the deduction of liabilities. (j) Offset arrangements A financial asset and a financial liability are offset and the net amount reported in the balance sheet when... -

Page 226

...-force policies together with net assets in excess of the statutory liabilities. US GAAP does not permit embedded value reporting. US GAAP requires bancassurance contracts to be classified either as insurance or investment contracts. US GAAP requires deferred acquisition cost and income accounting... -

Page 227

..., the related non-trading derivative is remeasured at fair value and the resulting profit or loss taken to the income statement. Monetary assets denominated in a foreign currency are retranslated at closing rates with exchange differences taken to profit or loss. Equity shares financed by foreign... -

Page 228

... 1998 was capitalised and amortised over its estimated useful economic life. Goodwill arising on acquisitions before 1 October 1998 was deducted from equity. The carrying amount of goodwill in the Group's opening IFRS balance sheet was its carrying value under UK GAAP as at 31 December 2003. There... -

Page 229

... property provisions Loan origination Pension costs Long-term assurance business Extinguishment of liabilities Financial instruments Derivatives and hedging Liabilities and equity Intangible assets - timing difference Other Taxation Net income available for ordinary shareholders - US GAAP 2005... -

Page 230

...the benefits in respect of service to date, with due allowance for future earnings increases. The plan assets consist mainly of fixed-income securities and listed securities. The investment policy followed for the plan seeks to deploy the plan assets primarily in UK and overseas equity shares and UK... -

Page 231

... to its main UK pension plan in 2006. 47 Post balance sheet events There have been no significant events between the year end and the date of approval of these accounts which would require a change to or disclosure in the accounts. Annual Report and Accounts 2005 Financial statements Notes on... -

Page 232

230 -

Page 233

... with UK GAAP 231 Additional information section 250 Exchange rates 251 Off balance sheet arrangements 253 Economic and monetary environment 253 Supervision and regulation 257 Description of property and equipment 257 Major shareholders 04 Additional information Annual Report and Accounts 2005 -

Page 234

... expenses (2, 3, 4) Insurance net claims Operating profit before impairment losses Impairment losses Operating profit before tax Tax Profit for the year Minority interests Preference dividends Profit attributable to ordinary shareholders Notes: (1) Includes gain on sale of strategic investment of... -

Page 235

... dividend paid and final dividend proposed as a percentage of profit attributable to ordinary shareholders before integration costs, amortisation of purchased intangibles and net gain on sale of strategic investments and subsidiaries (net of tax). (3) Return on average total assets represents profit... -

Page 236