RBS 2005 Annual Report Download - page 216

Download and view the complete annual report

Please find page 216 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

214

Notes on the accounts

UK GAAP

(t) Offset

Under UK GAAP an intention to settle net is not a requirement

for set off; the entity must have the ability to insist on net

settlement and that ability is assured beyond doubt.

(u) Insurance contracts

All contracts within the life assurance business are accounted

for as insurance contracts and the obligations to policyholders

presented as Long-term assurance liabilities attributable to

policyholders.

The value placed on in-force policies includes future

investment margins.

(v) Linked presentation

FRS 5 ‘Reporting the Substance of Transactions’ allows

qualifying transactions to be presented using the linked

presentation.

(w) Extinguishment of liabilities

Under UK GAAP, recognition of a financial liability ceases once

any transfer of economic benefits to the creditor is no longer likely.

IFRS

For a financial asset and a financial liability to be offset, IFRS

require that an entity must intend to settle on a net basis or to

realise the asset and settle the liability simultaneously.

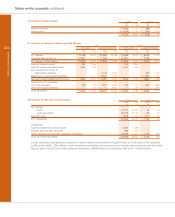

On implementation of IAS 32, the balance sheet value

of financial assets and financial liabilities increased by

£104 billion.

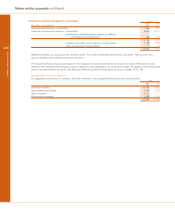

IFRS 4 requires life assurance products to be classified

between insurance contracts and investment contracts. The

latter are accounted for in accordance with IAS 39. Insurance

contracts continue to be accounted for using the embedded

value methodology.

The value of in-force policies excludes any amounts that reflect

future investment margins.

There is no linked presentation under IFRS. If substantially all

the risks and rewards have been retained, the gross assets

and related funding are presented separately.

A financial liability is removed from the balance sheet when,

and only when, it is extinguished i.e. when the obligation

specified in the contract is discharged or cancelled or expires.

Notes on the accounts continued

45 Transition to IFRS (continued)