RBS 2005 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

section

01

Operating and

financial review

75

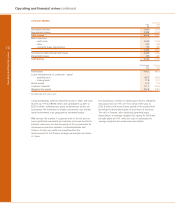

Operating and financial review

Annual Report and Accounts 2005

Retail Direct

Pro forma

2005 2004

£m £m

Net interest income 882 779

Non-interest income 1,084 995

Total income 1,966 1,774

Direct expenses

– staff costs 230 225

– other 375 391

605 616

Contribution before impairment losses 1,361 1,158

Impairment losses 571 410

Contribution 790 748

31 December 1 January

2005 2005

£bn £bn

Total assets 27.2 23.0

Loans and advances to customers – gross

– mortgages 13.8 9.4

– cards 9.5 9.3

– other 4.0 3.8

Customer deposits 2.7 2.8

Weighted risk assets 20.5 19.4

Total income rose by 11% to £1,966 million and contribution by

6% to £790 million, a strong performance in the context of

slower growth in demand for unsecured credit and higher

levels of consumer arrears. This performance reflected

disciplined pricing, tight cost control and stringent credit

assessment. Contribution before impairment losses increased

by 18% to £1,361 million.

During the year, the number of customer accounts increased

by 734,000 (4%). In the light of changing market conditions we

have focussed our marketing efforts on existing customers,

and this has resulted in very strong growth in our core NatWest

and RBS brands. We gained 336,000 credit card accounts in

these brands in the second half, 60% more than in the

equivalent period of 2004.

Net interest income increased by 13% to £882 million, reflecting

the success of the First Active brand in the UK mortgage

market and the maturing of the MINT portfolio. MINT, launched

in December 2003, made a contribution of £37 million in 2005.

Average loans and advances rose by 15% to £24.9 billion

with the fastest growth coming in mortgages, up 34% at

£11.9 billion. Personal loan growth slowed, reflecting strategic

decisions taken over the last 18 months to reposition pricing

and tighten lending criteria for personal loans sold directly.

Net interest margin was only slightly lower than in 2004, as

wider margins on our cards portfolio balanced the effects of

the increasing weight of mortgage assets in our loan book.

Non-interest income was up 9% to £1,084 million, benefiting

from higher volumes in both domestic and international card

acquiring, strong sales through Tesco Personal Finance, the

introduction of balance transfer fees and good growth in

Europe.

Expenses decreased by 2% to £605 million, with stringent cost

control across all activities, including reduced marketing costs

on personal loans. This was consistent with our more cautious

approach to direct lending and with our successful focus on

branch recruitment.

Impairment losses rose by 39% to £571 million, reflecting

higher lending volumes as well as the increase in personal

arrears signalled at the end of 2004. There are some signs of

a stabilisation of credit quality, assisted by the tightening of

lending criteria. Mortgage arrears remain very low. The

average loan-to-value ratio on new mortgages written in 2005

was 51% and on the stock of mortgages was 44%.