RBS 2005 Annual Report Download - page 240

Download and view the complete annual report

Please find page 240 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

238

Additional information

Additional information continued

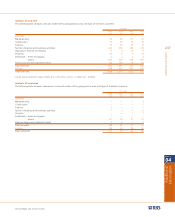

Risk elements in lending and potential problem loans

The Group’s loan control and review procedures do not include the classification of loans as non-accrual, accruing past due,

restructured and potential problem loans, as defined by the SEC in the US. The following table shows the estimated amount of

loans that would be reported using the SEC’s classifications. The figures are stated before deducting the value of security held or

related provisions.

IAS 39 requires interest to be recognised on a financial asset (or a group of financial assets) after impairment at the rate of interest used

to discount recoveries when measuring the impairment loss. Thus, interest on impaired financial assets is credited to profit or loss as the

discount on expected recoveries unwinds. Despite this, such assets are not considered performing. All loans that have an impairment

provision are classified as non-accrual. This is a change from past practice where certain loans with provisions were classified as past

due 90 days or potential problem loans (and interest accrued on them).

IFRS

2005 2004

£m £m

Loans accounted for on a non-accrual basis (2):

Domestic 4,977 3,658

Foreign 949 1,075

Total 5,926 4,733

Accruing loans which are contractually overdue 90 days or more as to principal or interest (3):

Domestic 2 634

Foreign 7 79

Total 9713

Loans not included above which are classified as ‘troubled debt restructurings’ by the SEC:

Domestic 2 14

Foreign — 10

Total 224

Total risk elements in lending 5,937 5,470

Potential problem loans (4)

Domestic 14 173

Foreign 5 107

Total potential problem loans 19 280

Closing provisions for impairment as a % of total risk elements in lending 65% 76%

Closing provisions for impairment as a % of total risk elements in lending and potential problem loans 65% 72%

Risk elements in lending as a % of gross lending to customers excluding reverse repos 1.60% 1.83%

Notes:

(1) For the analysis above, 'Domestic' consists of the United Kingdom domestic transactions of the Group. 'Foreign' comprises the Group’s transactions conducted through offices

outside the UK and through those offices in the UK specifically organised to service international banking transactions.

(2) All loans against which an impairment provision is held are reported in the non-accrual category.

(3) Loans where an impairment event has taken place but no impairment recognised. This category is used for over-collateralised non-revolving credit facilities.

(4) Loans for which an impairment event has occurred but no impairment provision is necessary. This category is used for over-collateralised advances and revolving credit facilities

where identification as 90 days overdue is not feasible.

IFRS

2005 2004

£m £m

Gross income not recognised but which would have been

recognised under the original terms of non-accrual and restructured loans

Domestic 334 235

Foreign 62 58

396 293

Interest on non-accrual and restructured loans included in net interest income

Domestic 130 58

Foreign 14 7

144 65