RBS 2005 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

section

01

Operating and

financial review

71

Operating and financial review

Annual Report and Accounts 2005

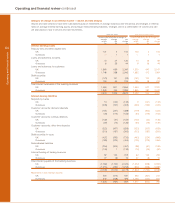

Corporate Markets – Mid-Corporate and Commercial

Pro forma

2005 2004

£m £m

Net interest income 1,760 1,607

Non-interest income 1,257 1,171

Total income 3,017 2,778

Direct expenses

– staff costs 529 489

– other 132 123

– operating lease depreciation 335 322

996 934

Contribution before impairment losses 2,021 1,844

Impairment losses 218 277

Contribution 1,803 1,567

31 December 1 January

2005 2005

£bn £bn

Total assets* 70.4 61.6

Loans and advances to customers – gross* 67.9 59.4

Customer deposits* 60.0 51.8

Weighted risk assets 74.2 65.6

* excluding repos and reverse repos

Corporate Markets generated good results in the Mid-Corporate

& Commercial customer segment in 2005, building on the

strength of its UK franchise. We maintained our market-leading

positions in corporate and commercial banking, asset finance

and invoice finance. Total income rose by 9% to £3,017 million,

whilst contribution rose by 15% to £1,803 million.

Net interest income increased 10% to £1,760 million as a result

of strong growth in average lending, up £7.7 billion, or 16%

and in average customer deposits, up £5.1 billion, or 12%.

Average interest-bearing deposits grew particularly strongly.

Non-interest income rose by 7% to £1,257 million, reflecting

our success in cross-selling our full range of products and

services to customers. Our business has benefited from the

co-location of our Lombard and Invoice Finance managers

with our corporate and commercial banking operations.

Expense growth, excluding operating lease depreciation,

was 8% which included a further investment in customer-

facing staff.

Impairment losses were 21% lower than in 2004 at

£218 million, reflecting a further improvement in our strong

credit metrics.