RBS 2005 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

74

Operating and financial review

Operating and financial review continued

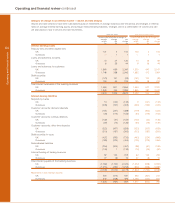

Retail Banking

Pro forma

2005 2004

£m £m

Net interest income 3,175 3,173

Non-interest income 2,258 1,999

Total income 5,433 5,172

Direct expenses

– staff costs 1,026 963

– other 311 329

1,337 1,292

Insurance net claims 486 398

Contribution before impairment losses 3,610 3,482

Impairment losses 601 490

Contribution 3,009 2,992

31 December 1 January

2005 2005

£bn £bn

Total banking assets 77.1 72.8

Loans and advances to customers – gross

– mortgages 47.3 44.1

– personal 13.7 13.2

– business 16.3 15.3

Customer deposits 77.7 71.9

Weighted risk assets 54.0 51.1

Retail Banking produced a stronger performance in the second

half, when it achieved year-on-year income growth of 7%,

compared with 3% in the first half. Total income for 2005

rose by 5% to £5,433 million and contribution by 1% to

£3,009 million. Contribution before impairment losses

increased by 4% to £3,610 million.

Overall customer numbers have increased since December

2004 with personal customers up 274,000 (2%) and registered

internet customers up 30%. During 2005 we continued to

demonstrate our commitment to customer service, with

significant progress in terms of the proportion of our

customers who are “extremely’’ satisfied and we are making

pleasing progress in the current account switcher market.

Among the high street banks, Royal Bank of Scotland ranks

first for customer satisfaction with NatWest now in joint second

place. NatWest remains the number one bank for students. In

2005, 44% of first year students in England and Wales chose

to open new accounts with us compared with 42% in 2004.

Against the backdrop of a slower rate of growth in consumer

borrowing, we have delivered robust growth in average loans

and advances, which increased by 11%. Average mortgage

lending grew by 12% to £46.1 billion, with particularly good

growth in higher margin products such as the offset mortgage.

Average unsecured personal lending, where we took further

steps to enhance our focus on high quality new business, was

up 10% to £13.3 billion. Average customer deposits grew by

6% to £70.9 billion, with particularly good inflows into savings

products.

Net interest income was stronger in the second half, recovering

from a dip in the first half to reach £3,175 million for the full year.

Net interest margin was lower in 2005 than in 2004 but second

half margin was similar to the first half, with increased product

margins offsetting mix effects. Spreads in mortgages and

some savings products improved in the latter part of the year.

Non-interest income rose by 13% to £2,258 million. In

bancassurance, Annualised Premium Equivalent income

increased by 25% to £171 million, with good sales of Child

Trust Funds and portfolio bonds. Excluding bancassurance

premium and other income, non-interest income increased by

11% to £1,567 million, reflecting growth in income from core

personal and small business banking services, and good

progress in our private banking and investment businesses.

Direct expense growth was contained to 3%, despite some

investment in future income initiatives in the second half. Staff

costs increased by 7% to £1,026 million as a result of

continued investment in customer-facing staff with over 500

additional customer advisors in branches, an increase in

telephone banking advisors, and continued expansion of our

bancassurance and investment businesses. We continue to

make efficiency gains in other areas resulting in a 5%

decrease in other costs to £311 million.

Net claims in bancassurance, which under IFRS include

maturities, surrenders and liabilities to policyholders, were

£486 million compared with £398 million in 2004, reflecting

higher levels of bond maturities and increases in liabilities to

policyholders as a result of strong investment returns.

Impairment losses increased by 23% or £111 million to

£601 million. The increased charge principally reflects the

growth in lending over recent years, including 17% growth in

2004. We have taken further steps to refine our credit policy and

improved our recoveries process. Mortgage arrears remain

very low. The average loan-to-value ratio on new mortgages

written in 2005 was 62% and on the stock of mortgages was

46%. Small business credit quality remains stable.