RBS 2005 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

68

Operating and financial review

Operating and financial review continued

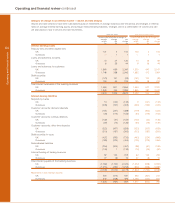

Taxation

Pro forma

2005 2004 2004

£m £m £m

Tax 2,378 1,995 1,856

%%%

UK corporation tax rate 30.0 30.0 30.0

Effective tax rate 30.0 27.4 28.4

The actual tax charge differs from the expected tax charge computed by applying the standard rate of UK corporation tax

as follows:

Pro forma

2005 2004 2004

£m £m £m

Expected tax charge 2,381 2,185 1,963

Interest on subordinated debt not allowable for tax 79 —83

Non-deductible items 230 110 110

Non-taxable items (166) (128) (128)

Taxable foreign exchange movements (10) (10) (10)

Foreign profits taxed at other rates 77 49 49

Unutilised losses – brought forward and carried forward (5) 66

Adjustments in respect of prior periods (208) (217) (217)

Actual tax charge 2,378 1,995 1,856

2005 compared with 2004

Impairment losses were £1,707 million compared with

£1,485 million in 2004 with higher provisions in Retail Markets

partly offset by improvements in Corporate Markets. The effect

of implementing the requirements of IAS 39 in 2004 would

have been to increase loan impairment losses by £105 million

for the year ended 31 December 2004.

2005 compared with pro forma 2004

New impairment losses were up 8%, £145 million to

£1,879 million. Recoveries of amounts previously written off

were up £28 million, 19% to £172 million. Consequently the

net charge to the income statement was up £117 million, 7%

to £1,707 million. Improvements in Corporate Markets partly

offset higher impairment losses in Retail Markets.

Loan impairment losses were up from £1,507 million in 2004

to £1,703 million. Other impairment losses were £4 million

compared with £83 million in 2004.

Total balance sheet provisions for impairment amounted to

£3,887 million compared with £4,145 million at 1 January 2005.

Total provision coverage (the ratio of total balance sheet

provisions for impairment to total risk elements in lending)

decreased from 70% to 65%.

The ratio of total balance sheet provisions for impairment to

total risk elements in lending and potential problem loans

decreased to 65% compared with 70% at 1 January 2005.

This reflects amounts written-off and the changing mix from

unsecured to secured exposure.

Impairment losses

Pro forma

2005 2004 2004

£m £m £m

New impairment losses 1,879 1,629 1,734

less: recoveries of amounts previously written-off (172) (144) (144)

Charge to income statement 1,707 1,485 1,590

Comprising:

Loan impairment losses 1,703 1,402 1,507

Other impairment losses 4 83 83

Charge to income statement 1,707 1,485 1,590