RBS 2005 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

section

03

Financial

statements

213

Notes on the accounts

Annual Report and Accounts 2005

UK GAAP

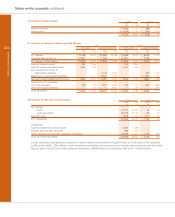

(q) Effective interest rate and lending fees

Under UK GAAP, loan origination fees are recognised when

received unless they are charged in lieu of interest.

(r) Derivatives and hedging

Under UK GAAP non-trading derivatives are accounted for on

an accruals basis in accordance with the accounting treatment

of the underlying transaction or transactions being hedged. If

a non-trading derivative transaction is terminated or ceases to

be an effective hedge, it is re-measured at fair value and any

gain or loss amortised over the remaining life of the underlying

transaction or transactions being hedged. If a hedged item is

derecognised the related non-trading derivative is remeasured

at fair value and any gain or loss taken to the income

statement.

Embedded derivatives are not bifurcated from the host

contract.

(s) Loan impairment

Under UK GAAP provisions for bad and doubtful debts are

made so as to record impaired loans at their ultimate net

realisable value. Specific provisions are established against

individual advances or portfolios of smaller balance

homogeneous advances and the general provision covers

advances impaired at the balance sheet date but which have

not been identified as such. Interest receivable from loans and

advances is credited to the income statement as it accrues

unless there is significant doubt that it can be collected.

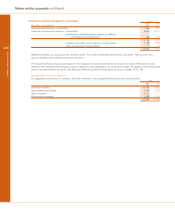

IFRS

IAS 39 requires the amortised cost of a financial instrument to

be calculated using the effective interest method. The effective

interest rate is the rate that discounts estimated future cash

flows over an instrument’s expected life to its net carrying

value. It takes into account all fees and points paid that are an

integral part of the yield, transaction costs and all other

premiums and discounts.

On implementation of IAS 39, the carrying value of financial

assets was reduced by £708 million and financial liabilities

increased by £224 million, deferred tax was reduced by £283

million and shareholders’ equity reduced by £649 million.

Under IAS 39, all derivatives are measured at fair value. Hedge

accounting is permitted for three types of hedge relationship:

fair value hedge – the hedge of changes in the fair value of a

recognised asset or liability or firm commitment; cash flow

hedge – the hedge of variability in cash flows from a

recognised asset or liability or a forecasted transaction; and

the hedge of a net investment in a foreign entity. In a fair value

hedge the gain or loss on the derivative is recognised in profit

or loss as it arises offset by the corresponding gain or loss on

the hedged item attributable to the risk hedged. In a cash flow

hedge and in the hedge of a net investment in a foreign entity,

the element of the derivative’s gain or loss that is an effective

hedge is recognised directly in equity. The ineffective element

is taken to the income statement. Certain conditions must be

met for a relationship to qualify for hedge accounting. These

include designation, documentation and prospective and

actual hedge effectiveness. On implementation of IAS 39, non-

trading derivatives were remeasured at fair value.

A derivative embedded in a contract is accounted for as a

stand-alone derivative if its economic characteristics are not

closely related to the economic characteristics of the host

contract, unless the entire contract is carried at fair value

through profit or loss.

IFRS require impairment losses on financial assets carried at

amortised cost to be measured as the difference between the

asset's carrying amount and the present value of estimated

future cash flows discounted at the asset's original effective

interest rate. There is no concept of specific and general

provision – under IFRS impairment is assessed individually for

individually significant assets but can be assessed collectively

for other assets. Once an impairment loss has been

recognised on a financial asset or group of financial assets,

interest income is recognised on the carrying amount using the

rate of interest at which estimated future cash flows were

discounted in measuring impairment.