RBS 2005 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

section

01

Operating and

financial review

79

Operating and financial review

Annual Report and Accounts 2005

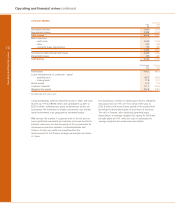

RBS Insurance

Pro forma

2005 2004

£m £m

Earned premiums 5,641 5,561

Reinsurers’ share (246) (455)

Insurance premium income 5,395 5,106

Net fees and commissions (449) (485)

Other income 543 460

Total income 5,489 5,081

Expenses

– staff costs 323 307

– other 413 345

736 652

Gross claims 3,903 3,815

Reinsurers’ share (76) (267)

Net claims 3,827 3,548

Contribution 926 881

31 December 31 December

2005 2004

In-force policies (000’s)

– Motor: UK 8,687 8,338

– Motor: Continental Europe 1,862 1,639

– Non-motor (including home, rescue, pet, HR24): UK 10,898 10,464

General insurance reserves – total (£m) 7,776 7,379

RBS Insurance produced a good performance in 2005, with

total income increasing by 8% to £5,489 million and

contribution by 5% to £926 million. The integration of Churchill

was completed in September 2005, ahead of plan, and

Churchill delivered greater transaction benefits than

anticipated at the time of the acquisition. Following the

integration of Churchill, all our direct businesses in the UK now

operate on a common platform.

RBS Insurance achieved 4% growth in UK motor policies in

force. In achieving this against a background of very strong

competition in UK motor insurance, we benefited from the

strength of our brands and the diversity of our distribution

channels. Growth came through our direct brands, through our

partnership business, where we operate insurance schemes

on behalf of third parties who in turn sell insurance products

to their customers, and through NIG, our intermediary business

acquired as part of Churchill. Our businesses in Spain,

Germany and Italy together delivered 14% growth in motor

policies in force. Linea Directa, our joint venture with Bankinter,

increased its customer base by 17% and, with more than 1

million policies, is the largest direct motor insurer and sixth

largest motor insurer in Spain.

Total home insurance policies declined by 1%. Within this total,

we continued to expand through our direct brands but there

was attrition of some partner-branded books.

In addition to expanding its intermediary business in motor and

home insurance, NIG achieved 10% growth in commercial

policies sold to SMEs.

Expenses rose by 13%. Excluding the impact of a change in

reinsurance arrangements, total income rose by 5% and

expenses by 4%. Net insurance claims on the same basis were

up by 5%, reflecting increased volumes, claims inflation in

motor and an increase in home claims following severe storms

in the UK in January 2005.

The UK combined operating ratio for 2005 was 93.6% (2004 –

93.3%).