RBS 2005 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

section

01

Operating and

financial review

59

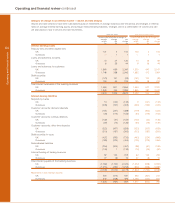

Operating and financial review

Annual Report and Accounts 2005

2005 compared with 2004

Profit

The implementation of IAS 32, IAS 39 and IFRS 4 affected the

timing of recognition of income and costs, classification of

debt and equity, impairment provisions and accounting for

insurance contracts in 2005. The effect of implementing the

requirements of these standards in 2004 would have been to

reduce profit before tax by £741 million for the year ended

31 December 2004.

Profit before tax, purchased intangibles amortisation, integration

costs and net gain on sale of strategic investments and

subsidiaries increased by 5% or £402 million, from

£7,849 million to £8,251 million. Profit before tax was up 9%,

from £7,284 million to £7,936 million.

Total income

Total income, excluding the gain on sale of strategic

investment, was up 9% or £2,178 million to £25,569 million.

This reflected growth in all divisions particularly Corporate

Markets, Citizens and Ulster Bank. The effect of implementing

the requirements of IAS 32, IAS 39 and IFRS 4 in 2004 would

have been to reduce total income by £876 million for the year

ended 31 December 2004.

Net interest income increased by 9% to £9,918 million.

Average loans and advances to customers and average

customer deposits grew by 24% and 17% respectively. The

effect of implementing the requirements of IAS 32, IAS 39 and

IFRS 4 in 2004 would have been to reduce net interest income

by £68 million for the year ended 31 December 2004. Interest

income is recognised on a constant yield basis under IFRS;

under UK GAAP interest was recognised on an accrual basis.

Non-interest income increased by 9% to £15,651 million with

good growth in banking fee income, financial markets income

and insurance premium income. Non-interest income

represents 61% of total income. The effect of implementing the

requirements of IAS 39 and IFRS 4 in 2004 would have been to

reduce non-interest income by £808 million for the year ended

31 December 2004.

Operating expenses

Operating expenses, excluding intangibles amortisation, integration

costs and loss on sale of subsidiaries, rose by 15% to £11,298

million. The effect of implementing the requirements of IAS 39

and IFRS 4 in 2004 would have been to increase operating

expenses by £74 million for the year ended 31 December 2004.

Integration

Integration costs were £458 million compared with £520 million

in 2004. Included in both periods are software amortisation

under IFRS relating to the acquisition of NatWest. The balance

principally relates to the integration of Churchill, First Active

and Citizens’ acquisitions, including Charter One which was

acquired in August 2004.

Cost:income ratio

The Group’s cost:income ratio in 2005 excluding acquisitions

was 41.8%, reflecting the impact on income in 2005 of IAS 32,

IAS 39 and IFRS 4.

Net insurance claims

Bancassurance and general insurance claims, after

reinsurance which under IFRS, include maturities and

surrenders, increased by 1% to £4,313 million. The increase

reflects volume growth and maturities of our guaranteed

capital bonds. The effect of implementing the requirements

of IFRS 4 in 2004 would have been to reduce net claims by

£314 million for the year ended 31 December 2004.

Impairment losses

Impairment losses were £1,707 million compared with

£1,485 million in 2004. Overall credit quality remained strong

in 2005, with improvements in Corporate Markets partly

offsetting higher impairment losses in Retail Markets. The

effect of implementing the requirements of IAS 39 in 2004

would have been to increase loan impairment losses by

£105 million for the year ended 31 December 2004.

Earnings

Basic earnings per ordinary share increased by 8% from 157.4p

to 169.4p. Earnings per ordinary share, adjusted for purchased

intangibles amortisation, integration costs and net gain on sale

of strategic investments and subsidiaries, increased by 3%,

from 170.2p to 175.9p. The effect of implementing the

requirements of IAS 32, IAS 39 and IFRS 4 in 2004 reduced

both basic and adjusted earnings per share by 7.6p, 5%.

A final dividend of 53.1p per ordinary share, up 29% is

recommended, giving a total dividend for the year of 72.5p, an

increase of 25%. If approved, the final dividend will be paid on

9 June 2006 to shareholders registered on 10 March 2006. The

total dividend is covered 2.4 times by earnings before

purchased intangibles amortisation, integration costs and net

gain on sale of strategic investments and subsidiaries.

Balance sheet

Total assets of £776.8 billion at 31 December 2005 were up

£188.7 billion, 32%, compared with 31 December 2004, with

£108.4 billion of this increase arising from the implementation

of IAS 32, IAS 39 and IFRS 4 on 1 January 2005, and the

balance reflecting business growth.

Loans and advances to customers were up £70.0 billion,

20%, at £417.2 billion of which £33.9 billion resulted from the

implementation of IAS 32 and IAS 39, mainly as a result of the

grossing up of previously netted customer balances. Excluding

this and a decrease in reverse repos, down 24%, £15.7 billion

to £48.9 billion, customer lending was up £51.8 billion, 16%,

reflecting organic growth across all divisions.

Customer accounts were up £59.5 billion, 21% at £342.9 billion

with £31.7 billion arising from the implementation of IAS 32 and

IAS 39, largely reflecting the grossing up of previously

netted deposits. Excluding this and repos, which decreased

£5.7 billion, 11% to £48.8 billion, deposits rose by £33.5 billion,

13%, to £294.1 billion with good growth in all divisions.

Capital ratios at 31 December 2005 were 7.6% (Tier 1) and

11.7% (Total).