RBS 2005 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

section

01

Operating and

financial review

73

Operating and financial review

Annual Report and Accounts 2005

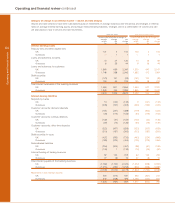

Retail Markets

Retail Markets was established in June 2005 to strengthen co-ordination and delivery of our multi-brand retail strategy across our

product range, and comprises Retail Banking, Retail Direct and Wealth Management. The performance of each of these divisions is

discussed on pages 74 to 76.

Pro forma

2005 2004

£m £m

Net interest income 4,499 4,362

Non-interest income 3,714 3,322

Total income 8,213 7,684

Direct expenses

– staff costs 1,514 1,450

– other 821 856

2,335 2,306

Insurance net claims 486 398

Contribution before impairment losses 5,392 4,980

Impairment losses 1,185 916

Contribution 4,207 4,064

1 January

2005 2005

£bn £bn

Total banking assets 114.4 104.9

Loans and advances to customers

– mortgages 64.6 56.9

– personal 21.5 20.2

– cards 9.6 9.4

– business 16.7 15.9

Customer deposits 105.9 97.0

Investment management assets – excluding deposits 31.4 26.6

Weighted risk assets 80.6 76.5

Total income increased by 7% to £8,213 million and

contribution by 4% to £4,207 million, with good discipline on

costs helping to offset increased impairment losses on

unsecured lending.

At the end of 2004 we referred to the changes being seen in

the retail markets with the consumer transitioning from an

environment which had seen several years of very fast growth

in consumer lending to an increased emphasis on savings and

investment.

As a consequence, we planned to refocus our strategy to grow

our sales of deposit and bancassurance products faster than

the market, to exploit our potential for building profitable market

share in the mortgage market and to concentrate more on the

development of our branch franchise, building on our strong

service proposition. During 2005 this transition has gathered

momentum and we have achieved good progress in our

strategies.

Branch deposit balances outgrew the market and our

bancassurance sales accelerated strongly, with annual

premium equivalent sales 25% higher than in 2004. Our share

of net mortgage lending, assisted by the launch of the First

Active brand, reached 8% in 2005. Our credit card business,

meanwhile, made excellent headway in marketing through

branch channels; we gained 60% more credit card customers

in our core NatWest and RBS brands in the second half than in

the same period of 2004.