RBS 2005 Annual Report Download - page 214

Download and view the complete annual report

Please find page 214 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

212

Notes on the accounts

UK GAAP

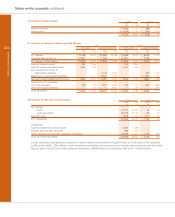

(n) Financial instruments: financial assets

Loans are measured at cost less provisions for bad and

doubtful debts, derivatives held-for-trading are carried at fair

value and hedging derivatives are accounted for in

accordance with the treatment of the item being hedged

(see Derivatives and hedging below).

Debt securities and equity shares intended for use on a

continuing basis in the Group’s activities are classified as

investment securities and are stated at cost less provision for

any permanent diminution in value. The cost of dated

investment securities is adjusted for the amortisation of

premiums or discounts. Other debt securities and equity

shares are carried at fair value.

(o) Financial instruments: financial liabilities

Under UK GAAP, short positions in securities and trading

derivatives are carried at fair value; all other financial liabilities

are recorded at amortised cost.

(p) Liabilities and equity

Under UK GAAP, all shares are classified as shareholders'

funds. An analysis of shareholders’ funds between equity and

non-equity interests is given.

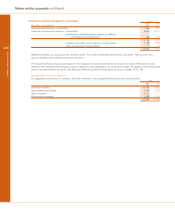

IFRS

Under IAS 39, financial assets are classified into held-to-

maturity; available-for-sale; held-for-trading; designated as at

fair value through profit or loss; and loans and receivables.

Financial assets classified as held-to-maturity or as loans and

receivables are carried at amortised cost. Other financial

assets are measured at fair value. Changes in the fair value of

available-for-sale financial assets are reported in a separate

component of shareholders’ equity. Changes in the fair value of

financial assets held-for-trading or designated as at fair value

are taken to profit or loss. Financial assets can be classified as

held-to-maturity only if they have a fixed maturity and the

reporting entity has the positive intention and ability to hold to

maturity. Trading financial assets are held for the purpose of

selling in the near term. IFRS allows any financial asset to be

designated as at fair value through profit or loss on initial

recognition. Unquoted debt financial assets that are not

classified as held-to-maturity, held-for-trading or designated as

at fair value through profit or loss are categorised as loans and

receivables. All other financial assets are classified as

available-for-sale.

IAS 39 requires all financial liabilities to be measured at

amortised cost except those held-for-trading and those that

were designated as at fair value through profit or loss on initial

recognition.

There is no concept of non-equity shares in IFRS. Instruments

are classified between equity and liabilities in accordance with

the substance of the contractual arrangements. A non-

derivative instrument is classified as equity if it does not

include a contractual obligation either to deliver cash or to

exchange financial instruments with another entity under

potentially unfavourable conditions, and, if the instrument will

or may be settled by the issue of equity, settlement does not

involve the issue of a variable number of shares. On

implementation of IAS 32, non-equity shares with a balance

sheet value of £3,192 million and £2,568 million of non-equity

minority interests were reclassified as liabilities.

Notes on the accounts continued

Impementation of IAS 32, IAS 39 and IFRS 4

45 Transition to IFRS (continued)