RBS 2005 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2005 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

144

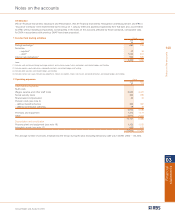

Accounting policies

incidence, timing and amount of claims and any specific

factors such as adverse weather conditions. In order to calculate

the total provision required, the historical development of

claims is analysed using statistical methodology to extrapolate,

within acceptable probability parameters, the value of

outstanding claims at the balance sheet date. Also included in

the estimation of outstanding claims are other assumptions

such as the inflationary factor used for bodily injury claims

which is based on historical trends and, therefore, allows for

some increase due to changes in common law and statute.

Costs for both direct and indirect claims handling expenses are

also included. Outward reinsurance recoveries are accounted for

in the same accounting period as the direct claims to which they

relate. The outstanding claims provision is based on information

available to management and the eventual outcome may vary

from the original assessment. Actual claims experience may differ

from the historical pattern on which the estimate is based and

the cost of settling individual claims may exceed that assumed.

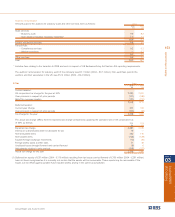

Goodwill

The Group capitalises goodwill arising on the acquisition of

businesses, as disclosed in the Accounting policies. The

carrying value of goodwill as at 31 December 2005 was

£18,823 million (2004 – £18,032 million).

Goodwill is the excess of the cost of an acquisition over the fair

value of its net assets. The determination of the fair value of

assets and liabilities of businesses acquired requires the exercise

of management judgement; for example those financial assets

and liabilities for which there are no quoted prices, and those

non-financial assets where valuations reflect estimates of

market conditions such as property. Different fair values would

result in changes to the goodwill arising and to the post-acquisition

performance of the acquisition. Goodwill is not amortised but

is tested for impairment annually or more frequently if events or

changes in circumstances indicate that it might be impaired.

For the purposes of impairment testing goodwill acquired in a

business combination is allocated to each of the Group’s cash-

generating units or groups of cash-generating units expected to

benefit from the combination. Goodwill impairment testing

involves the comparison of the carrying value of a cash-

generating unit or group of cash generating units with its

recoverable amount. The recoverable amount is the higher of the

unit's fair value and its value in use. Value in use is the present

value of expected future cash flows from the cash-generating

unit or group of cash-generating units. Fair value is the amount

obtainable for the sale of the cash-generating unit in an arm’s

length transaction between knowledgeable, willing parties.

Impairment testing inherently involves a number of judgmental

areas: the preparation of cash flow forecasts for periods that

are beyond the normal requirements of management reporting;

the assessment of the discount rate appropriate to the

business; estimation of the fair value of cash-generating units;

and the valuation of the separable assets of each business

whose goodwill is being reviewed.

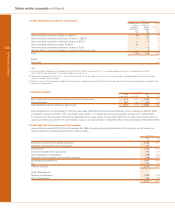

Accounting developments

International Financial Reporting Standards

The International Accounting Standards Board (“IASB”) issued

IFRS 7 ‘Financial Instruments: Disclosures’ in August 2005.

The standard replaces IAS 30 ‘Disclosures in the Financial

Statements of Banks and Similar Financial Institutions’ and the

disclosure provisions in IAS 32 ‘Financial Instruments: Disclosure

and Presentation’. IFRS 7 requires disclosure of the significance

of financial instruments for an entity’s financial position and

performance and of qualitative and quantitative information

about exposure to risks arising from financial instruments. The

standard is effective for annual periods beginning on or after 1

January 2007. Earlier application is encouraged.

At the same time the IASB issued an amendment ‘Capital

Disclosures’ to IAS 1 ‘Presentation of Financial Statements’. It

requires disclosures about an entity's capital and the way it is

managed. This amendment is also effective for annual periods

beginning on or after 1 January 2007. Earlier application is

encouraged.

The IASB has also issued three amendments to IAS 39

‘Financial Instruments: Recognition and Measurement’. The

first, ‘Cash Flow Hedge Accounting of Forecast Intragroup

Transactions’, published in April 2005, amends IAS 39 to

permit the foreign currency risk of a highly probable forecast

intragroup transaction to qualify as a hedged item in

consolidated financial statements. The amendment is effective

for annual periods beginning on or after 1 January 2006.

The second, ‘The Fair Value Option’, published in June 2005,

places conditions on the option in IAS 39 to designate on initial

recognition a financial asset or financial liability as at fair value

through profit or loss. The amendment is effective for annual

periods beginning on or after 1 January 2006. Earlier application

is encouraged. The Group has adopted this amendment from

1 January 2005 (see accounting policies on page 136).

The third, ‘Financial Guarantee Contracts’, published in August

2005, amends IAS 39 and IFRS 4 ‘Insurance Contracts’. The

amendments define a financial guarantee contract. They

require such contracts to be recorded initially at fair value

and subsequently at higher of the provision determined in

accordance with IAS 37 ‘Provisions, Contingent Liabilities

and Contingent Assets’ and the amount initially recognised

less amortisation. The amendments are effective for annual

periods beginning on or after 1 January 2006.

In December 2005, the IASB issued amendments to IAS 21

‘The Effects of Changes in Foreign Exchange Rates’ to clarify

that a monetary item can form part of the net investment in

overseas operations regardless of the currency in which it is

denominated and that the net investment in a foreign operation

can include a loan from a fellow subsidiary. The amendments

are effective immediately but have not been endorsed by the EU.

The Group is reviewing IFRS 7 and the amendments to IAS 1

and IAS 21 and those to IAS 39 that it has not implemented,

to determine their effect on its financial reporting.

US GAAP

For a discussion of recent developments in US GAAP relevant

to the Group, see Note 46 on the accounts.

Accounting policies continued